Summary

- Six constituents in the broad Alerian Midstream Energy Index (AMNA) spent a combined $745 million on equity repurchases in 3Q23.

- Corporations were more active with buybacks this quarter than MLPs, in keeping with the trend for 2023.

- Buybacks remain an important tool for returning capital to investors but also continue to compete with other capital allocation priorities.

As midstream MLPs and corporations have generated significant free cash flow in recent quarters, they have prioritized return of capital to shareholders through dividends and equity buybacks. While dividend growth was in focus last week, today’s note examines overall midstream/MLP buyback activity in 3Q23 across select Alerian energy infrastructure indices.

Midstream Buyback Activity Moderates in 3Q23

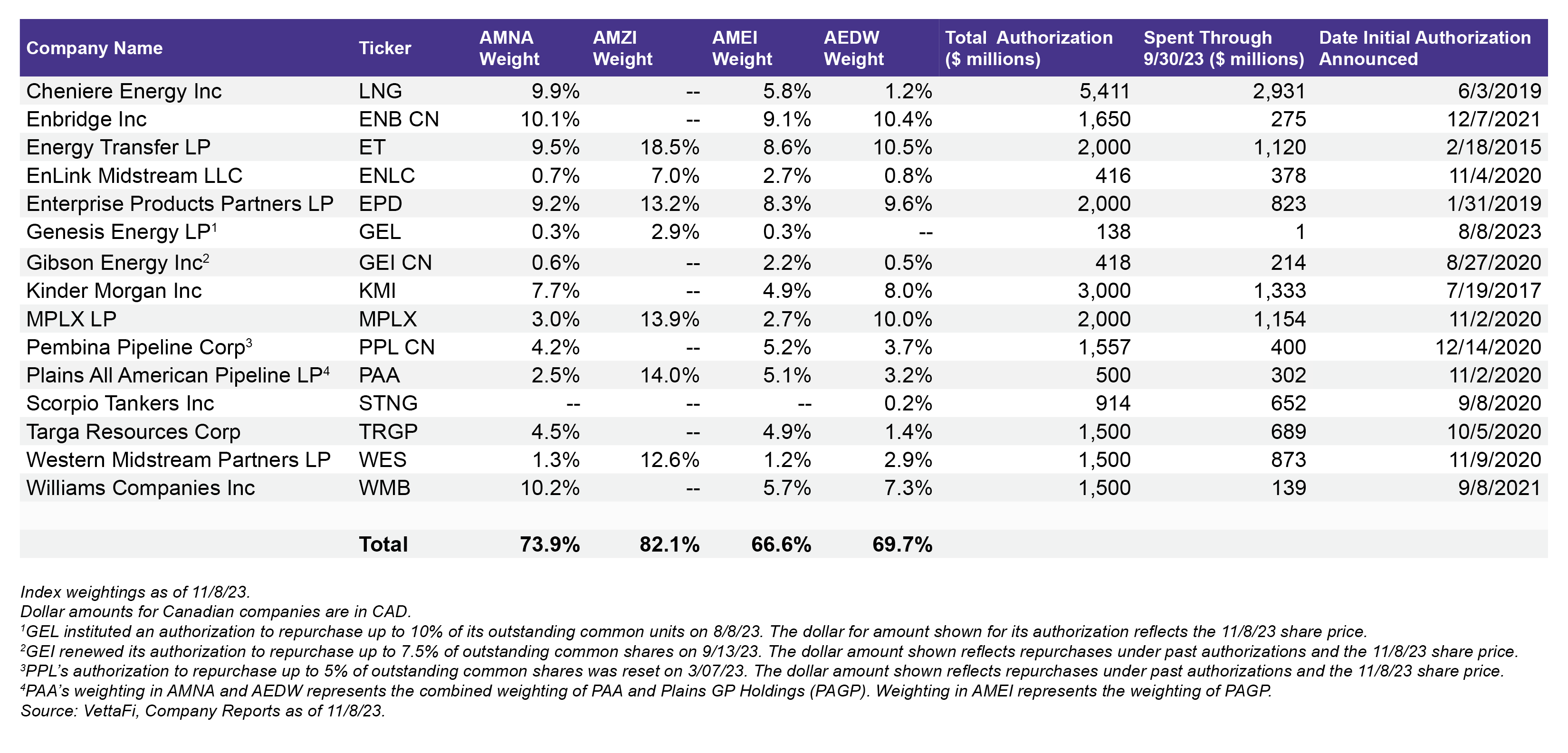

Six constituents in the Alerian Midstream Energy Index (AMNA) collectively repurchased $745 million in equity during 3Q23. Canadian C-Corps stayed on the sidelines, as did almost all MLPs. For context, AMNA constituents repurchased $1.1 billion in equity in 2Q23 and $850 million in 1Q23 (read more).[1]

Cheniere Energy (LNG) once again led the way, with $357 million in buybacks during 3Q23. In total, LNG has repurchased $1.1 billion in common equity year-to-date through 3Q23 – accounting for more than a third of the aggregate repurchases.

Following LNG, Targa Resources (TRGP) spent $132 million on buybacks in 3Q23, bringing its total year-to-date repurchases to $333 million. Kinder Morgan (KMI) bought back $73 million in equity during 3Q23, but notably spent an additional $83 million on repurchases in just the first few weeks of October (not included in table below).

Western Midstream (WES) was the only MLP with meaningful buybacks during the quarter, having repurchased $128 million in common units from Occidental (OXY) under WES’ existing buyback authorization. As a result of the repurchase, OXY’s ownership in WES is now below 50%. Finally, EnLink Midstream (ENLC) repurchased $54 million, including the repurchase of units held by Global Infrastructure Partners.

The table below shows the energy infrastructure companies with buyback authorizations in place, how much each has spent on repurchases, and each company’s weighting in AMNA, the Alerian MLP Infrastructure Index (AMZI), the Alerian Midstream Energy Select Index (AMEI), and the Alerian Midstream Energy Dividend Index (AEDW). More than two-thirds of the indexes by weighting have buyback authorizations in place.

YTD 2023 Buybacks and Other Capital Allocation Priorities

For the first three quarters of 2023, equity repurchases by AMNA constituents have totaled $2.7 billion compared to over $3.1 billion for the same period last year (read more). While aggregate buybacks are fairly similar, some of the players have changed, and activity has been less widespread.

Buybacks remain an important tool for returning capital to investors, but with many taking an opportunistic approach, repurchases can vary with the market environment. MLPs were relatively more active with buybacks in 2022 led by MPLX (MPLX), which has not done any repurchases in 2023 but increased its distribution by 9.7%. MLPs have seen stronger equity performance this year than their C-Corp peers, which likely explains in part lower buyback spending from MLPs relative to corporations this year. Cheniere Energy has been a standout for buybacks in both 2022 and 2023.

Buybacks also continue to compete with other uses of capital, including acquisitions, growth spending, debt reduction, and dividends. Several companies with buyback authorizations have announced acquisitions this year, which can reduce excess cash for buybacks. Furthermore, most companies continue to prioritize dividend growth, largely at percentages that outpace inflation. This can also contribute to more muted buybacks.

Bottom Line

With existing room under buyback authorizations and strong free cash flow generation continuing, midstream corporations and MLPs can deploy buybacks opportunistically while also balancing buybacks against other capital allocation priorities.

Related Research

Midstream Buybacks Picked Up in 2Q23

4Q22 Caps a Strong Year for Midstream/MLP Buybacks

Midstream Investors Can Give Thanks for Strong 3Q22 Buybacks

3Q23 Midstream Dividend Recap: MLPs Bring the Growth

Examining Midstream/MLP Dividend Growth by Company

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AEDW is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP) and the ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND, for which it receives an index licensing fee. However, AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND.

[1] Aggregate dollar amounts include Canadian dollars for the Canadian corporations with repurchase programs.

For more news, information, and strategy, visit the Energy Infrastructure Channel.