Summary

- Higher interest rates have changed the playing field for income investors after more than a decade of lackluster yields. However, the outlook for rates is arguably uncertain.

- For income investors, it can be beneficial to look for yield that is independent of interest rates and Federal Reserve actions.

- Master Limited Partnerships (MLPs) have historically provided generous yields regardless of the interest rate environment, albeit with greater risk. MLPs are not bond substitutes but can help enhance the yield of an income portfolio while providing diversification benefits.

Fixed income investments started to provide meaningful income again last year and into 2023 as the Federal Reserve aggressively raised rates to combat inflation. A series of hikes brought the target federal funds rate from 0-0.25% at the start of 2022 to 5-5.25% today. After more than a decade of lackluster yields, higher interest rates changed the playing field for income investors.

However, those higher interest rates came at a cost. Rising rates contributed to losses for both bond and equity markets in 2022 (read more). Furthermore, elevated inflation has meant that real yields remain modest.

Higher interest rates are nice for investors putting money to work today in bonds or parking cash in money market funds paying upwards of 4.5%. However, what about the prior decade of low rates? What if the economy tumbles into a recession and rates fall again? Beyond a widely anticipated rate hike announcement this week, the outlook for rates remains uncertain. If rates fall, bond prices will rise, but reinvestment risk will be an issue.

For income investors, it can be beneficial to look for yield that is independent of interest rates and Federal Reserve actions. For example, Master Limited Partnerships (MLPs) have historically provided generous yields regardless of the interest rate environment. MLPs are able to offer attractive income due in part to their pass-through structure, which also allows for potential tax advantages (read more).

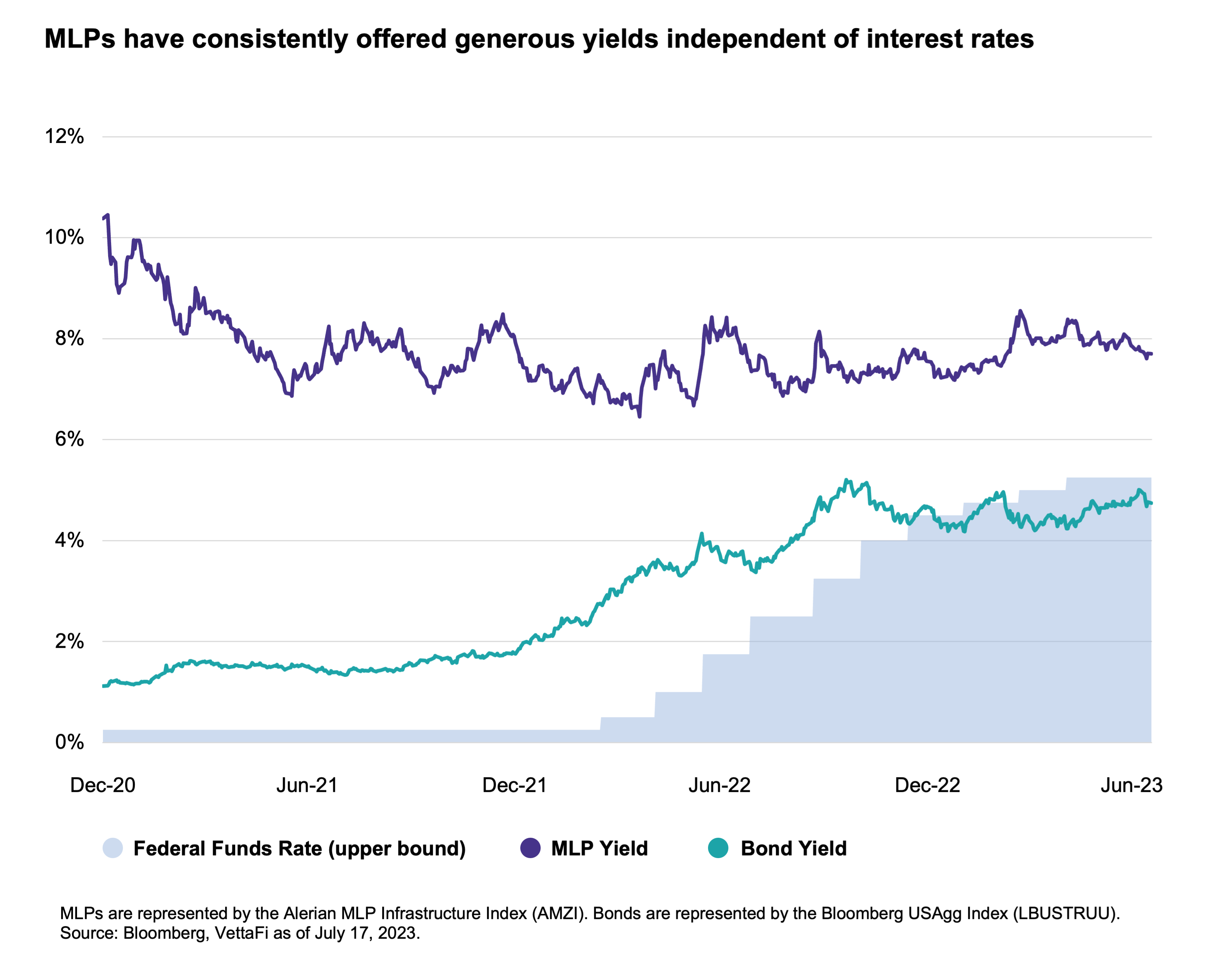

As shown below, when the federal funds rate was 0-0.25%, corporate bonds represented by the Bloomberg USAgg Index (LBUSTRUU) were yielding less than 2%. However, MLPs represented by the Alerian MLP Infrastructure Index (AMZI) were yielding around 8.0%. The ten-year average yield for the AMZI is 7.8% compared to 2.5% for corporate bonds.

MLPs’ higher income comes with additional risk. MLPs are equities and can trade based on sentiment for the energy sector. The MLP space came under significant pressure in 2020, particularly in the early phases of the pandemic when energy demand was temporarily decimated. Though some MLPs cut their payouts in 2020, there have been positive dividend trends in recent years and no cuts among AMZI constituents since July 2021.

MLPs provide compelling income but should not be characterized as a fixed income alternative or bond substitute. Rather, MLPs can help enhance an income portfolio with even a modest allocation. Typically, MLPs may account for 3-5% of an income portfolio depending on the investor’s objectives and risk tolerance. Notably, MLPs have a ten-year correlation with bonds of less than 0.1, providing diversification benefits as well.

Income is arguably easier to find today, but higher interest rates could prove fleeting. The income provided by MLPs, which does not ebb and flow with the federal funds rate, can be a helpful addition to income portfolios.

For more information on MLPs, visit our Energy Infrastructure Channel or join our upcoming webcast on August 9 at 2 p.m. ET, “How the US Energy Outlook Benefits Midstream/MLPs.”

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

For more news, information, and analysis, visit the Energy Infrastructure Channel.

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP and MLPB for which it receives an index licensing fee. However, AMLP and MLPB are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP and MLPB.