THREE OPPORTUNITIES, ONE WITH MOMENTUM, TWO WITHOUT

By RiverFront Investment Management

In June 2018, we wrote a weekly called “Don’t Leave the Party, Just Start Drinking Water”. In our global balanced portfolios, this has meant:

- Maintaining stock to bond weightings within a few percentage points of long-term guidelines.*

- Keeping the bond portion of our portfolios invested in higher quality corporate bonds (as opposed to lower quality higher yielding bonds) and maturities more in-line with the Barclays Aggregate Index than before.

- Being more willing to own US Small-Cap stocks, Developed International Growth stocks, and Emerging Market stocks in our longer horizon portfolios.

Since we remain strategic bulls of stocks we are ‘still at the party.’ Due to the length and strength of the global stock rally since 2009, we are prudently ‘drinking water.’ That said, our portfolios have themes we think differentiate us from passive US and overseas stock indexes. Three such opportunities are discussed below.

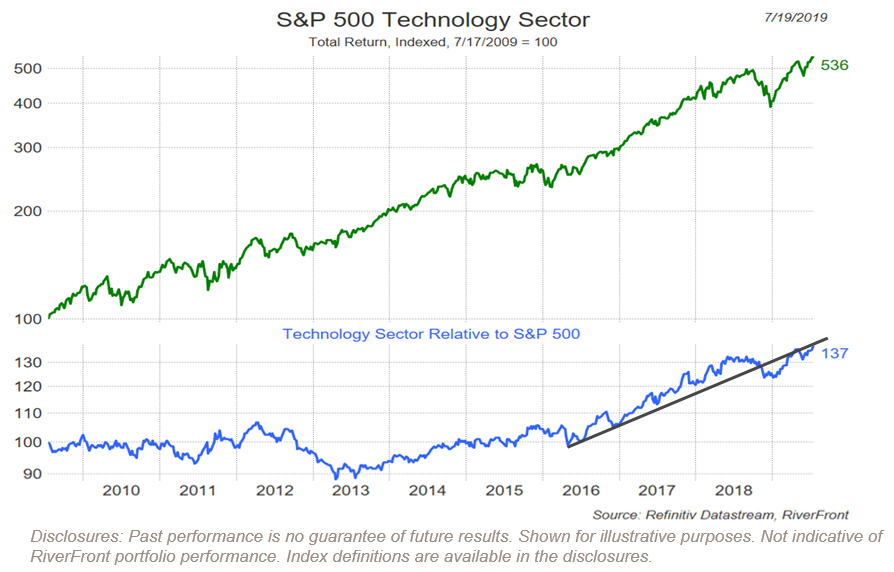

OPPORTUNITY ONE: US TECHNOLOGY STOCKS

We believe US technology stocks still offer reasonable value, and they clearly have absolute and relative price momentum.

We also like them because we believe there is still good business momentum in the sector. In judging the technology sector, we believe business momentum, especially growth of free cash flow, is the most important determinant of relative performance, and we still see strong momentum. Valuation, unless at extremes, has been a poor guide for technology stocks. We also recognize that US technology companies have left most of their global competitors far behind in the fastest growing areas of the internet era. We believe there are structural reasons for this. The US has provided the best environment for innovative risk takers to partner with risk capital. As a result, it has been the ‘location of choice’ for exceptional talent (both home-grown and imported), creating technological success stories in multiple industries such as retail, healthcare, entertainment, defense, energy, computing, and communications. We currently prefer industry groups like software and services and defense equipment; we also have a preference for medical devices in our longer-horizon portfolios.

OPPORTUNITY TWO: US SMALL-CAP COMPANIES

Our current investment rationale for owning small-caps is that the US economy is on sound footing, capital costs remaining low, and the opportunity for greater entrepreneurialism, as discussed above. Additionally, we recognize that when larger companies buy smaller ones, they often pay a significant premium at acquisition, which further enhances small-cap relative performance.

However, the price momentum is currently declining and small-caps are at the bottom of their recent range relative to large-caps (see parallel lines in chart above). This therefore is a different kind of opportunity, as the timing of a return to better relative performance is uncertain. We are currently invested in small-caps as an asset class and are evaluating the degree of our exposure given short-term uncertainties. Over the long-term, we think it is a question of when, not if, US smaller companies will see a sustainable uptrend in relative performance.

OPPORTUNITY THREE: CYCLICAL STOCKS

Investors are concerned about global growth and this has been reflected in the relative underperformance of cyclical sectors, both in the US and abroad. Additionally, stocks in Emerging Markets, Europe, Japan, Australia, and Canada which all tend to be more sensitive to the global economic cycle than the S&P 500 have suffered. As we learned in 2016- 2017, should the global cycle start to improve, even at the margin, these regions will do much better in our view. We believe such an improvement could occur over the next 6-12 months as policymakers around the world begin deploying additional monetary and fiscal stimulus programs.

This article was written by the team at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Small-cap companies may be hindered as a result of limited resources or less diverse products or services and have therefore historically been more volatile than the stocks of larger, more established companies.

Index Definitions (you cannot invest directly in an index):

CRSP ranks all NYSE companies by market capitalization and divides them into ten equally populated portfolios. Alternext and NASDAQ stocks are then placed into the deciles determined by the NYSE breakpoints, based on market capitalization. The series of 10 indices are identified as CRSP 1 through CRSP 10, where CRSP 10 has the largest population and smallest market-capitalization. CRSP portfolios 1-2 represent large cap stocks, portfolios 3-5 represent mid-caps and portfolios 6-10 represent small caps.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Standard & Poor’s (S&P) 100 Index — Constituents of the S&P 100 are selected for sector balance and represent about 59% of the market capitalization of the S&P 500 and almost 45% of the market capitalization of the U.S. equity markets. The stocks in the S&P 100 are generally among the largest and most established companies in the S&P 500.

Standard & Poor’s (S&P) SmallCap 600 Index – measures the performance of about 600 small cap companies and represents about 3% of the US equities markets.

Standard & Poor’s (S&P) Information Technology Sector Index — comprised of investable U.S. and Canadian equities in the Information Technology space.

Bloomberg Barclays US Aggregate Bond Index measures the performance of the US investment grade bond market. The index invests in a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States – including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities, all with maturities of more than one year.

RiverFront Investment Group, LLC, is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or expertise. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). RiverFront also serves as sub-advisor to a series of mutual funds and ETFs. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser.

Copyright ©2019 RiverFront Investment Group. All Rights Reserved. 906739