Summary

- Six constituents in the broad Alerian Midstream Energy Index (AMNA) spent a combined $650 million on equity repurchases in 3Q24.

- While 3Q24 aggregate buybacks declined compared to 2Q24, total buyback spending for the first nine months of 2024 outpaced the same period in 2023.

- Over 85% of AMNA by weighting currently have a buyback authorization in place.

With midstream equities largely seeing strong performance this year, a handful of midstream C-corps and MLPs have been steadily repurchasing equity. Today’s note recaps buyback activity for midstream in 3Q24 and thus far in 2024. It also discusses the companies that could be active with buybacks in the coming quarters.

5 Names Continue to Drive Midstream Equity Repurchases

Six constituents of the Alerian Midstream Energy Index (AMNA) have been active with buybacks every quarter this year. These companies spent an aggregate $650 million on equity repurchases in 3Q24. Total buybacks in the quarter were down from the $1.02 billion spent in 2Q24 (read more) and $1.49 billion spent in 1Q24 (read more). However, aggregate repurchases are up year-over-year. Buybacks through the first nine months of 2024 total $3.2 billion compared to $2.4 billion for the same period in 2023.

Once again, Cheniere Energy (LNG) led buyback activity for 3Q24, repurchasing $282 million in common equity. Cheniere accounts for 60% of total midstream buybacks thus far in 2024, given its YTD buyback spend of $1.97 billion. In June, LNG added $4 billion to its repurchase authorization through 2027. Behind Cheniere, Targa Resources (TRGP) had the second-highest repurchase spend in 3Q24 at $168 million. That brings its year-to-date buybacks to $647 million through September 30.

Rounding out activity for the quarter, Enterprise Products Partners (EPD) and MPLX (MPLX) each spent $76 million on repurchases. Year-to-date through September 30, EPD has spent $156 million on buybacks, while MPLX has spent $226 million. Finally, EnLink Midstream (ENLC) repurchased $45 million. That brings its total buyback spend to $145 million through the first nine months of 2024.

With strong performance in midstream, particularly for natural-gas-focused C-corps, and healthy growth opportunities (read more), buyback activity has been fairly concentrated. Typically, one would expect more buybacks when stocks are lagging. Interestingly, all five companies had seen price gains YTD through September 30. But TRGP was the only one outpacing AMNA’s price return of 21.9%. MPLX and ENLC were slightly underperforming the index. And EPD and LNG were up just 10.5% and 5.4%, respectively, YTD through September 30. Notably, TRGP was up 70.4% as of September 30. Its $647 million in YTD repurchases are significantly higher than the $374 million spent for full-year 2023.

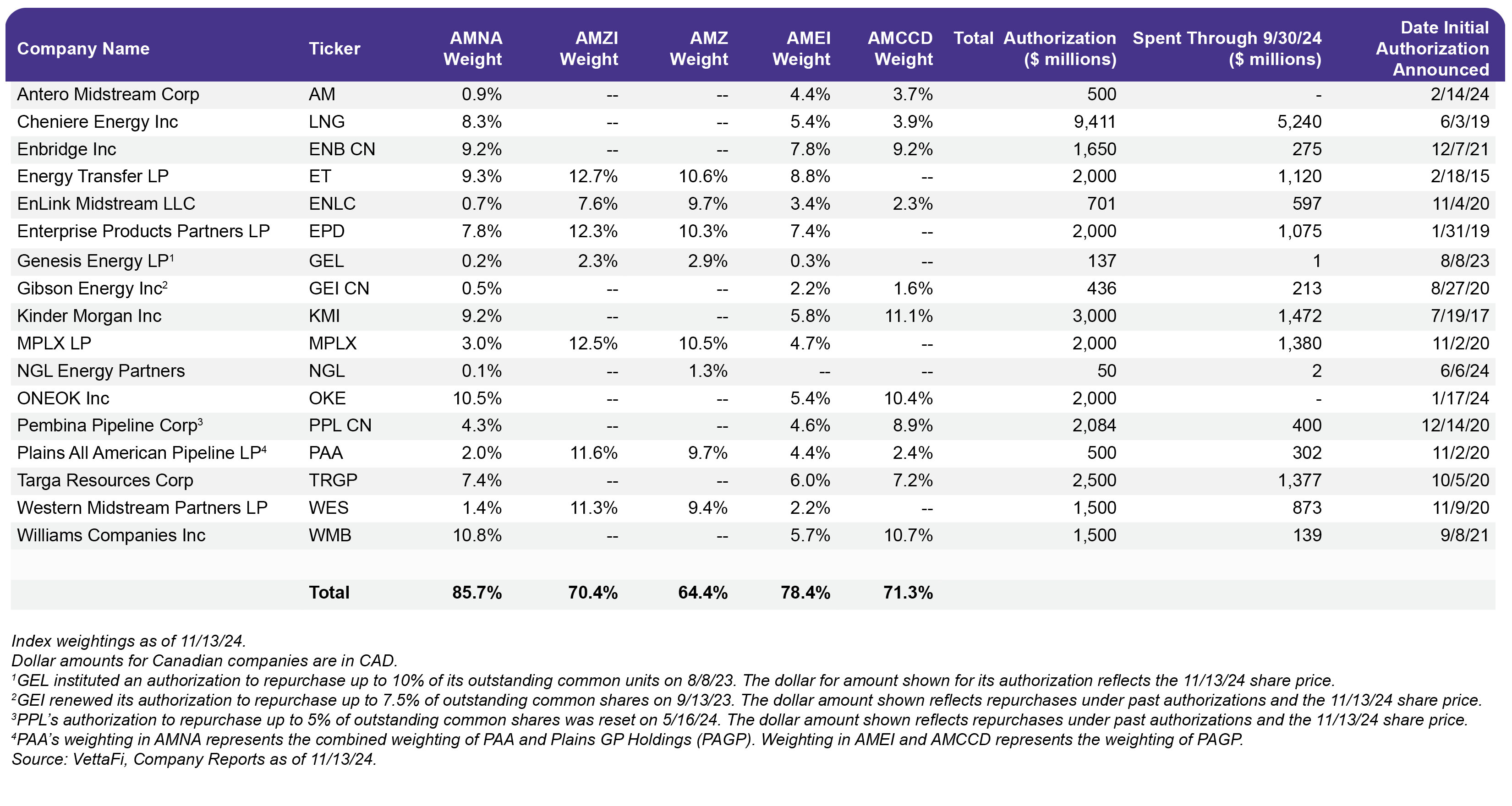

The table below shows the energy infrastructure companies with buyback authorizations and their total repurchases. It also includes each company’s weighting in AMNA, the Alerian MLP Infrastructure Index (AMZI), the Alerian Midstream Energy Select Index (AMEI), and the Alerian Midstream Energy Corporation Dividend Index (AMCCD). The bulk of the indexes by weighting as of November 13 have buyback authorizations in place.

Could Other Companies Come Off the Sidelines?

While five companies have been very consistent with buybacks this year, could others join their ranks? Clearly, buybacks continue to compete with other uses of capital. These include debt reduction, growth projects, and dividends. In midstream, most companies rightfully have a greater emphasis on dividend growth (read more) or would prioritize growth projects over repurchases. Buybacks can also depend on stock performance and valuations. That said, some companies have talked about the potential for buybacks going forward.

ONEOK (OKE) authorized a $2 billion buyback program in January 2024 but has not made repurchases yet. OKE announced the acquisition of Medallion Midstream and Global Infrastructure Partners’ interest in ENLC in August (read more). And management reaffirmed its intention to execute on the $2 billion authorization by year-end 2027. However, the company also has plans to reduce leverage toward its target of 3.5x in 2026 as growth projects are brought online.

Management of Antero Midstream (AM), which announced a $500 million authorization in February, has indicated it will consider buybacks once its leverage ratio is at 3.0x. AM ended 3Q24 with a leverage ratio of 3.1x, and management expects to hit its leverage target during 4Q24.

In its recent earnings report, Keyera Corp, (KEY CN) announced that the company intends to seek approval to authorize a new buyback program. That said, dividend growth and growth projects tend to rank as higher capital allocation priorities. Buybacks would be nice to have as a tool when opportunity arises.

Bottom Line:

While aggregate equity buybacks from energy infrastructure companies dipped in 3Q24 compared to the prior two quarters, activity remains strong, and year-to-date repurchases through September 30 have outpaced the same period in 2023.

Related Research:

2Q24 Midstream Dividend Recap: MLPs Drive Growth

Midstream/MLP Buybacks Rebounded in 1Q24

Don’t Be Spooked by Midstream Capex Creep

3Q24: Another Strong Quarter for Midstream/MLP Payouts

Examining MLP/Midstream Dividend and Buyback Yields

ONEOK Consolidating Again: Buying GIP’s Stakes in EnLink, Medallion

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AMCCD is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMNA, ENFR, ALEFX, and MMLP, for which it receives an index licensing fee. However, AMLP, MLPB, AMNA, ENFR, ALEFX, and MMLP are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMNA, ENFR, ALEFX, and MMLP.

For more news, information, and strategy, visit the Energy Infrastructure Channel.