After months of lockdown in 2020-2021, there has undoubtedly been a lasting effect on the economy. Although there were a lot of negatives, several trends that were popularized by the pandemic became popular investment opportunities. While some have proven to be long-term trends, some have faded into the background. This note looks at four thematic trends post-lockdown including e-commerce, remote work, streaming media, and the metaverse.

1. E-commerce – The Future of Retail

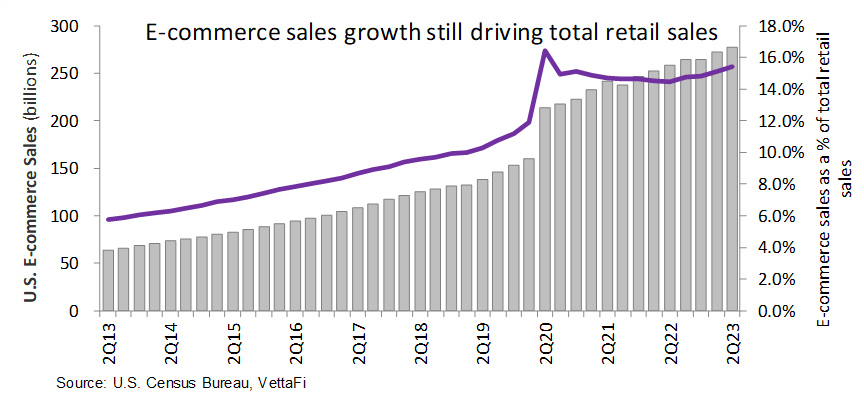

While the pandemic pulled forward e-commerce growth significantly, this was part of a longer trend that started years ago. The U.S. Census Bureau’s e-commerce data goes as far back as 4Q of 1999. And since then, e-commerce growth has outpaced total retail sales growth each quarter (even throughout the Great Recession). But because of the pandemic, growth rates increased to ~50% rates in 2020. And when those rates were lapped in 2021, they finally fell below total retail sales. This deceleration lasted from 2Q21 to 2Q22. Since then, e-commerce has grown at a much faster pace — returning closer to its normal rate of acceleration.

Growth has been mostly attributed to clothing and general goods (i.e., low volume, high replacement goods), in addition to non-store retailers like Amazon (see previous note). Furniture and home goods saw strength during the pandemic as more people stayed at home and decided to renovate/redecorate their homes. That grew weaker after the initial surge. But we could potentially see strength re-emerge as more people stay in smaller homes for longer due to higher home prices and higher interest rates.

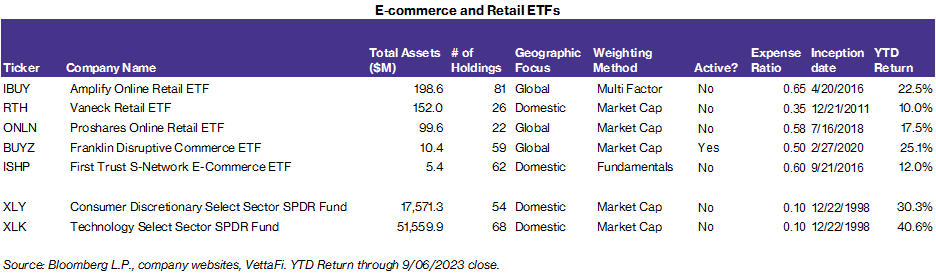

The e-commerce industry earns more revenue each year. But how do investors capture the growth besides individual stocks like Amazon? Several e-commerce ETFs exist, most of which are diversified ETFs that hold online e-commerce companies and shipping companies. Investors can also access the trend through broader retail or consumer discretionary ETFs. Most large retailers have been integrating e-commerce into their businesses and will benefit from its long-term growth.

2. Job Flexibility – Remote Work and the Gig Economy

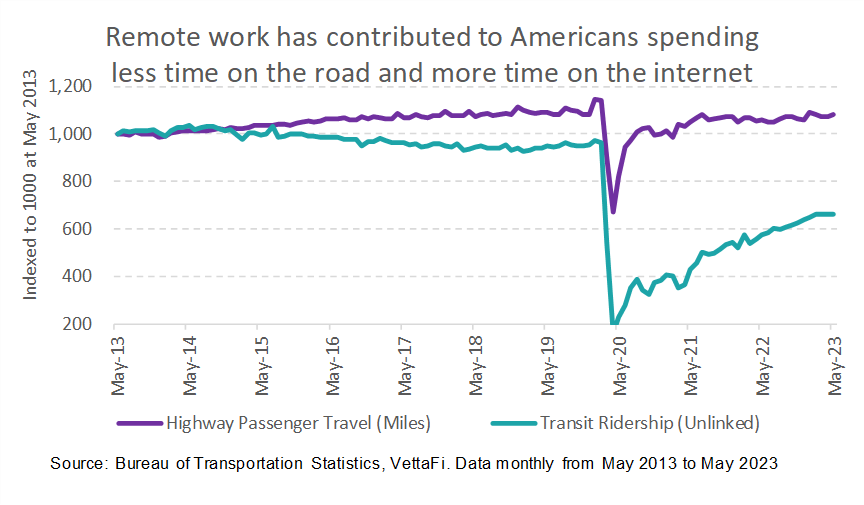

After months of remote work, many large offices have implemented return-to-office initiatives including full-time back in the office. But there is still a large portion of the workforce that works either remotely or on a hybrid schedule. Before the pandemic, the amount of remote jobs was increasing very slowly. But after the pandemic pulled forward, the trend has stuck around post-pandemic. This is partially due to greater technology capabilities and the number of computer-based employees in finance, technology, and other office roles. On top of higher commercial rent, many companies have been willing to save on office leases, especially in large cities. Data from the Survey of Working Arrangements and Attitudes (SWAA) cites that 4.7% of people worked remotely at least some of the time pre-pandemic versus a peak of 61.5% during the pandemic. The number is 30.9% post-pandemic. This data also becomes apparent when you look at commuter data (see chart below). Highway passenger miles are still trending below pre-pandemic levels. Transit ridership is significantly lower with fewer workers commuting to work. This means less time on the road and more time on the internet, contributing to e-commerce growth and greater cloud computing needs.

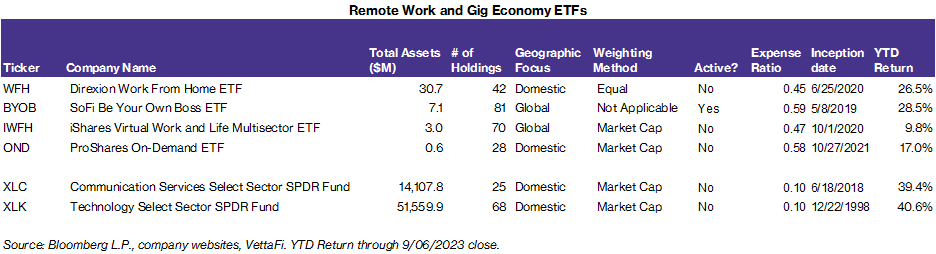

While many people enjoy the independence and flexibility of remote work, not everyone can land a remote job. Workers are turning to the gig economy, which expanded significantly during the pandemic. Many customers turned to app-based delivery services like Uber Eats (UBER), DoorDash (DASH), and Grubhub (GRUB) when restaurants weren’t open for dining. Customers also started using grocery delivery or curbside pickup from Amazon Fresh (AMZN), Walmart (WMT), or Instacart (to trade under CART after its IPO) to avoid crowded grocery stores. Although the industry has grown crowded and many customers have returned to restaurants and grocery stores, Instacart’s upcoming IPO illustrates that there’s still room for growth, particularly for players with better technology and advertising opportunities. According to Instacart, only 12% of grocery sales are made online and they predict that number could double over time.

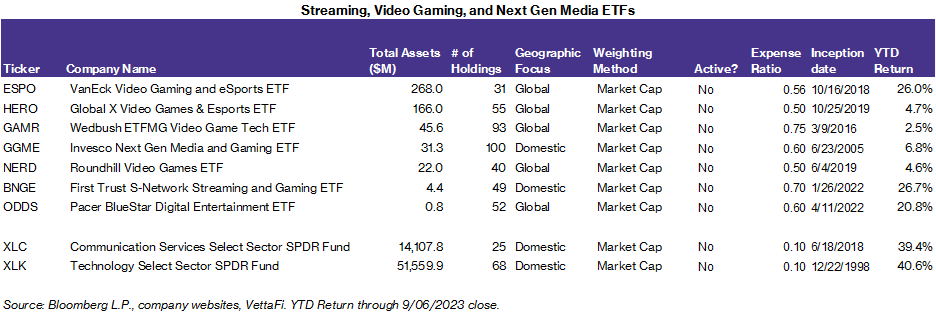

3. Streaming and Gaming – Next-Gen Media and Communications

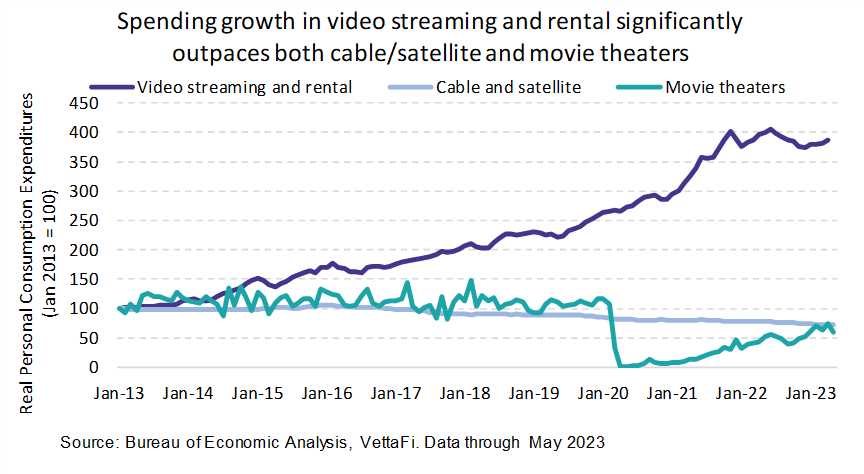

While people still value going to the movie theaters for special events (judging by the record-breaking numbers for Barbie and Oppenheimer weekend), watching movies at home has stayed a popular choice post-pandemic lockdowns. Consumers are now benefitting from shorter theatrical windows and possibly too many streaming choices, like Netflix (NFLX), Max (WBD), and Disney Plus and Hulu (DIS) which have been growing market share relative to both movie theaters and traditional cable and satellite TV. Even after lockdowns ended, there has still been a strong correlation with more devices and stronger and faster internet speeds. But these days consumers also value choice — including having a large library of movies or TV series to choose from rather than watching set programming on live TV.

On a similar note, the video gaming industry has also evolved to become more interactive and a social experience. All major consoles now offer online gaming in addition to the popularity of streaming video game services like Twitch (owned by Amazon). Online gaming also allows the user to access a broad catalog of games through a single source.

4. Metaverse – (Maybe) The Next Generation of Internet

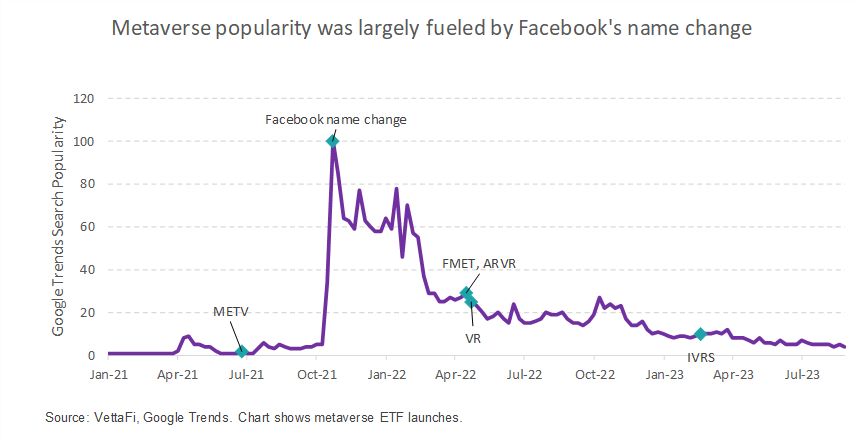

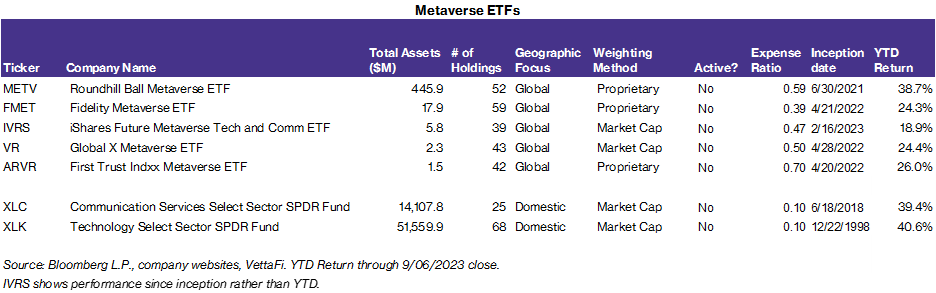

The concept of the metaverse has been around for years. But it became mainstream in 2021 when investors were buzzing about crypto, blockchain, and NFTs. Since everyone was under lockdown, the concept of the Metaverse opened up many new possibilities — virtual concerts, advanced interactive worlds, and fun social media avatars. Its popularity skyrocketed toward the end of 2021 when Facebook announced its name change to Meta. But the metaverse remained too conceptual — few pure-play public companies could prove themselves as a major player in the industry. Most metaverse companies (like Roblox) are essentially still video game companies. So while the metaverse may be a bigger deal in the future, these ETFs may have been early to the game. If you’re a believer in the metaverse, it may not hurt to have a small allocation in a metaverse ETF. The Roundhill Ball Metaverse ETF (METV) has performed about in line with broader tech and communications sector ETFs (~40% YTD) partially due to large holdings in Apple (AAPL), Nvidia (NVDA), and Meta Platforms (META).

VettaFi will host its Equity Symposium webcast on September 21, 2023, at 11 AM ET/8 AM PT. Free registration is available here. This event is eligible for CE credits.

For more news, information, and analysis, visit the Leveraged & Inverse Channel.