In addition to the three factors above that can support emerging market exposure, there are other region-specific themes that may lend support as well: https://www.etftrends.com/emerging-market-etf-opportunity-is-too-big-to-ignore/ . These relate to demographic/population forces and the increased portion emerging markets have become in relation to the global economy. On the flip side, that increases that impact EM has on the global economic cycle and its ability to speed up and slow down overall growth.

From an exposure standpoint, we look at broad and country specific holdings. When we’re talking macro support, we like to think in terms of broad exposure. Holdings like IEMG (iShares core MSCI Emerging Markets) and SPEM (SPDR Emerging Markets) can accomplish this objective. These are both low cost broad exposure that will take advantage of broad theme moves. IEMG has exposure to South Korea whereas SPEM does not.

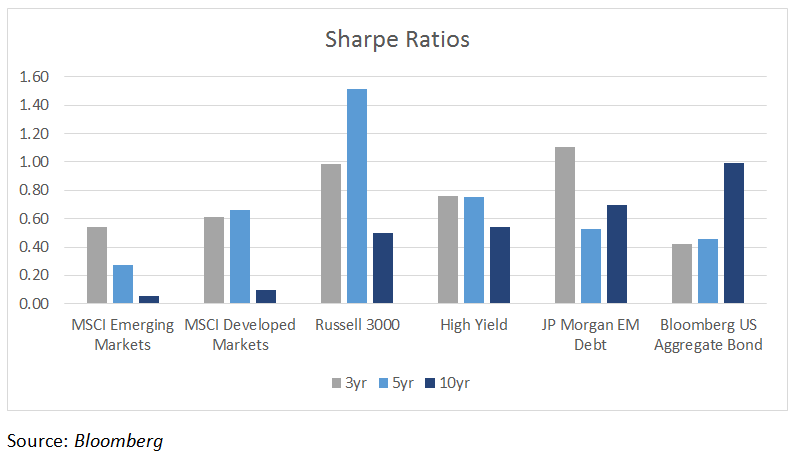

*Astor holds positions in SPEM and IEMG.

The Risks

With Emerging markets, there is always risks to the equation. We’ve seen some substantial ones in the past few years.

Global Growth – This is the biggest concern to any market exposure at this point. As discussed above, economic growth trends support market exposure currently. An acceleration in Emerging market PMI appeared to coordinate and push equity markets in EM. That’s why it is important to keep an eye on those data points and trends for clues as to when risk no longer is favorable. Interest rates, which have been everyone’s friend in recent years, are now creating some concern on the upside. That must be watched also.

China – The world’s second largest economy poses a risk if growth slows. In 2014 and 2015, worries about a China hard landing invoked substantial anxiety amongst investors, and markets reacted. Lending curbs are being implemented now to reduce credit risk, but will also slow the economy to its longer run growth target near 6%. This can be seen as positive long term, but slower growth does draw attention.

Political issues are a concern in these regions. We saw this in large part in Brazil last year as late spring/early summer saw a near 20% correction. Russia is also in this camp, albeit a lesser extent. The punch line is these are always a concern, but as long as overall global growth remains stable at minimum, that should minimize the impact should political issues arise.

Bryan Novak is the Senior Managing Director & Portfolio Manager at Astor Investment Management, a participant in the ETF Strategist Channel.