Summary

- Growing liquefied natural gas (LNG) export capacity in recent years has helped the U.S. become the world’s largest LNG exporter.

- U.S. LNG export capacity is on track to rise 80% by 2028 and could still see further growth.

- Energy infrastructure companies focused on natural gas and LNG producers are set to benefit from the anticipated long-term growth.

Global demand for liquefied natural gas (LNG) has grown over the past decade, prompting investment in new U.S. LNG export projects. Today’s note looks at the U.S. LNG projects currently under development, proposed facilities, and how investors can position to take advantages of long-term growth in LNG.

The US Is the Global LNG Export Leader

Demand growth for LNG over the past decade was driven by several factors. These include global economic development and a desire to shift away from coal for power generation. In 2022, demand for LNG spiked following Russia’s invasion of Ukraine and the subsequent Western embargoes on Russian natural gas supply (read more). Looking ahead, as Asia (and particularly China) moves away from coal and local natural gas production declines, global LNG demand should increase. LNG player Shell (SHEL) expects global demand growth to exceed 50% by 2040.

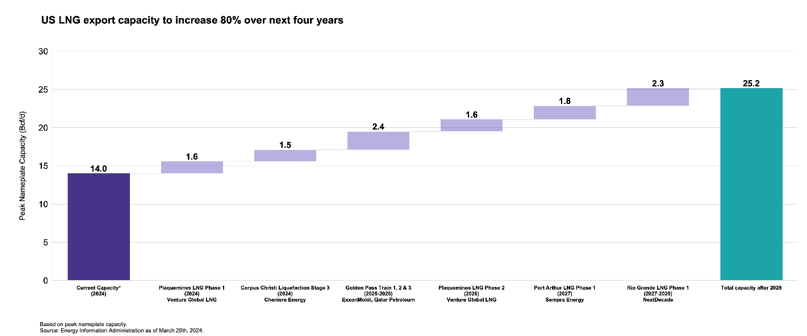

The rise in U.S. LNG production capacity over the past few years has positioned the U.S. as the world’s largest LNG exporter. In 2023, the U.S. exported 11.9 billion cubic feet per day (Bcf/d) of LNG on average, according to the U.S. Energy Information Administration (EIA). With ample and affordable natural gas supply, U.S. LNG projects are being developed and export capacity is set to rise (read more). As shown in the chart below, there are six LNG projects in the U.S. currently being developed that will increase capacity by 80% from 14 Bcf/d in 2024 to over 25 Bcf/d by 2028. U.S. LNG exports are constrained by production capacity. Therefore, growth depends on additional facilities coming online.

Two LNG projects are expected to be completed by year-end 2024: Phase 1 of Venture Global’s Plaquemines project in Louisiana and Cheniere Energy’s (LNG) Corpus Christi Liquefaction Stage 3 in Texas. Combined, the two projects will add 3.1 Bcf/d in incremental liquefaction capacity or around 22% of current levels. As these projects ramp, U.S. LNG exports are expected to increase by 18% in 2025.

(Click image to enlarge)

US Temporary Pause Has New Projects in a Holding Pattern

Several other projects are working toward a final investment decision (FID). That is the point at which a company formally commits to developing a project. It’s worth noting that signing long-term offtake agreements (i.e., signing up customers to buy the produced LNG) is a prerequisite for a project to reach FID. There are a handful of projects that are currently working toward FID, according to data from the EIA. That could bring even more liquefaction capacity online down the road.

However, the industry hasn’t gone without some challenges. In January, the Biden administration announced a pause on the issuance of new LNG export licenses to non-Free Trade Agreement countries. The pause should be temporary while the U.S. Department of Energy (DOE) conducts economic and environmental impact studies. That is not technically a ban on new LNG projects. But it does prevent the export to all but 21 select countries, and could delay new project FIDs.

The DOE conducted similar studies in 2018 and 2019 and afterwards continued issuing export licenses. Thinking positively, delays to new LNG project FIDs could prevent a near-term supply glut and push the growth story beyond 2028.

LNG Growth Benefits Midstream

In the U.S., new LNG facilities have been built along the Gulf Coast, given the advantages of deep-water ports and proximity to U.S. natural gas production. LNG projects largely source natural gas from the Permian basin (read more) and the Haynesville (read more). And midstream companies have been investing in infrastructure to connect production and export facilities with many touchpoints (i.e., fee opportunities) in between. Specifically, midstream companies gather natural gas from wells, process the gas into usable form, and transport gas to LNG facilities on the coast. Some midstream names operate the LNG facilities where natural gas is supercooled for export, directly participating in liquefaction. With long-term export contracts (typically 20 years), natural gas infrastructure is expected to be used for decades to come.

Midstream/MLP indexes that include gathering and processing (G&P) names, natural gas pipeline operators, and liquefaction companies are bound to benefit from steady LNG export growth. For the Alerian MLP Infrastructure Index (AMZI), G&P companies account for 24.1%, gas pipeline companies account for 24.5%, and liquefaction companies account for 4.0% of the index by weighting as of May 1, 2024. For the Alerian Midstream Energy Select Index (AMEI), G&P companies account for 30.6%, gas pipeline companies account for 38.2%, and liquefaction companies account for 5.8% of the index by weighting as of May 1, 2024. Additionally, the Alerian Liquefied Natural Gas Index (ALNGX) includes companies that are materially engaged in the LNG industry (read more).

Bottom Line:

U.S. LNG export capacity should see steady growth over the next four years based on projects under construction. New project FIDs could add to expected exports in coming years. Liquefaction and natural gas energy infrastructure companies will continue to benefit from growing U.S. LNG exports.

Related Research:

U.S. LNG Projects Advance Even as Global Prices Slump

Midstream Positions for Ballooning U.S. LNG Exports

Natural Gas Drives Permian Pipeline Growth

LNG Has Haynesville Humming – Benefits Midstream/MLPs

Global LNG Market Poised for Long-Term Growth

Canadian LNG Projects Advance to Meet Asian Demand

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX). ALNGX is the underlying index for the Roundhill Alerian LNG ETF (LNGG).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and LNGG, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, ALEFX and LNGG are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, ALEFX and LNGG.

For more news, information, and analysis, visit the Energy Infrastructure Channel.