ONEOK (OKE) is acquiring Global Infrastructure Partners’ (GIP) interest in EnLink Midstream (ENLC), as well as private Medallion Midstream, in a pair of transactions valued at $5.9 billion in aggregate. Both transactions are expected to close in early 4Q24. Following the initial transaction, ONEOK plans to acquire the remaining public interest in ENLC in a tax-free transaction. For OKE, these deals provide beneficial integration with existing assets and enhance its Permian position into a one-stop shop for handling producers’ crude, natural gas, and natural gas liquids (NGLs).

Details

OKE is acquiring GIP’s managing member interest in ENLC for $300 million in cash and is acquiring the common units owned by GIP for $14.90 per unit, which represents a 12.8% premium to ENLC’s closing price on August 27. GIP owns 43% of ENLC’s common units. OKE will pay approximately $3.3 billion in cash for GIP’s interest in ENLC (common units and managing member interest).

Following the initial transaction, OKE plans to pursue an acquisition of the remaining publicly held units of ENLC in a tax-free transaction by exchanging ENLC units for OKE shares. Management did not provide a specific timeline for acquiring the remaining ENLC units.

Medallion Midstream is the largest privately-owned crude gathering and transportation system in the Midland Basin of the Permian. It is being acquired for $2.6 billion in cash.

Valuations

OKE is acquiring Medallion at a 6.3x multiple based on estimated 2025 EBITDA and including base run-rate synergies. OKE indicated the implied deal value for ENLC represents an 8.3x multiple based on estimated 2025 EBITDA and including synergies. Keep in mind synergies lower the multiples.

As of August 28, ENLC was trading at 8.7x using the Bloomberg consensus EBITDA estimate for 2025. ENLC had a 6.3% weight in the Alerian MLP Infrastructure Index (AMZI), which was trading at a 2025 EBITDA multiple of 8.6x using a weighted average and Bloomberg consensus estimates as of August 28. Within midstream, gathering and processing (G&P) businesses have typically traded at lower multiples than long-haul pipeline businesses.

Rationale and Synergies

The announced transactions with GIP build upon OKE’s acquisition of Magellan Midstream Partners last year (read more) and the smaller acquisition of NGL assets from Easton Energy earlier this year. The transactions with GIP are expected to be immediately accretive to earnings per share and free cash flow per share. The acquisitions add business and geographic diversification while taking run-rate annual EBITDA to approximately $8 billion. As the energy sector broadly consolidates, scale can be attractive and enhance competitiveness.

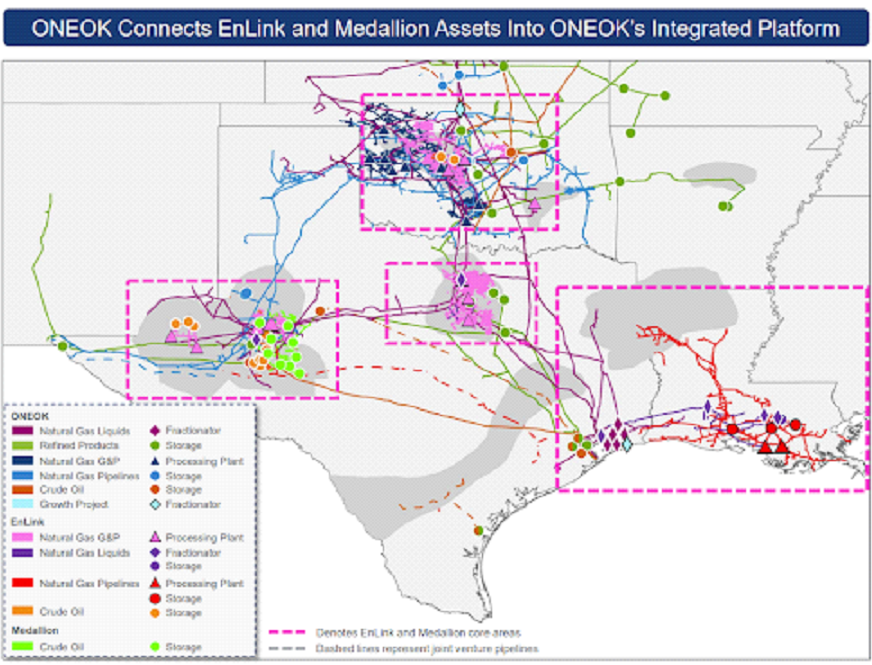

For ONEOK, the acquisitions of G&P businesses provide greater integration between the wellhead and OKE’s existing assets in the Permian and Oklahoma as shown below (and provide a new footprint in Louisiana). For example, Medallion’s gathering pipelines feed into OKE’s long-haul crude system and ultimately their East Houston crude terminal (legacy Magellan assets). A larger footprint in the Permian is clearly desirable given a positive outlook for ongoing growth from the basin. And the transactions increase OKE’s Permian EBITDA to ~$700 million annually with growth anticipated. With the acquisitions, OKE can provide a full suite of services to Permian customers across natural gas, crude, and NGLs, enhancing its competitive positioning.

Source: ONEOK’s Acquisition Presentation

OKE estimates annual synergies from the transactions of $250 million to $450 million in three years. Notably, the base case of $250 million is achievable even if the remaining public units in ENLC are not acquired.

Though there will be cost savings, management explained that the synergies are vastly weighted toward commercial opportunities, which they described as “feed and fill.” In short, the acquired assets help provide security of supply to OKE’s existing pipelines and can help fill OKE’s pipelines, providing operating leverage (i.e., ability to generate more fees on pipelines by increasing utilization). Some volumes flow from ENLK’s system onto OKE’s West Texas LPG Pipeline. But management indicated there is plenty more that could move from ENLK’s assets onto OKE’s pipeline. With an integrated system, OKE should be in a better position to compete for producer volumes as producers’ existing contracts expire.

Capital Allocation Priorities Remain Intact

On the call this morning, management reiterated ONEOK’s capital allocation priorities, including stated plans to grow the dividend by 3%-4% and to execute on the $2 billion buyback plan to be completed by the end of 2027. Management continues to expect dividends and buybacks to represent 75%-85% of free cash flow after capital spending.

While leverage (net-debt-to-EBITDA) at the end of 2025 is expected to reach 3.9x following the transactions, management sees leverage trending toward its 3.5x target in 2026 as growth projects come online. OKE sees the added scale and diversified portfolio of businesses with resilient cash flows supporting returns for investors. OKE expects to maintain its investment-grade credit ratings. And it still expects having to begin paying cash taxes under the alternative minimum tax in 2027.

Bottom Line

The transactions with GIP add scale, diversification, and greater integration to OKE’s asset base and mark another example of midstream consolidation. ENLC holders will have to wait for more color on a potential stock-for-unit exchange in the future. But ONEOK clearly intends to purchase the remaining interest in ENLC.

Related Research

How Consolidation Has Changed the Midstream Landscape

MLP M&A Monday: SUN Adding NuStar to Its Galaxy

Better Together: Energy Consolidation Continues

OKE Acquiring MMP: Valuation Nice, Taxes Add Wrinkle

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP and MLPB, for which it receives an index licensing fee. However, AMLP and MLPB are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP and MLPB.

For more news, information, and analysis, visit the Energy Infrastructure Channel.