‘IN OUR VIEW, A BELIEF IN A SUSTAINABLE ECONOMIC RECOVERY IS CRITICAL FOR HIGHER STOCK PRICES OVER THE COMING YEAR’

By Riverfront Investment Group

You might be surprised to know the opening statement is not recent. It was taken from our Weekly View archives from June 2010. In that piece, we discussed the conditions we believed would lead to a sustainable economic recovery as we emerged from the Global Financial Crisis (GFC). Then, just as now, our focus was trying to find confirmation that the US economy was on more solid ground.

Today, the S&P 500 has recovered roughly 2/3 of the losses incurred since February 19th, similar to mid-2010. Economic data and earnings have yet to turn. We expect that they will turn, but over the next year the turnaround will need to be meaningful to justify current and ultimately higher stock price levels. Our portfolios are positioned to reflect our belief that we will see such an improvement.

Unlike in times of past financial crises, historians will not point to an asset bubble or a tech wreck, but rather a massive economic pause in the form of a global pandemic. In last week’s Weekly View, we presented the bull and bear cases for elevated market valuations against a depressed economic backdrop. Space constraints prevented in-depth comments on all the variables that we are watching, so in this week’s edition we take a deeper dive into a few more areas we believe will be important in shaping the response from the markets in the coming months.

We need to see a reversal in the unemployment levels – soon: We began 2020 with unemployment levels near historical lows. Today, headlines abound regarding COVID-19’s impact on the labor market and the fact that the shutdown has resulted in the highest number of job losses since the Great Depression of the 1930s. To put this in perspective, a study conducted by The Pew Research Center revealed that over 40% of US adults say that they or someone in their household has either lost a job or seen a reduction in pay as a result of the shutdown. There is no denying the magnitude of the unemployment crisis, so we are attentive to any signs of improvement in the employment data. We may have gotten one such signal in the form of the latest continuing claims report. Continuing claims refers to individuals who have filed for unemployment insurance and are still receiving benefits. A drop in the number of continuing claims suggests that people are finding jobs and no longer receiving benefits. Continuing claims fell by almost 4 million people during the week ending May 16. One week does not constitute a trend, but we are encouraged by this latest release and continue to look for signs of a bottom in the unemployment data.

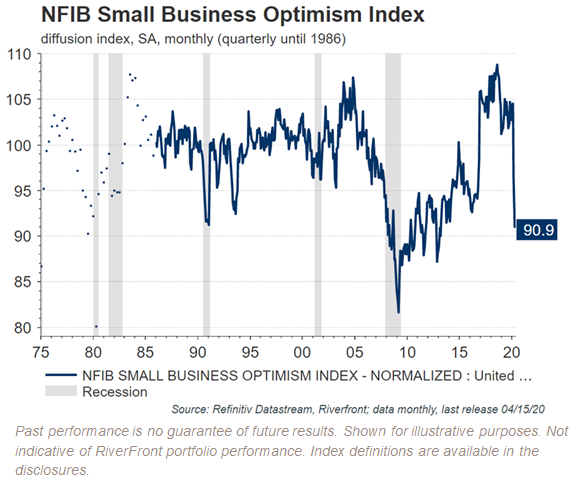

We need to see improving sentiment from both businesses and consumers: Sentiment is important because it often precedes actual business activity. Since the shutdown began, both business and consumer sentiment has plunged. However, while the recent index reading from the National Federation of Independent Businesses (NFIB) fell to levels not seen since 2001, the report was better than consensus expectations. Perhaps the most encouraging news in the report was the optimism expressed as business owners looked ahead six months and projected that business conditions will improve. We would like to see the index rise above 95 in the next 3-6 months. We believe this is important because small businesses are responsible for almost 50% of private-sector employment. Sentiment among home builders is also showing signs of improvement. Even though the National Association of Home Builders sentiment data remains in negative territory, the improvement in the May data relative to April was better than street expectations. CEOs from some home builders reported a pick-up in demand as stay-at-home restrictions are easing.

The all-important consumer sentiment data, while still mixed, is also showing improvement as it relates to consumers’ outlooks. In the most recent Conference Board consumer confidence report, the ‘expectations’ component rose while the ‘present situations’ data continued to decline. Prior to the COVID-19 crisis, consumer confidence was historically high. US consumers account for nearly 70% of GDP which means a robust recovery in aggregate economic growth will likely be dependent on a resumption in spending on apparel, travel, automobiles, and all the other goods that consumers normally purchase. Fortunately, it would appear that, the wherewithal to consume currently exists given that the personal savings rate in the US stood at 13.1% in March, is the highest level since the early 1980s. The cash is there, but it remains to be seen if the appetite for consumption will remain subdued or return to pre-COVID-19 levels.

We need to see a re-acceleration of strong housing market trends: As we noted above, the sentiment amongst home builders is showing signs of improvement, perhaps for good reason. In a recent update from the National Association of Realtors, their chief economist stressed his belief that while April pending home sales will be the lowest recorded during the crisis, he expects a rebound in the housing market in the summer months. He also cited an increase in mortgage applications in recent weeks which could be a sign of increased sales ahead. The combination of low mortgage interest rates, pent up demand, and high savings rates are all factors that could result in a reacceleration of the homebuying trends we were seeing at the start of the year.

We need to monitor the re-escalation of tensions with China: The relationship between the United States and China has clearly deteriorated over the past month. Throughout much of 2019, we saw market and economic impacts from trade tensions brewing between the leaders of both countries. While a trade deal was signed in the fall, the issues now are much larger than just trade. As the world has been focused on the pandemic, China has flexed both its military and economic muscles towards other countries in the region. One notable example is China’s bypassing of Hong Kong legislative process in enacting national security measures for the island last week. At this time, the US is considering punitive measures in response that could include sanctions, tariffs, and restrictions on Chinese companies – all of which could ultimately mean headwinds for the US and the global economy.

In conclusion, we acknowledge there is no road map for the way forward. In these types of times, we continue to follow our mantra of ‘process over prediction,’ leaning on our longstanding investment processes to guide our portfolio decision making. This incorporates both: risk management if conditions were to further deteriorate or increasing our allocation to equities if conditions continue to improve. Our last several trades involved the purchase of stocks, reflecting the improving environment and our portfolios are now slightly overweight equities.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the US dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the US dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the US and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-US securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Index Definitions: You cannot invest directly in an index

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

The National Federation of Independent Business (NFIB) Small Business Optimism Index is a composite of ten seasonally adjusted components. It provides an indication of the health of small businesses in the U.S., which account of roughly 50% of the nation’s private workforce.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID 1201787