Summary

- DeepSeek news weighed on midstream names that have discussed supplying data centers, as the energy needs of data centers were called into question.

- DeepSeek represents efficiencies to AI development. But the continued growth in AI will likely still require significant data center capacity that will need natural gas. The potential demand impact remains unclear, with a wide range of estimates.

- The long-term outlook for North American natural gas demand growth is not solely based on data centers, and exports are a larger and more straightforward driver of incremental demand.

Excitement around Project Stargate was quickly replaced by worry, as China-based DeepSeek unveiled an open-source AI product that was brought to market faster and cheaper than comparable offerings. It also required much less energy. That raised questions around the energy needs for future data centers, with implications for natural gas demand. Natural gas pipeline companies that have discussed supplying data centers saw significant selling pressure last Monday. Today’s note discusses midstream’s positioning amid the DeepSeek news and the broader trends supporting natural gas demand growth.

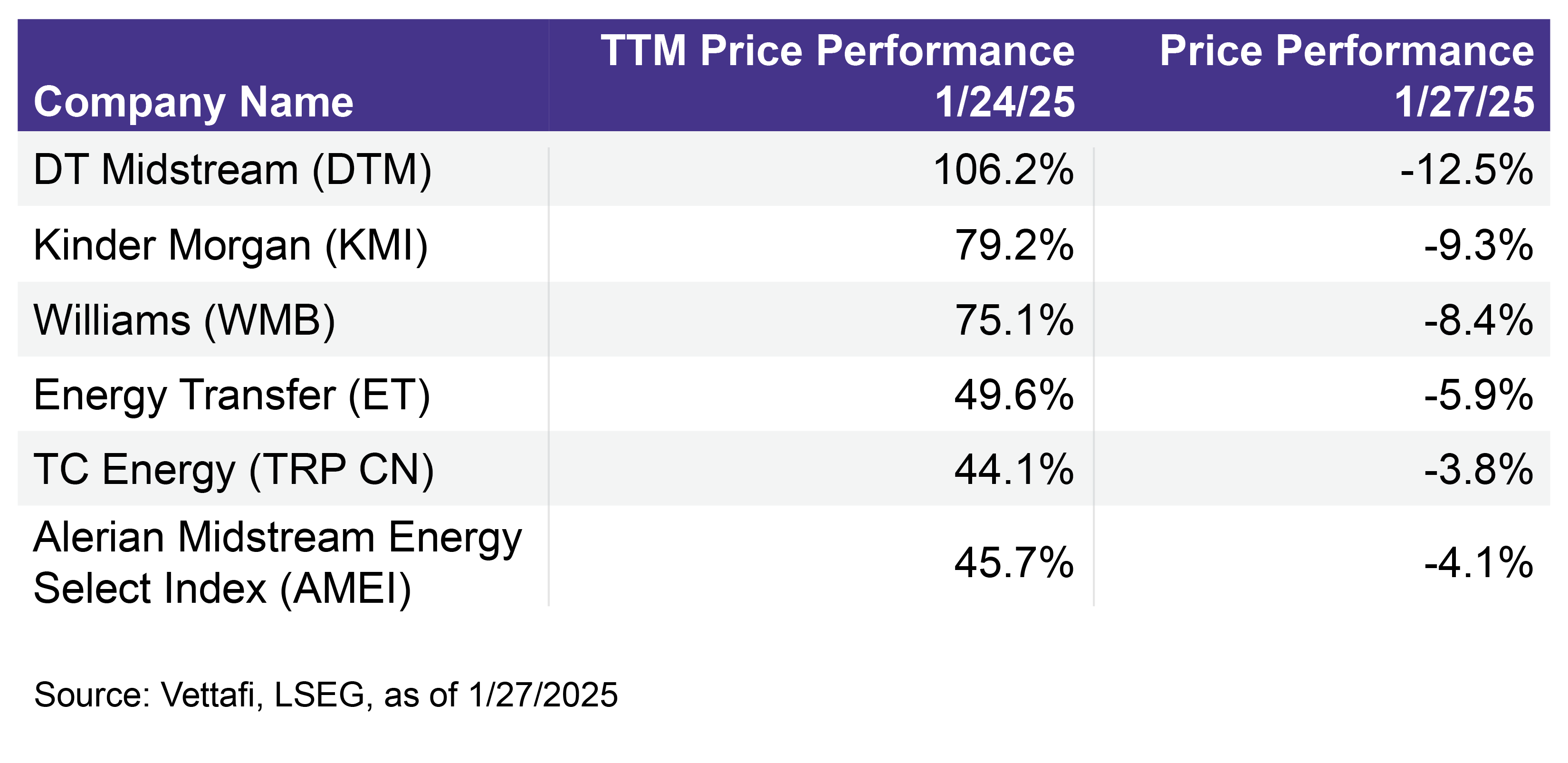

DeepSeek’s Impact on Midstream Performance in Perspective

A key theme in energy last year was the strengthening multiyear outlook for North American natural gas demand, supported in part by expected demand from energy-hungry data centers (read more). Companies focused on natural gas pipelines generally saw the strongest performance in 2024, given expected benefits from multiyear natural gas demand growth.

On Monday, January 27, concerns around the energy implications of DeepSeek caused a sharp sell-off for select names exposed to the data center theme as shown in the table below and compared with the Alerian Midstream Energy Select Index (AMEI). For context, AMEI ended January up 3.2% on a price-return basis.

In light of last week’s sell-off, there are a few key points for midstream investors to keep in mind. First and foremost, data center demand is just one component of the outlook for growing North American natural gas demand (discussed more below).

Secondly, estimates for natural gas demand from data centers have been very broad, ranging from 2 billion to 3 billion cubic feet per day (Bcf/d) to upward of 10 Bcf/d. Natural gas producer EQT (EQT) had previously estimated that coal retirements and an aggressive data center buildout could represent another 18 Bcf/d of natural gas demand by 2030, but their base case was 10 Bcf/d. In their December 2024 presentation, Kinder Morgan (KMI) estimated 3-6+ Bcf/d of additional demand from data centers by 2030 as its base case.

In short, natural gas demand from data centers has been and continues to be a wild card. We believe computing capacity will require more energy. Natural gas represents a cost-effective, relatively quick, and reliable solution for powering data centers 24/7. Natural gas also plays an important role in supplying backup power to offset the intermittency of solar and wind.

It is also important to note that midstream conversations with data center customers have been early-stage. Companies have referenced inquiries and discussions, instead of signed deals. As KMI management discussed on its 4Q24 earnings call, it is early in the data center trend.

Other natural gas opportunities related to power generation and liquefied natural gas (LNG) exports are more developed. KMI, for example, has announced four major new projects in recent months (GCX Expansion, Mississippi Crossing, Trident, and South System 4 expansion) representing over 5 Bcf/d of capacity. As another example, Williams (WMB) is advancing its Southeast Supply Enhancement project on Transco. The AI story has garnered significant attention and interest. But the long-term outlook for North American natural gas demand growth is not solely based on data centers.

Exports Remain the Largest, Clearest Driver of Incremental Gas Demand

Examining the outlook for natural gas in totality, demand growth is largely centered around LNG exports (read more). Specifically, North American LNG export capacity is set to increase by 13 Bcf/d by 2028 based on projects under construction in the U.S., Canada, and Mexico. The projects in Mexico rely on natural gas from the U.S. (read more). Sanctioning of additional LNG projects would only add to natural gas demand.

Beyond exports, other structural factors are expected to drive natural gas demand. These include growing electricity demand and coal plant retirements. In Washington, there seems to be a recognition that the U.S. will need more power, as well as improvements to the grid, based on comments from the Trump Administration. The need to grow baseload dispatchable power generation is especially important. This is due to global competitiveness, particularly around AI, continuing to ramp up. Industrial onshoring can also drive additional natural gas demand, with tariffs potentially adding to onshoring trends.

AI Advancements Likely Still Benefit Natural Gas

Even considering DeepSeek, as AI continues to develop, demand for data centers will likely grow. And that can benefit natural gas. Recently, the Stargate Project was announced. It will invest $500 billion toward AI infrastructure in the U.S. over the next four years. The details of the plan are yet to be announced. But incremental data center capacity under the Stargate project is already being built in Texas. Last week, Chevron (CVX) announced a new partnership with GE Vernova (GEV) and investment firm Engine No. 1 to develop reliable power solutions at scale for data centers running on natural gas.

Bottom Line:

DeepSeek news reinforced that natural gas demand related to data centers remains a wild card. But investors should not lose sight of the other structural drivers for growing natural gas demand — namely, exports.

AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Related research:

Midstream’s Natural Gas Outlook Continues to Strengthen

Who Will Need the Next Wave of LNG Export Capacity?

Midstream Connects US Gas With Growing Mexican Demand

For more news, information, and analysis, visit the Energy Infrastructure Channel.

VettaFi LLC (“VettaFi”) is the index provider for ENFR and ALEFX, for which it receives an index licensing fee. However, ENFR and ALEFX are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing or trading of ENFR and ALEFX.