Markets rallied on Wednesday despite news of another quarter-point interest rate increase from the Fed. The same markets closed lower on Thursday on the heels of higher-than-expected second-quarter GDP, a familiar pattern of the last six months. Ongoing market sensitivity to changing economic data and announcements highlights the precarious position that investors continue to find themselves in as they seek to discern the path forward.

Second quarter GDP came in above even analyst expectations, lifting hopes that the U.S. may very well sidestep a recession for now. Markets appeared to run out of steam however on the heels of the GDP announcement, closing lower after a near-record run for the Dow Jones.

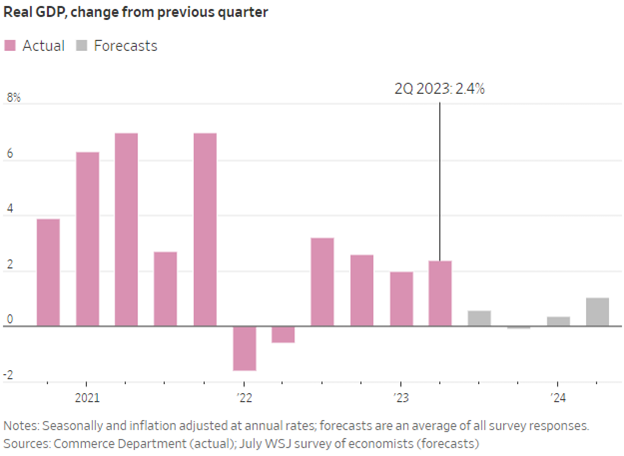

Image source: WSJ

“We’ve turned the corner on the risk here, and instead of being heavily weighted to recession, it’s balanced between recession and not recession,” Amy Crews Cutts, chief economist at AC Cutts & Associates, told the WSJ.

A Tale of Two Markets

Ongoing investor and market uncertainty has been the norm this year, prolonging volatility, while equities continue their strong rally. It’s a tale of two markets as investors remain split between fears of recession and hope for recovery.

The second quarter’s strong GDP is yet another point in favor of avoiding recession. Strong equity performance, a resilient labor market, and falling inflation alongside a still resilient consumer create hope that the U.S. may yet avoid the grips of moderate recession in the second half. Second-quarter company earnings beats add more fuel to hopes of continuing positive gains.

See also: “Equities Rally — but Is There Turmoil Underneath?”

Broad inflation continues to fall from 2022 highs and core inflation showed the first signs of significant easing in June. Core inflation — that excludes food and energy — rose just 0.2% month-over-month and 4.8% year-over-year in June. It’s the lowest core inflation has been since October 2021.

Not everyone sees falling inflation as a positive though. While consumers continue to spend, they are doing so in services, creating deflation in goods. At the same time, unemployment remains near record lows. Unemployment fell to 3.6% in June, and wages gained 4.4% for the month — wage gains now outpace inflation. Wage gains and the labor market are core measurements the Fed looks at when determining monetary policy.

BlackRock sees the months ahead as a “rollercoaster trajectory over the next quarters before inflation likely settles near 3%,” according to strategists.

The Fed hiked rates to the highest level in two decades this week, setting interest rates between 5.25%-5.5%. The regulatory body has taken what’s been dubbed as a “hawkish wait” regarding future hikes. For now, they are in a wait-and-see approach as the longer-term impacts of tightening play out. Continued economic resiliency and wage gains create uncertainty and continued fears of another potential hike later this year.

Prolonged high rates are also likely to dampen consumer spending on big-ticket items this fall. Whether the strong spending on services this summer translates to steadiness in the fall remains to be seen.

Invest for a Multitude of Market Outcomes With Managed Futures

Managed futures strategies are particularly beneficial in an environment of change. This is due to their ability to rapidly adapt to new market trends and outlooks. Should recession indeed play out, the major managed futures hedge funds maintain positions to capture continued slowing. If the economy manages to navigate a soft landing and then lift off, the funds will pivot rapidly to capture the new performers.

See also: “Managed Futures: The Rapid Responders in Crisis and Beyond”

The iMGP DBi Managed Futures Strategy ETF (DBMF) is an actively managed fund that uses long and short positions within derivatives (mostly futures contracts) and forward contracts. These contracts span domestic equities, fixed income, currencies, and commodities (via its Cayman Islands subsidiary).

The position that the fund takes within domestically managed futures and forward contracts is determined by the Dynamic Beta Engine. This proprietary, quantitative model attempts to ascertain how the largest commodity-trading advisor hedge funds have their allocations. It does so by analyzing the trailing 60-day performance of CTA hedge funds and then determining a portfolio of liquid contracts that would mimic the hedge funds’ performance (not the positions).

DBMF has a management fee of 0.85%.

For more news, information, and analysis, visit the Managed Futures Channel.