Summary

- Five constituents in the broad Alerian Midstream Energy Index (AMNA) spent a combined $1.02 billion on equity repurchases in 2Q24. Over 85% of AMNA by weighting currently have a buyback authorization in place.

- Aggregate buyback spend of $2.6 billion for AMNA constituents in 1H24 exceeded the 1H23 total of $2.0 billion.

- Companies have significant room under current authorizations to continue repurchasing equity, with a few names likely to start buying back shares in 2H24.

Over the past few years, energy infrastructure companies have been repurchasing common equity as an additional way to return free cash flow to investors. Buybacks have been a complementary tailwind to the strong dividend growth trends that have been seen. Today’s note discusses 2Q24 buyback activity for midstream MLPs and C-Corps, as well as the ample running room for additional repurchases.

Companies Drive over $1 Billion in 2Q24 Buybacks

Five constituents of the Alerian Midstream Energy Index (AMNA) repurchased common equity in 2Q24, totaling $1.02 billion. Coupled with 1Q24 buybacks of $1.49 billion (read more), AMNA constituents repurchased $2.6 billion in equity in 1H24 in total. That exceeded the $2.0 billion spent in 1H23. Comparing 2Q24 and 1Q24, activity was concentrated around similar names.

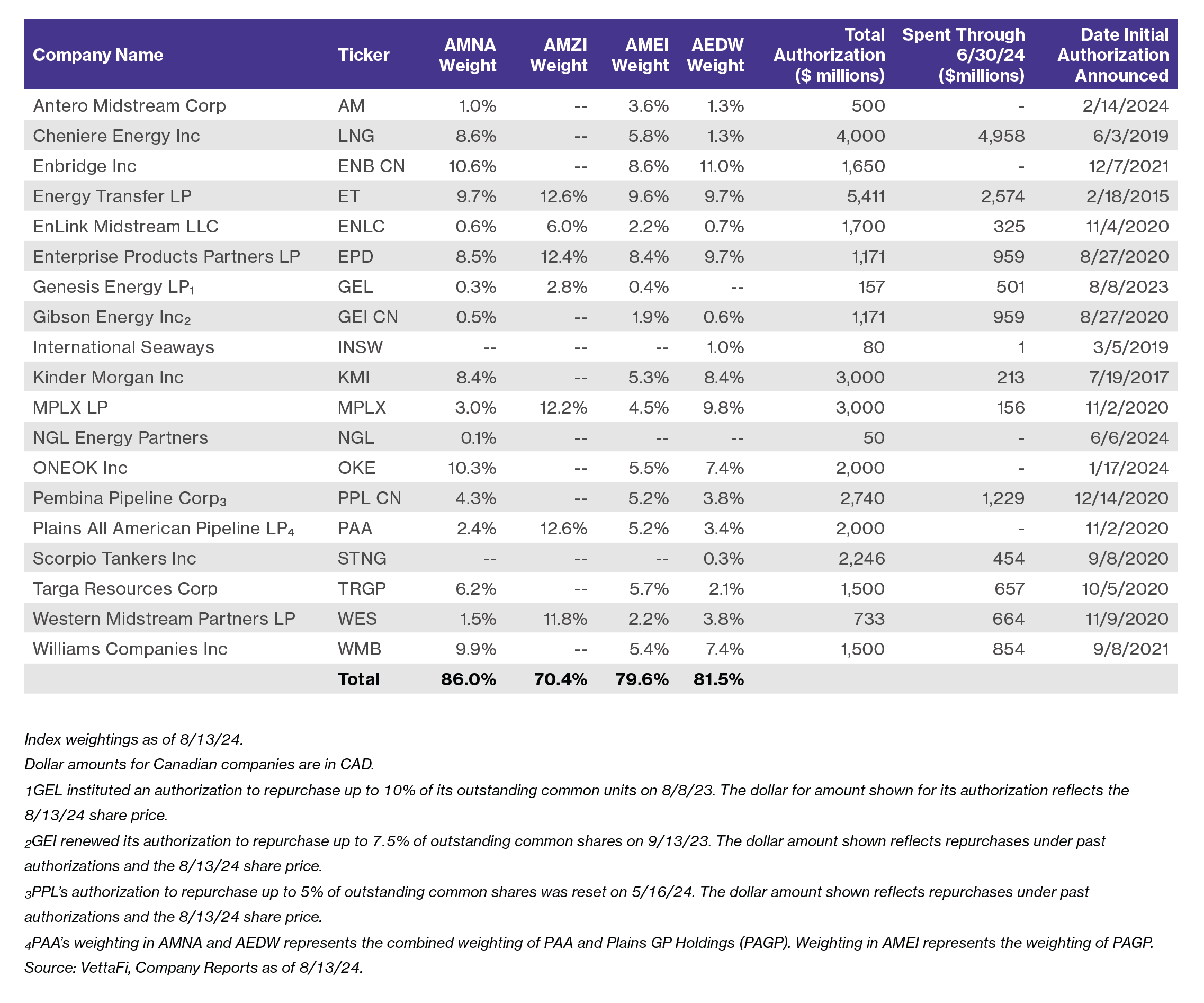

Cheniere Energy (LNG) remained active, repurchasing $496 million of its equity in 2Q24, after spending $1.2 billion in 1Q24. In June, Cheniere added $4 billion to its buyback authorization through 2027. Targa Resources (TRGP) set a quarterly company record by repurchasing $355 million in common equity in 2Q24. Alongside its earnings results, TRGP announced a new $1 billion repurchase program.

Other companies active with buybacks in 2Q24 include MPLX at $75 million and Enterprise Products Partners (EPD) at $40 million. Both matched their respective buyback spend from 1Q24. Similarly, EnLink Midstream (ENLC) repurchased $50 million during 2Q24, consistent with its 1Q24 activity. ENLC also added $50 million to its buyback authorization, bringing its authorization for 2024 to $250 million.

The table below shows the energy infrastructure companies with buyback authorizations in place, how much each has spent on repurchases, and each company’s weighting in AMNA, the Alerian MLP Infrastructure Index (AMZI), the Alerian Midstream Energy Select Index (AMEI), and the Alerian Midstream Energy Dividend Index (AEDW). More than 70% of the indexes by weighting as of August 13 have buyback authorizations in place. Five names have spent over $1 billion on repurchases since their authorizations were announced, though Cheniere stands out for nearly $5 billion in buybacks since 2019. Buybacks add to a compelling shareholder yield in the midstream/MLP space (read more).

New Companies Could Be Active with Buybacks in 2H24.

Looking ahead, companies with existing programs have plenty remaining under their current authorizations to continue making repurchases. Several names have also added to or established new buyback programs recently. In addition to the incremental authorizations from LNG, TRGP, and ENLC, ONEOK (OKE) announced a new $2 billion buyback program in January to be executed through 2029. Although OKE did not repurchase shares in 1H24 given an upcoming debt maturity in September, management expects to complete the buyback program over the coming years as discussed on OKE’s recent earnings call.

Antero Midstream (AM), which introduced a $500 million authorization in February, also has not yet made any repurchases. As discussed on its 2Q24 earnings call, AM management expects to utilize the buyback program in the second half of 2024 once it has reached its leverage ratio target of 3.0x. Additionally, Pembina Pipeline Corporation (PPL CN) renewed its buyback authorization for five percent of its outstanding common shares in May.

Bottom Line:

While aggregate equity buyback activity among energy infrastructure companies dipped in 2Q24 compared to 1Q24, activity remains strong, and 1H24 buybacks were above what was seen in 1H23. Looking ahead, companies have ample amounts remaining under buyback authorizations for future repurchases.

Related Research:

2Q24 Midstream Dividend Recap: MLPs Drive Growth

Midstream/MLP Buybacks Rebounded in 1Q24

Examining MLP/Midstream Dividend and Buyback Yields

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AEDW is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP) and the ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND, for which it receives an index licensing fee. However, AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND.

For more news, information, and analysis, visit the Energy Infrastructure Channel.