Summary

- MLPs/midstream are not particularly rate sensitive but could see some benefits as interest rates move lower.

- With fixed income yields moderating, investors may decide to look to MLPs/midstream for income when making new allocations.

- Rising interest rates were not a significant headwind for energy infrastructure, and falling rates are unlikely to be a significant tailwind, although select companies with higher leverage stand to benefit.

With recent market turmoil only adding to the likelihood of a Fed interest rate cut in September (and beyond), it is timely to consider the impact of falling interest rates on the MLP/midstream space. Although midstream is not particularly rate sensitive, there could be some modest tailwinds for companies as rates move lower. Today’s note discusses the impact of interest rates on MLPs/midstream as it relates to 1) competition among income-generating investments and 2) borrowing costs.

Midstream/MLP yields become relatively more attractive.

As investments with generous yields, MLPs/midstream compete with other income-oriented equities and bonds for investor dollars. With fixed income yields moderating, investors may decide to look to MLPs/midstream for income when making new allocations. The chart below shows current yields for MLPs/midstream relative to benchmarks for bonds, utilities, and REITs. Midstream MLPs are represented by the Alerian MLP Infrastructure Index (AMZI), and broader midstream is represented by the Alerian Midstream Energy Select Index (AMEI), which is 25% MLPs and 75% US and Canadian energy infrastructure C-Corps.

As shown above, yields for investment-grade bonds and high-yield bonds have come down noticeably from their October 2023 highs. Today, AMZI and AMEI offer yields above those of the investment-grade bond benchmark, while high-yield bonds still have a small edge over MLPs. Importantly, the majority of names in both AMZI and AMEI have grown their dividends over the past year based on dividends paid in 2Q24 (read more and stay tuned for our next quarterly dividend recap). Positive dividend trends add to confidence in MLP/midstream yields. Interestingly, the yield for the investment-grade bond benchmark is still better than those offered by REITs and utilities.

To be clear, MLPs/midstream are not bond substitutes and typically have greater risk as equities. For context, at the end of July, companies with investment-grade credit ratings represented 64.9% of AMZI and 77.9% of AMEI by weighting. Investors comfortable with equity investing and its risks may be more inclined to consider MLPs/midstream for income as bond yields moderate.

Lower borrowing costs can benefit companies with more debt.

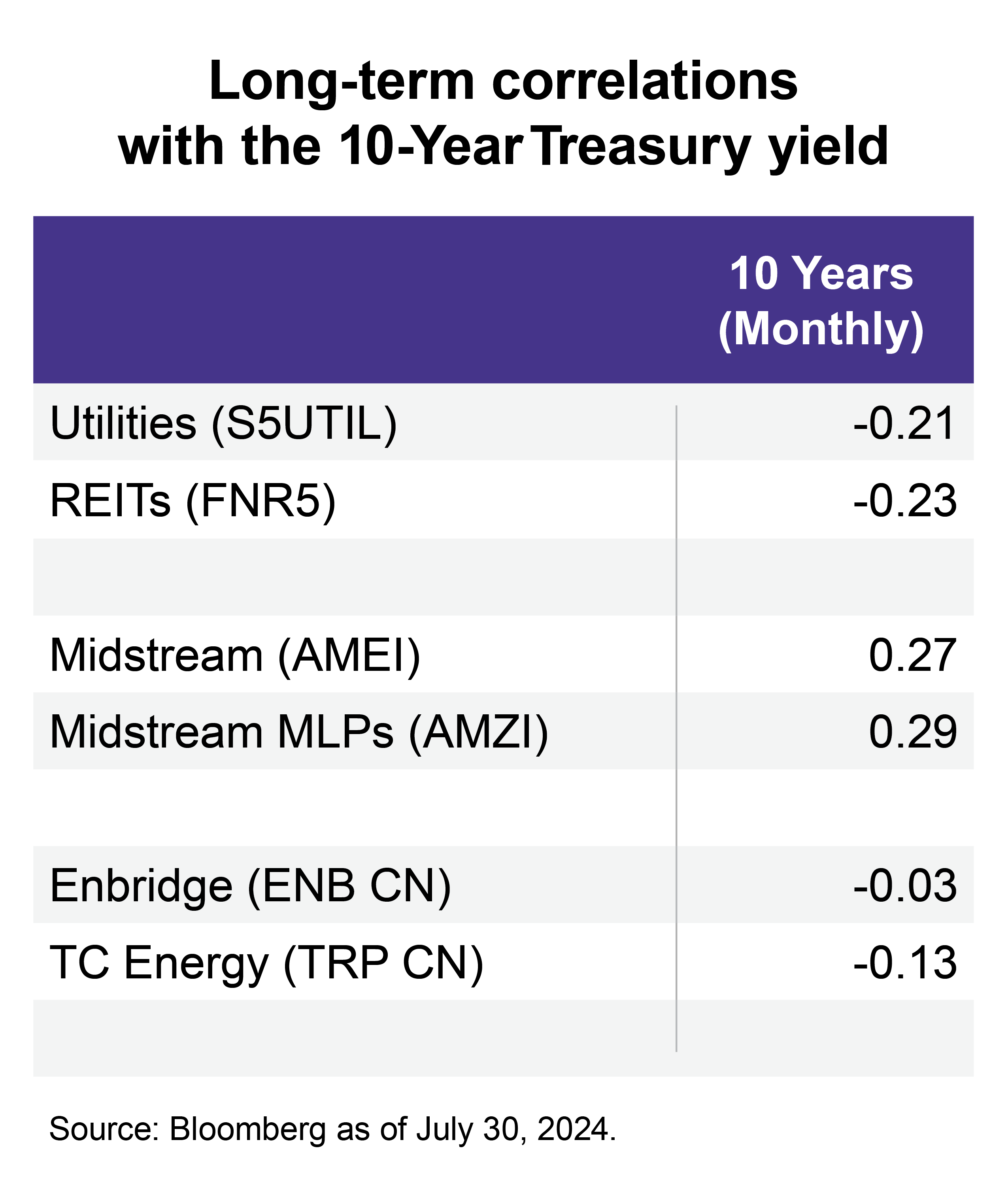

Beyond changing the competitive landscape for income investments, lower interest rates can be beneficial as it becomes cheaper to borrow money. This is important for capital-intensive businesses that rely heavily on debt, such as utilities. Utilities and REITs both have negative long-term correlations with the 10-Year Treasury yield, implying that their equities and interest rates tend to move in opposite directions. On the other hand, AMZI and AMEI have positive long-term correlations with the 10-Year Treasury yield around 0.3.

Interest rates are not a primary determinant of MLP/midstream performance and have arguably become less impactful for the space as balance sheets have improved. Since 2020, midstream capital spending has generally moderated, and companies have used excess cash flow to reduce debt. As such, rising rates were not a significant headwind for midstream/MLPs from 2021 through 2023 (read more), and falling rates are unlikely to be a significant tailwind. That said, lower borrowing costs could be marginally beneficial for the group in general and particularly helpful for two AMEI constituents – TC Energy (TRP CN) and Enbridge (ENB CN).

Relative to their energy infrastructure peers, ENB and TRP tend to have higher leverage due to greater capital spending and heftier project backlogs. Both stocks have a slightly negative correlation with the 10-Year Treasury yield as shown above, while other top constituents of AMEI have positive correlations. ENB and TRP’s relatively higher yields and the investing landscape in Canada may also contribute to their interest rate sensitivity.

From the end of 2021 until the 10-Year Treasury yield hit a relative high on October 19, 2023, ENB and TRP significantly underperformed AMEI, falling by 10.9% and 19.5% on a price-return basis, respectively, as AMEI gained 19.4%. TRP and ENB then outperformed AMEI as the 10-Year Treasury yield fell in November and December 2023. While lower rates have likely already helped their equity performance (the Bank of Canada cut in June and July), a further decline in interest rates could benefit ENB and TRP. Again, interest rates are just one factor in their equity performance.

Bottom Line:

For MLPs/midstream broadly, interest rates are not a primary determinant of equity performance. Rising rates were not a significant headwind for midstream, and lower rates are unlikely to be a significant tailwind. However, lower rates can provide some marginal benefits broadly, and companies with higher leverage arguably stand to benefit.

For an update on midstream in the context of the broader outlook on energy, please join our upcoming 30-minute LiveCast on Tuesday, August 13, at 12:30 p.m. ET (register here).

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

1Q24 Midstream/MLP Dividends: Growth Story Intact

Midstream/MLPs Resilient in Periods of Rising Rates

Midstream/MLPs Raising the Bar with Lower Leverage

For more news, information, and analysis, visit the Energy Infrastructure Channel.

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.