SUMMARY

- LNG export projects and power generation remain important drivers of natural gas demand growth with benefits for midstream. LNG demand is fairly straightforward, while power generation represents more of a wildcard.

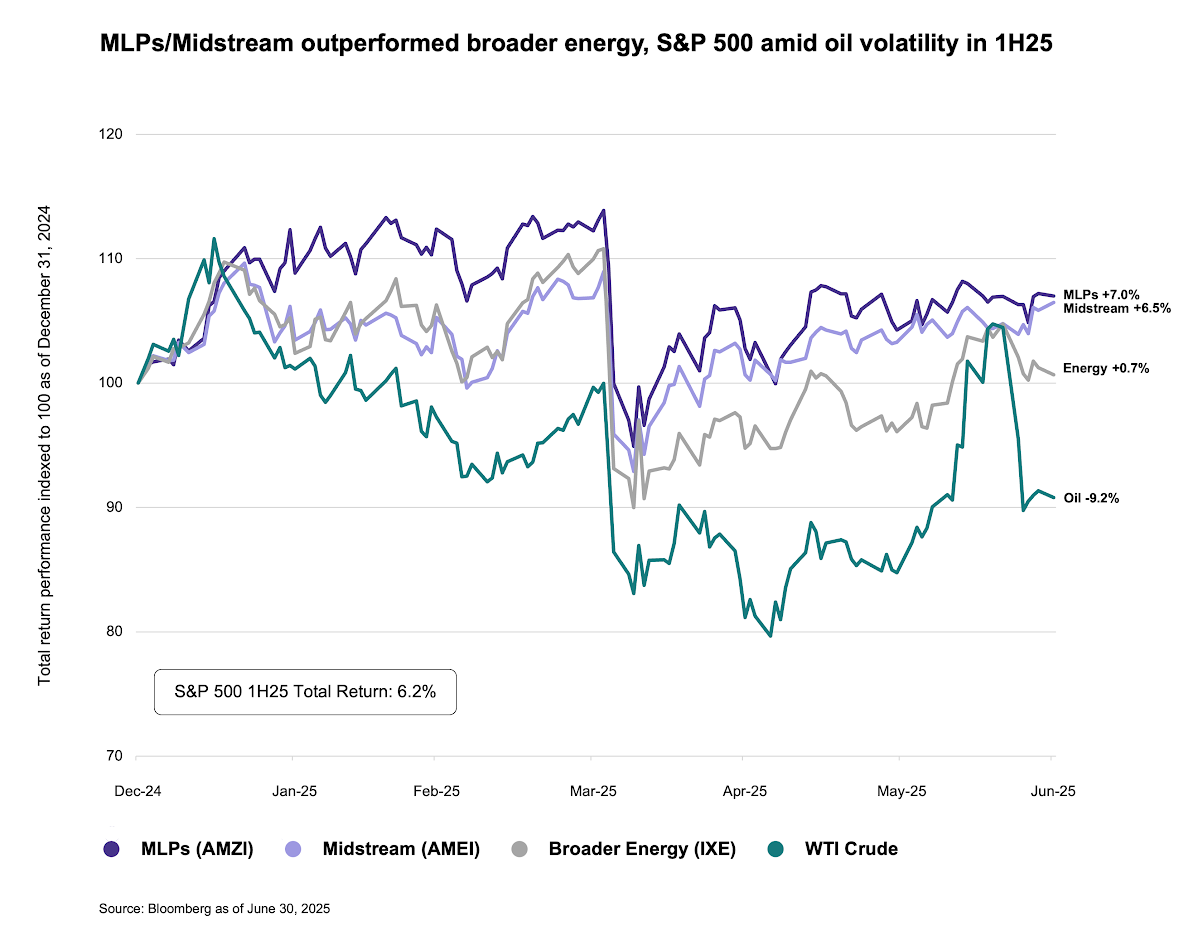

- MLPs and midstream outperformed the S&P 500 and broader energy, as oil prices fell 9% in 1H25.

- With a more supportive regulatory backdrop and a robust demand outlook for natural gas, natural gas pipeline projects in the northeast are catching a second wind.

With half of 2025 in the books, this note looks at some of the key developments for energy infrastructure so far this year. Amid significant volatility in oil and equities broadly, MLPs/midstream managed to outperform the broader market and the energy benchmark in 1H25. Midstream names largely reaffirmed financial guidance for 2025 alongside 1Q25 results, even as companies in other sectors were pulling forecasts amid tariff uncertainty. While there is plenty to discuss, this note covers four key topics impacting MLPs/midstream in 1H25. These include:

- The positive momentum in U.S. LNG export projects

- Ongoing focus on power demand implications for natural gas

- Oil’s volatility amid tariffs and geopolitical events and midstream’s defensiveness

- The revival of natural gas pipeline projects in the U.S. Northeast

U.S. LNG projects advancing.

With a supportive administration, more U.S. LNG projects are announcing sales agreements and advancing to final investment decision (FID). At FID, companies commit to a project and begin construction. Projects under construction are expected to increase U.S. LNG export capacity by over 60% by 2030.

Notable recent FIDs:

- Woodside Energy (WDS) reached FID for Louisiana LNG in late April. The initial phase with capacity of 16.5 million tons per annum (MTPA) is expected online in 2029.

- Cheniere Energy (LNG) announced FID for additional capacity at Corpus Christi and a debottlenecking project, representing a combined 5 MTPA.

Projects under development have also announced new sales agreements, with LNG a potential beneficiary of U.S. trade negotiations. In late May, NextDecade (NEXT) announced a 20-year sales agreement with Japan’s JERA for 2 MTPA for Train 5 at Rio Grande LNG.

LNG exports are expected to be the largest driver of incremental natural gas demand through the end of this decade (read more). While some midstream names directly participate, there are broader benefits. Additional export capacity will require more production, creating opportunities across the natural gas value chain. While there has been notable progress for U.S. projects in 2025, Canada’s first LNG facility recently loaded its initial cargo. Two additional LNG projects are under construction in British Columbia (read more).

Power demand for natural gas still in focus.

While LNG capacity is straightforward, the expected natural gas demand growth from power generation over the coming years remains unclear. U.S. electricity demand is set to grow meaningfully after being relatively flat for 20 years. That said, it is difficult to pinpoint the related natural gas demand, with data centers still a wildcard.

Natural gas pipeline companies came under pressure in late January after DeepSeek raised questions about data centers’ energy needs (read more). However, since then, midstream companies have continued to announce pipeline projects supporting power generation, including opportunities tied to data centers (read more). With a wide range of natural gas demand estimates tied to power generation, this continues to be an area of focus. Midstream natural gas pipeline announcements can serve as a potential catalyst.

Oil volatility drives swings in energy stocks as midstream remains defensive.

For midstream, the natural gas outlook is in focus as a notable growth driver. But oil prices still tend to dominate short-term energy sentiment. Oil prices this year have been marked by volatility stemming from geopolitics, unwinding production cuts from OPEC+, and economic concerns, including the impact of tariffs.

Energy was the best-performing sector in 1Q25 and the worst-performing sector in 2Q25. Amid oil volatility, MLP/midstream’s defensiveness has been on full display. As shown below, the Alerian MLP Infrastructure Index (AMZI) and Alerian Midstream Energy Select Index (AMEI) have handily outperformed the broader energy sector represented by the Energy Select Sector Index (IXE).

With U.S. oil prices hitting a four-year low in the high $50s per barrel in early May, producers quickly began to pull back on activity and drop rigs. However, production expectations for many large producers were little changed (read more). If oil can continue to hold above $60 per barrel, modest oil production growth in the U.S. likely continues.

Northeast natural gas projects revived.

With a more supportive regulatory backdrop and a robust demand outlook for natural gas, natural gas pipeline projects in the Northeast have caught a second wind. On its May earnings call, Williams (WMB) noted it was working on the Constitution pipeline, which would carry gas from Pennsylvania to New York, as well as the less complex Northeast Supply Enhancement (NESE) project. NESE would expand and upgrade the Transco gas pipeline system in Pennsylvania, New Jersey, and New York. Constitution and NESE had been canceled in 2020 and 2024, respectively, after permitting challenges.

Other pipelines have held open seasons this year to gauge customer interest. Boardwalk Pipelines held an open season for its Borealis expansion project, which would extend its Texas Gas Transmission system further into Ohio. DT Midstream (DTM) also held an open season for an expansion of the Millennium Pipeline in New York. As of June, the company was negotiating commitments and fine-tuning project design.

Finally, EQT Corp (EQT) plans to expand the Mountain Valley Pipeline (MVP), which came online in June 2024 and runs from West Virginia to Virginia. EQT is also working on MVP Southgate to extend the line into North Carolina.

In aggregate, these projects can help relieve some of the constraints that have typically faced Appalachian gas production (read more), while helping meet growing natural gas demand for power.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

U.S. LNG Dealmaking Picks Up With Benefits for Midstream

The Outlook for U.S. Energy Production & Midstream Impact

Rising Electricity Demand Needs Natural Gas & Midstream

Basin Basics: Appalachia Offers More Than Gas

Canada Enters LNG Export Market as First Facility Prepares for Shipment

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news information and analysis, visit the Energy Infrastructure Channel.