Summary

- The Marcellus is the largest natural gas basin in the U.S. with competitive economics, while the Utica offers a promising oil opportunity.

- Pipeline solutions are helping alleviate historical takeaway constraints for gas production, most notably with the start-up of the Mountain Valley Pipeline in June.

- While it’s still early days, well results in the oil window of the Utica are promising, and production can benefit from existing infrastructure and proximity to refineries.

Appalachia is known for its natural gas production, predominantly from the Marcellus shale, which is the largest natural gas basin in the U.S. Appalachia also includes the Utica shale, which offers an emerging oil opportunity. This note discusses the unique characteristics of the Marcellus and Utica, how pipeline solutions are helping relieve constraints, and the underappreciated potential for oil production from the Utica.

Overview of Appalachia

Appalachia includes the Marcellus and Utica shale. The Marcellus spans portions of Pennsylvania, West Virginia, and Ohio, but natural gas comes predominantly from Pennsylvania, which is second only to Texas in gas production. The liquids-rich portion of the Utica is generally in eastern Ohio. Combined, the Marcellus and Utica accounted for about 36 billion cubic feet per day (Bcf/d) on average of marketed natural gas production in 2023, according to the Energy Information Administration.

Unique Characteristics of the Marcellus/Utica

Appalachia offers some unique characteristics in comparison to other basins. Importantly, production tends to be the most economic of the gas-oriented basins in the U.S. For example, EQT (EQT) estimates its free cash flow breakeven at $2 per million British thermal unit (MMBtu) following the acquisition of Equitrans Midstream. Put another way, EQT can generate free cash flow if NYMEX natural gas is at $2/MMBtu or above. Similarly, Range Resources (RRC) estimates 87% of its core undrilled Marcellus inventory at the end of 2023 has a breakeven below $2.50/MMBtu.

Beyond competitive economics, Appalachia is known to be pipeline-constrained. Recently completed projects are providing some relief (discussed more below), but pipeline takeaway capacity remains a limitation. Setting aside current production curtailments due to weak natural gas prices, pipeline constraints limit producer activity to a degree, which preserves drilling inventory for the future. RRC’s core inventory with a breakeven below $2.50/MMBtu represents 30 years of drilling inventory based on current activity levels.

Portions of Appalachia provide wet or rich gas, which contains more natural gas liquids (NGLs) or condensate, which is light liquid hydrocarbons. In addition to natural gas processing plants, there’s significant fractionation capacity within the basin that processes mixed NGLs into purity products (ethane, propane, butane, isobutane, and natural gasoline). NGLs can meet local demand or be exported (read more). For example, ethane can be exported through Energy Transfer’s (ET) Mariner West pipeline to Canada or transported to Shell’s (SHEL) petrochemical facility near Pittsburgh, which produces polyethylene used in plastics. NGLs can also move east through ET’s Mariner East system to its Marcus Hook terminal, which serves local customers and can export up to 400,000 barrels per day of NGLs.

Pipeline Solutions Helping

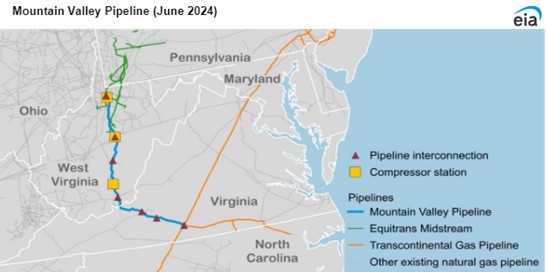

While production and reserves are significant, pipeline capacity out of Appalachia has historically been constrained, albeit recent project start-ups are helping. Most notably, Mountain Valley Pipeline (MVP) began operations in June 2024 with 20-year service contracts. The 300-mile, 2-Bcf/d pipeline, which was originally expected to be in-service in 4Q18, connects gathering systems in West Virginia to Transco’s Station 165 in Virginia. Williams’ (WMB) Transco is a 10,000+ mile natural gas system from Texas to New York, which handles nearly 20% of U.S. natural gas consumption.

Source: Energy Information Administration

EQT, which now owns MVP, having acquired Equitrans, plans to expand MVP to 2.5 Bcf/d by adding compression. Meanwhile, Williams is expanding Transco south of Station 165 by 1.6 Bcf/d to serve high-growth Mid-Atlantic and Southeast markets, where there are a growing number of data centers (read more). Transco’s Southeast Supply Enhancement project is expected to come online in 4Q27, with the best return of any large Transco expansion in WMB’s history.

Transco’s Regional Energy Access (REA) expansion was recently completed and provides 0.8 Bcf/d of capacity to help meet demand in Pennsylvania, New Jersey, and Maryland. A D.C. Circuit Court vacated the Federal Energy Regulatory Commission’s approval of REA on July 30, and WMB has indicated it will take the necessary legal and regulatory steps to ensure the project continues to serve its customers.

Pipeline capacity serving the Marcellus has not been easy to add. For example, the proposed Atlantic Coast Pipeline was scrapped in 2020, and restoration work began last year. MVP was aided across the finish line by an act of Congress through the support of West Virginia Senator Joe Manchin. These challenges make the existing pipeline in the ground that much more valuable and potential expansion projects, which are an easier lift from a regulatory standpoint, all the more attractive.

Utica Provides Promising Oil Opportunity.

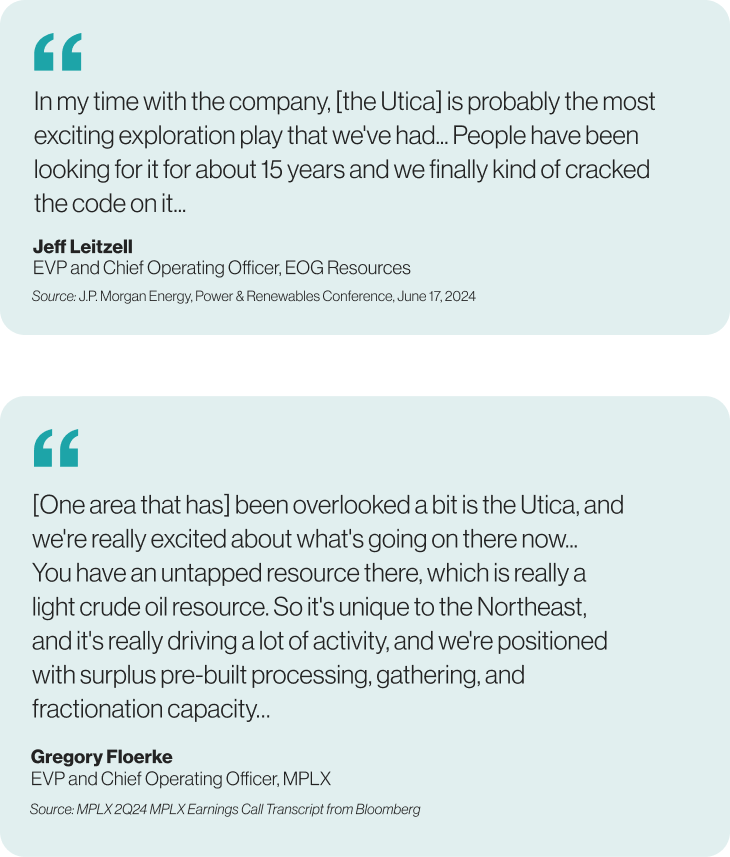

While Appalachia is known for its gas, Ohio’s Utica shale represents an emerging oil play. EOG Resources (EOG) has accumulated 445,000 net acres in the Utica, but has mainly focused on delineating 225,000 acres in the volatile oil window of the play. EOG plans to complete 20 net wells in the Utica this year, compared to six net wells last year. Results have been encouraging and are even competitive with the Permian basin.

On its August earnings call, EOG management noted that it is setting up local gathering systems and have been able to sell crude to local refineries. Marathon Petroleum’s (MPC) Canton, Ohio, and Catlettsburg, Kentucky, refineries are in the vicinity. EOG also highlighted ample processing and fractionation capacity in the area, noting that the Utica does not need a major infrastructure build-out.

MPLX (MPLX) has a significant gathering and processing footprint in the Marcellus and Utica, including fractionation capacity, thanks in part to its 2015 acquisition of MarkWest. Earlier this year, MPLX bought out Summit Midstream’s (SMC) interest in various gathering and processing joint ventures in the Utica for $625 million. Management is excited about the prospects of increasing activity in the Utica given their existing assets (see quote below).

Bottom Line:

The Appalachian basin offers attractive characteristics, including significant resources, competitive economics, and potential oil production in close proximity to existing refineries. On the other hand, pipeline capacity has been a challenge, though recent projects are helping.

Related Research:

- Midstream Investing in NGLs Amid Record Exports

- AI, Natural Gas & Midstream’s Emerging Opportunities

- Williams (WMB) and the Golden Age for Natural Gas

For more news, information, and analysis, visit the Energy Infrastructure Channel.