Note: This article appears on the ETF Strategist Channel

By Innealta Capital

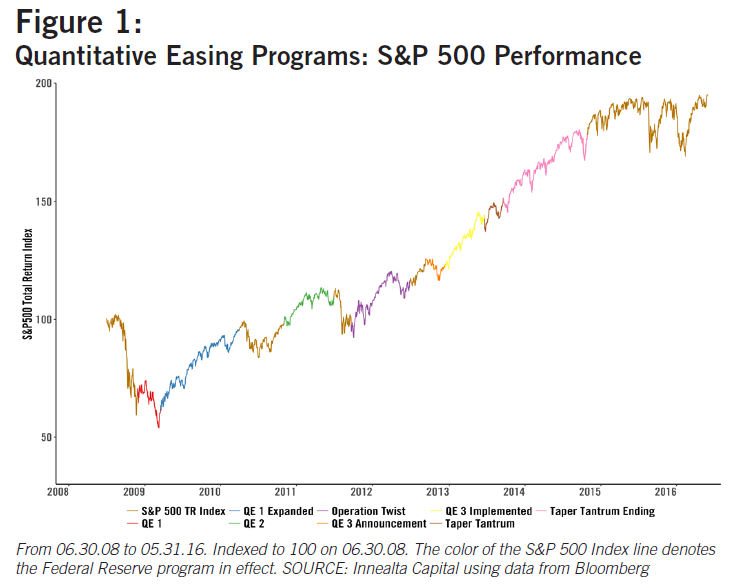

The Federal Reserve’s Quantitative Easing program (QE) has been a powerful tool for controlling domestic interest rates for the better part of a decade. The Federal Open Market Committee (FOMC) has sustained one of the most accommodative monetary policies in the history of U.S. financial markets. That accommodative stance, which started in late 2008, has been an important contributing factor to the record-high levels reached by the S&P 500 Index. Figure 1 shows the several attempts made by the Fed, during this market cycle, to push the U.S. economy toward recovery. However, at this point the current Fed’s target rate of 0.25% – 0.50% leaves little-to-no wiggle room to lend further support to potentially depressed equity markets in the future.

{kind=link}

During the second quarter of 2016, the Fed began hinting their desire to proceed on a path towards interest rate normalization. One should expect markets to respond to the eventual lack of continuous Central Bank support. It is important for investors to understand how equity markets will respond to such monetary policy regime changes. With equity markets at historically high valuations, the switch away from an accommodative monetary policy may communicate negative consequences to markets which have become used to Central Bank support.

Methodology

We define a U.S. contractionary monetary policy regime as an interest rate environment where the Federal Funds Effective Rate (FFER) increases 1.25% or more over a period longer than 12 months. Conversely, a U.S. accommodative monetary policy regime is one in which the FFER falls 1.25% or more over a period longer than 12 months. These restrictions (i.e., rate change and regime duration) constitute a conservative rules-based approach to identify different interest rate environments.

In practice, as shown in Figure 2, our method identifies local peaks and troughs, which in turn can be thought as the beginning of monetary policy regimes changes.

Using data from December 1969 to March 2016, we identify 15 unique periods: 7 contractionary (shaded areas) and 8 accommodative (non-shaded areas).

{kind=link}

Within each interest rate regime identified we calculate and compare the annualized excess rate of return over the risk-free rate, proxied by the 13-week Treasury bill, of U.S. equity markets (S&P 500 Index). We follow an identical procedure for international equity markets (MSCI World ex US Index). Finally, we compare the annualized excess returns of U.S. equity and international equity markets in rising (contractionary) vs. falling (accommodative) interest rate environments.

Results

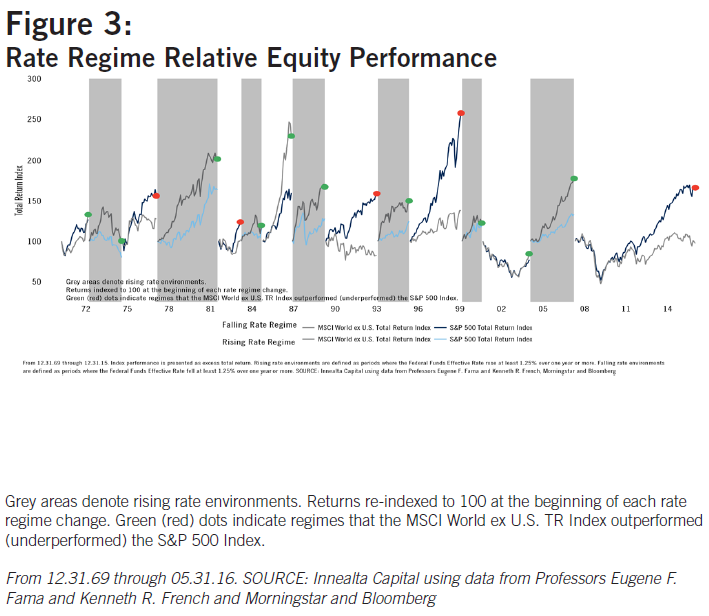

From Figure 3, U.S. interest rates appear to be negatively correlated to U.S. equity returns and positively correlated to international equity returns.

{kind=link}

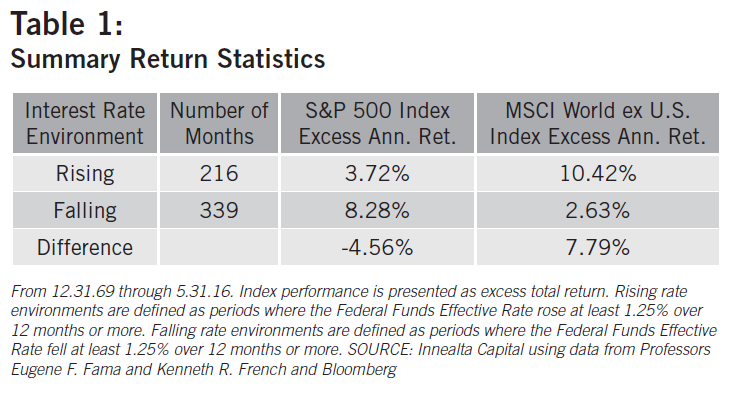

Table 1 summarizes our main findings; U.S. equity markets tend to perform better during falling interest rate environments than during rising rate environments. U.S. equity market excess returns are, on average, 4.56% higher during U.S. accommodative monetary policy regimes.

{kind=link}

International markets, however, exhibit a different behavior than U.S. equity markets. International equity market excess returns, on average, are 7.79% lower during U.S. accommodative monetary policy regimes.

Related: International Portfolios – How Thoughtful Diversification Can Reap Benefits

The results above show that there may be an opportunity for investors to benefit from monetary policy shifts by timely reallocating financial resources between domestic and international equity markets. Using history as a guide, investors could earn annualized excess returns of 10.42% by investing internationally during U.S. contractionary monetary policy regimes (vs. 3.72% in U.S. equity markets) and earn annualized excess returns of 8.28% by investing domestically during U.S. accommodative monetary policy regimes (vs. 2.63% in international equity markets).

Robustness

The study’s results are robust to a variety of methodology changes. For example, marginal changes to the thresholds used to identify rising and falling interest rate environments, shorter sample periods, and alternative equity and fixed income markets benchmarks don’t qualitatively alter the study findings.

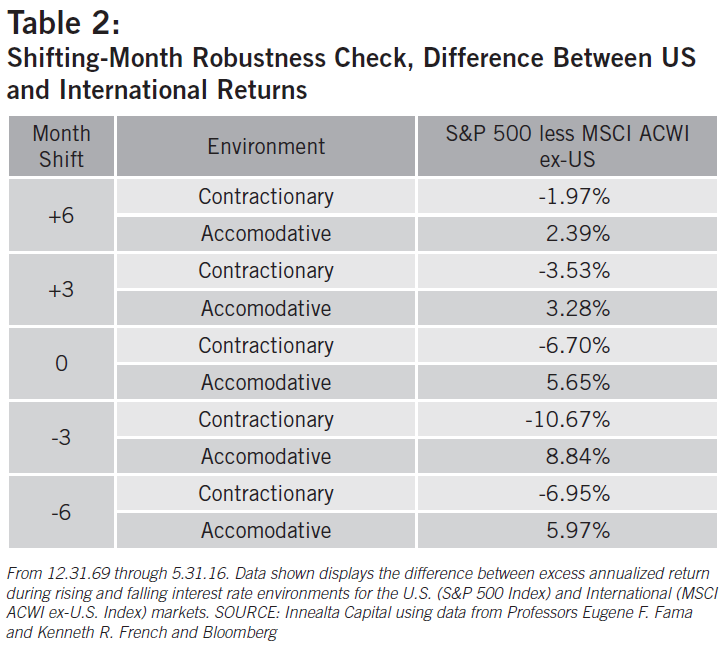

As an additional robustness check we introduced noise in the algorithm used to identify interest rate environments. Particularly, we allowed for a +/- 3 and 6 month window of misidentification, which is equivalent to modeling an investor being “too early” or “too late” to realize a monetary policy regime change.

Related: Searching for Yield to Bolster Near-Term Total Return

Table 2 displays the difference in returns between U.S. and international equity markets during contractionary and accommodative U.S. monetary regimes. From the table, it is clear that introducing a window of misidentification does not invalidate the results of the paper.

In other words, investors could still take advantage of monetary regime shifts to allocate their resources between domestic and international equity markets even when they are not accurate in identifying the precise time when those regime changes occur.

{kind=link}

Conclusion

In this study we showed that US equity markets outperform international equity markets during U.S. accomodative monetary policy regimes. Additionally, international equity markets outperform U.S. equity markets during U.S. contractionary monetary policy regimes. Considering the current state of our economy, investors may be facing a unique opportunity to benefit from the purported monetary policy shifts by timely reallocating financial resources between domestic and international equity markets.

This article was written by Dr. Vito Sciaraffia, Chief Investment Officer, and Aaron Steinman, Research Analyst, at Innealta Capital, a participant in the ETF Strategist Channel.

[related_stories]Disclosure Information:

The information provided comes from independent sources believed reliable, but accuracy is not guaranteed and has not been independently verified. Any security information, portfolio management or tactical decision process are opinions of Innealta Capital (Innealta), a division of AFAM Capital, Inc. and the performance results of such opinions are subject to risks and uncertainties. For more information about AFAM Capital, Inc. visit afamcapital.com.

The MSCI All Country World Index Ex-U.S. is a market-capitalization-weighted index designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. It includes both developed and emerging markets. The S&P 500 is an American stock market capitalization-weighted index that tracks the 500 most widely held stocks on the New York Stock Exchange or NASDAQ. It seeks to represent the domestic stock market by reflecting the risk and return of all large cap companies.

AFAM Capital, Inc. is an investment adviser, registered with the Securities & Exchange Commission and notice filed in Texas, California, and various other states. For more information, visit afamcapital.com. Registration as an investment advisor does not imply any certain level of skill or training. Innealta is an asset manager specializing in the active management of portfolios of ETFs.