Summary

- On a year-over-year basis, more than 90% of the Alerian Midstream Energy Index (AMNA) by weighting has grown their dividends. No AMNA constituent has cut its regular dividend since July 2021.

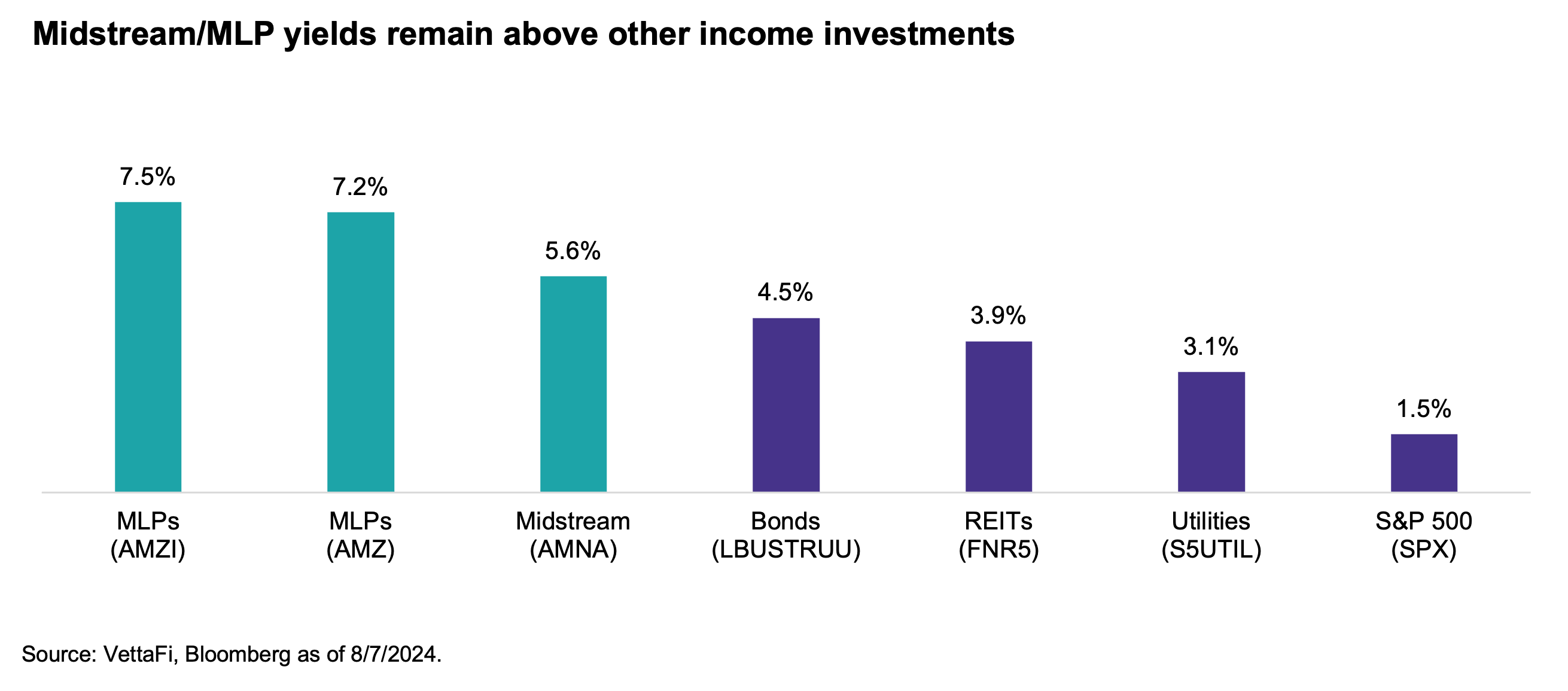

- Dividend growth enhances energy infrastructure’s already generous yields, which have been consistently above other income investments in recent years.

- The long-term outlook for continued dividend growth is constructive, with 3Q24 likely to provide more examples of dividend hikes.

Dividend growth has supported strong returns in the energy infrastructure space in recent years, as companies have been generating free cash flow and prioritizing returning cash to investors. Dividend growth has enhanced the already-compelling yields for midstream/MLPs relative to other income investments. Dividend growth trends remain intact, and the long-term outlook is constructive. Today’s note recaps 2Q24 midstream/MLP dividend growth, current yields compared to other income investments, and previews 3Q24 payouts.

2Q24 Dividends: MLPs Drive Sequential Growth

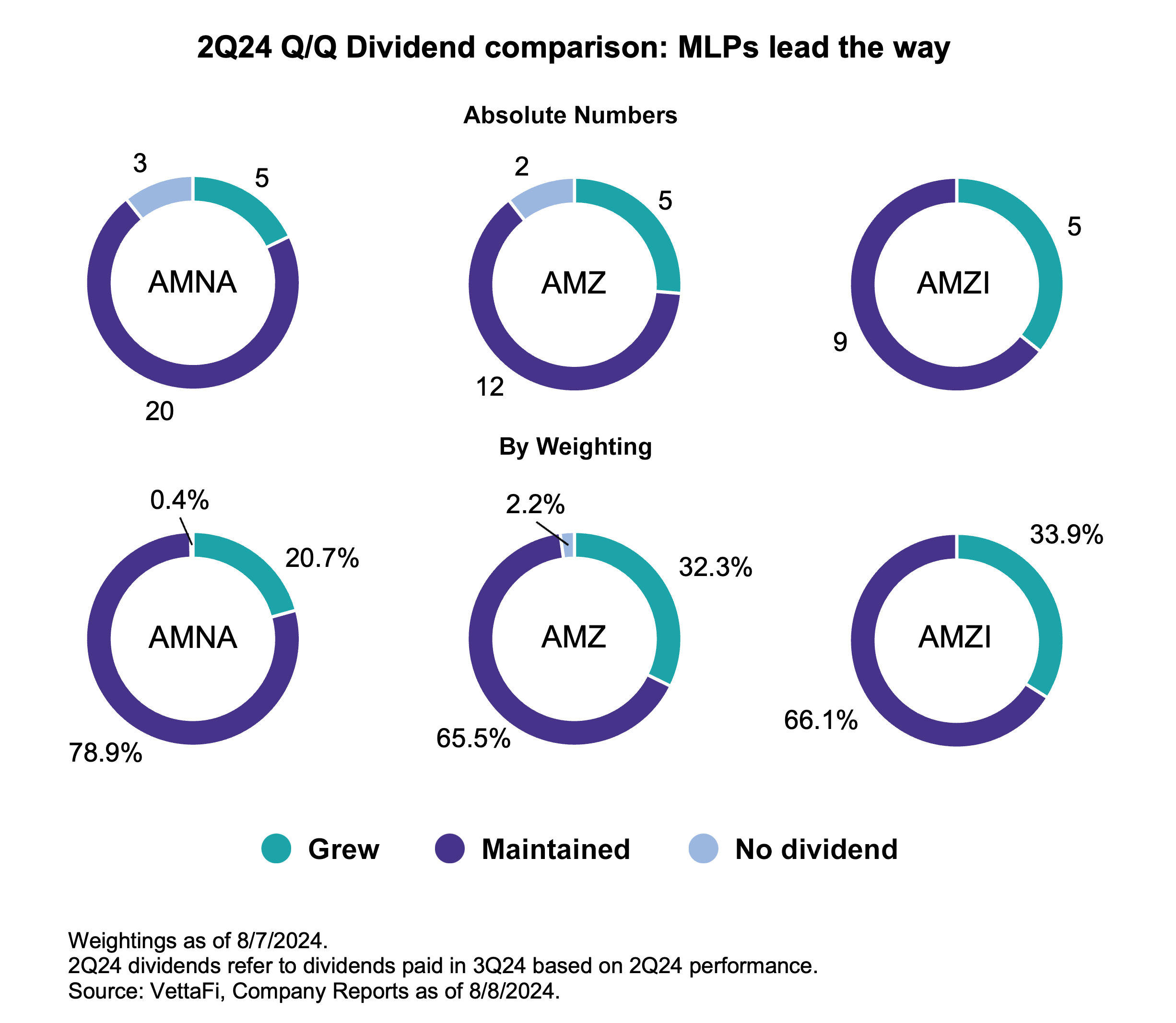

Dividend growth for this quarter was overall more modest compared to what was seen in the first quarter (read more), with a few names announcing low-percentage increases. This is typical for the second quarter given that companies tend to make annual increases with their fourth or first quarter dividends. Notably, there were no cuts this quarter, and no AMNA constituent has cut its regular dividend since July 2021.

For the second quarter, growth largely came from MLPs, including heavyweights Enterprise Products Partners (EPD) and Energy Transfer (ET). EPD grew its distribution by 1.9% to $0.525 per unit, while ET increased by 0.8% to $0.32 per unit. ET has a 3-5% annual growth target for its distribution. Turning to smaller MLPs, Delek Logistics Partners (DKL) and Global Partners (GLP) continued their streak of modest sequential increases, raising their distributions 1.9% and 1.4%, respectively.

The largest sequential percentage growth came from Hess Midstream (HESM), which increased its payout 2.5% to $0.6677 per share. Additionally, HESM reaffirmed its target to grow its distribution by at least 5% annually through 2026 in its 2Q24 earnings report.

The pie charts below show quarter-over-quarter changes to dividends for the Alerian Midstream Energy Index (AMNA), the Alerian MLP Index (AMZ), and the Alerian MLP Infrastructure Index (AMZI) by comparing 2Q24 payouts to those made for 1Q24. To be clear, 2Q24 dividends refer to dividends paid in 3Q24 based on operational performance in 2Q24.

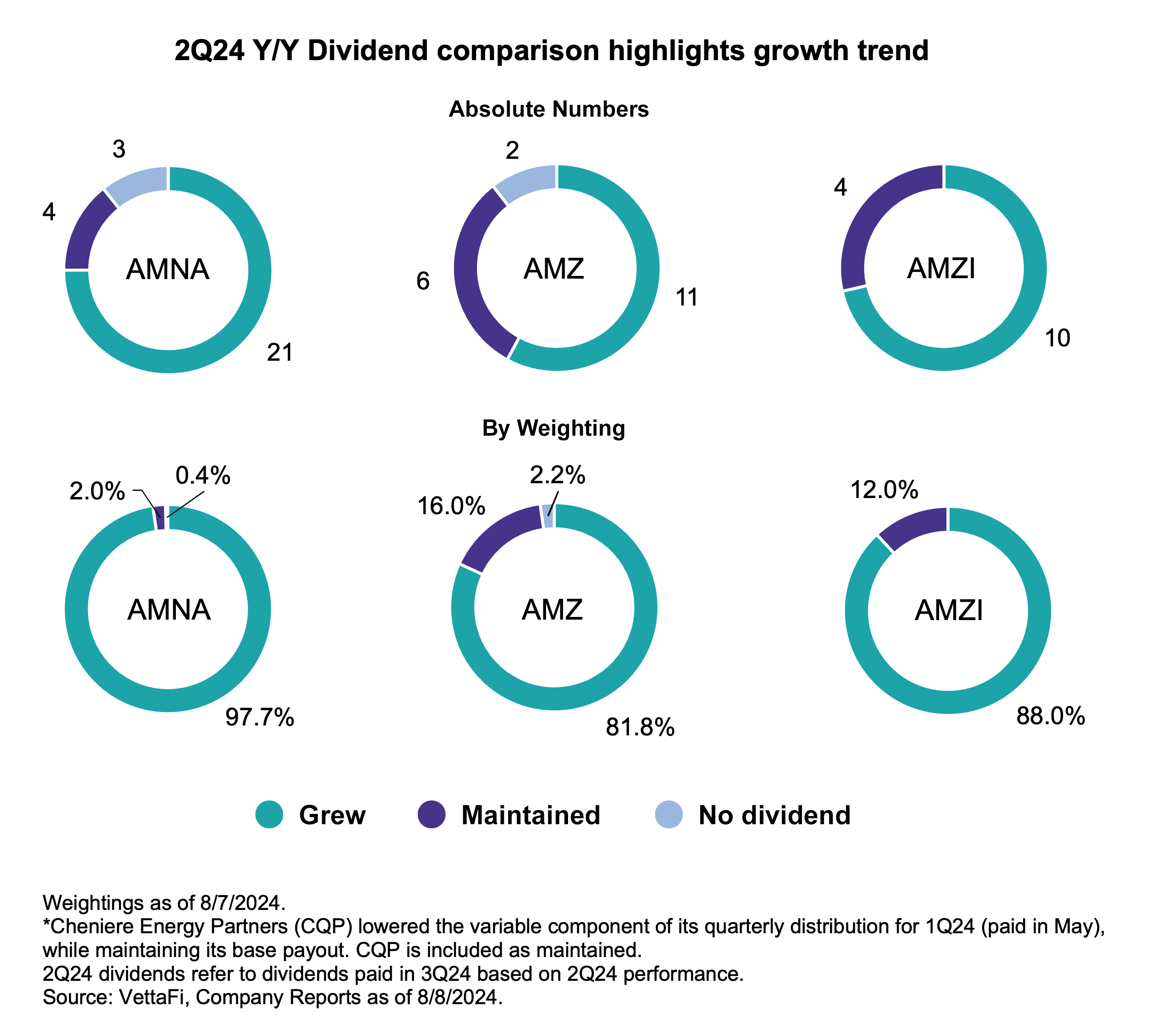

Year-over-Year Comparison Shows Bias Towards Growth

While there were only a handful of sequential increases this quarter, the year-over-year trends illuminate the strong growth that has been seen in the space. The majority of constituents in AMNA, AMZ, and AMZI have grown their payouts during the past year, representing over 80% of each index by weighting as of August 7, as shown in the charts below. For the broad North American midstream benchmark, AMNA, over 90% of the index by weighting have grown their payouts since 2Q23. Keep in mind that larger companies tend to more commonly grow their dividends and have higher index weightings. However, more names have grown their payouts than have maintained across all three indexes.

Growing Dividends Enhance Midstream/MLP Yields

The energy infrastructure space is known for providing compelling yields compared to other income investments. Even with strong performance in recent years, midstream yields remain above income investments like bonds, REITs, and utilities as shown in the chart below. With the Federal Reserve forecasted to cut rates this year, midstream/MLP yields represent an attractive option for income-seeking investors (read more). The positive dividend trends discussed above can add confidence to midstream/MLP payouts, and dividend growth is expected to continue as companies largely generate free cash flow.

Previewing 3Q24 dividends.

Although dividend increases tend to be more common with the first and fourth quarter payouts, announcements for 3Q24 could provide some notable examples of growth. Cheniere Energy (LNG) plans to increase its dividend by 15% to $2.00 per share as announced in June. The planned dividend raise accompanied an increase in LNG’s share repurchase authorization by $4 billion (stay tuned for our quarterly buyback update). Genesis Energy (GEL) will increase its distribution by 10% with its 3Q24 payout in November. GEL has maintained its payout at $0.15/unit since cutting in 2020.

While the company has not provided guidance, MPLX (MPLX) has increased its distribution by 10% with its third quarter payout for the last two years. As discussed on its earnings call last week, management views the distribution as the primary method for returning capital to investors. Per management, the combination of strong coverage, low leverage, and growing cash flows puts MPLX in an excellent position for future distribution growth.

Bottom Line:

Energy infrastructure continues to provide attractive yields, which have only been enhanced by broad dividend growth. The outlook for dividend growth remains strong as companies continue to generate free cash flow and prioritize returning cash to shareholders.

AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB) and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA).

Related Research:

1Q24 Midstream/MLP Dividends: Growth Story Intact

Can MLPs/Midstream Benefit from Lower Interest Rates?

Beyond 2024: Examining Multi-Year Guidance for Midstream

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMJB, MLPR, AMLP, MLPB and AMNA, for which it receives an index licensing fee. However, AMJB, MLPR, AMLP, MLPB, and AMNA are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMJB, MLPR, AMLP, MLPB and AMNA.