Bull vs. Bear is a weekly feature where the VettaFi writers’ room takes opposite sides for a debate on controversial stocks, strategies, or market ideas — with plenty of discussion of ETF ideas to play either angle. For this edition of Bull vs. Bear, Nick Peters-Golden and Karrie Gordon discussed the fundamentals for and against investing in Japan ETFs.

Nick Peters-Golden, staff writer, VettaFi: Hi Karrie! I’ve been looking forward to this one for a while because, with the debt ceiling, rising rates, and a looming recession, U.S. equities are stressful enough. Investing in Japan ETFs doesn’t just offer diversification; it also presents one of the strongest opportunities for portfolio returns in worldwide right now.

Karrie Gordon, staff writer, VettaFi: As an anime fan since my teenage years, I’m a big fan of Japan and much of its culture. When it comes to investing, however, I’m happier to sit on the sidelines, at least for now. There’s a lot of uncertainty currently regarding the direction of the Japanese economy and monetary policy. In a second half rife with risk, Japan’s outlook is just too nebulous for ETF investors, in my opinion.

Weakening Yen Spells Opportunity for Currency Plays

Peters-Golden: Let’s start with perhaps the strongest point in favor of investing in Japan ETFs right now: currency hedging. Specifically, the carry effect. The carry effect between Japan and the U.S. is more attractive than any other developed market pairing. The difference between interest rates in two currencies helps calculate the “cost of carry” for those currencies.

We can see the effect of the cost of carry in a pair of examples, thanks to the analysts over at WisdomTree Investments. In their example, when foreign interest rates rise higher than U.S. interest rates, like with Brazil, hedging currency exposure costs investors. In the inverse scenario, with, say, Japan, the carry effect pays investors to hedge currencies.

The formula accounts for the difference in rates, and with the Federal Funds Rate around 5% as of May, and Japan’s rate at -0.03%, that gap pays. Effectively, the carry effect paid investors 5.4% trading dollar-yen currency pair futures as of mid-May. The Fed’s rate hikes have taken rates so high so quickly, and likely for a long while, that Japan currency hedging looks to be a really promising opportunity.

Investors can access those currency benefits in the WisdomTree Japan Hedged Equity Fund (DXJ). DXJ has returned 24% YTD – almost double its Factset Segment Average. It’s also added nearly $300 million in net inflows over just the last month.

If the currency effect by itself isn’t enough, how about diversifying away from the dollar? S&P 500 earnings right now have a notable, potent weak dollar bias. How? Since the start of 2023, the dollar has weakened since spiking last year. In past cases, dollar weakness has preceded stronger S&P 500 earnings, while dollar strength goes before weaker earnings. Therein lies the weak dollar bias.

So, investing abroad without any hedging just adds to that weak dollar bet. True diversification means weakening the grip the dollar has on a portfolio. This adds to the case for a currency focus in Japan ETFs like DXJ.

The carry effect has helped drive DXJ forward, outperforming all but one other currency-hedged ETF YTD. Currency-hedged Japan ETFs, particularly, are flooring hedged-equity ETFs focused on other regions, like stagnant European equities, for example. Taken together, DXJ’s currency effect returns alone make the case for investors to up their Japan exposure.

The Real Cost of Weakening Currency

Gordon: Those are great points, and I’ve long been a fan of DXJ, but it’s still not enough to sway my stance. For several reasons, Japan isn’t an ideal investment for the near term, but let’s talk about currency. The Japanese yen depreciated to its lowest level in 30 years last October. It crossed the 150:1 threshold to the U.S. dollar and currently sits at ¥139 to the dollar. The yen depreciated in recent days on news the Fed could hike rates for longer. Bank of America analysts wrote in a note this week that the currency could continue to weaken through Q3 this year.

A weak yen is a double-edged sword for the Japanese export-reliant economy. Yes, it’s great for multinational corporations headquartered in Japan. These companies can and do capitalize on overseas profits that compound when converted to the yen.

For local companies and citizens, however, it’s predictably disastrous. Yen depreciation creates a greater financial burden on households and small businesses, weighing on economic and consumer recovery potential.

Bank of Japan’s Governor Kazuo Ueda took office this April and could bring change to Japan’s monetary policy. Ueda committed to continuing (for now) the yield curve control policy implemented by his predecessor. The accommodative monetary policy isn’t likely to change until next year.

Meanwhile, in the U.S., the Fed hinted recently that rate hikes could extend for longer. This sets up for the yen and dollar divergence to grow once more. Bank of American analysts forecast that recovering oil prices and international tourism won’t correct for yen undervaluation.

In short, a weak yen is good for some of the Japanese economy while it greatly hurts other parts. It’s a convoluted, complex morass, heightening investment uncertainty in the near term. Global economic slowing and recession in the second half will weigh heavily on outsourcing companies. The outsized profits for companies that have outsourced internationally will likely be impacted by reduced demand. The benefits of a weak yen will contract while the economic challenges it poses domestically are likely to grow.

Playing the Inflation Game for Economic Benefit

Peters-Golden: Currency-hedging offers one advantage, but let’s now add in the case for Japan’s economy itself. If you and our readers allow, Karrie, let me offer a tasty metaphor: the Japanese economy right now is a bit like a Japanese soufflé pancake.

If properly inflated, it provides rich, delectable rewards; if not, all the air gets out, it deflates, and we’re left with a sad pancake.

So long as the Bank of Japan (BoJ) and the Japanese government get the recipe right and whisk in just the right amount of inflation, investors can look to Japanese equities for some delicious investments.

Let’s talk about the first part of this metaphor here, inflation. Without it, we won’t have a great investment opportunity or a tasty cake. It fits the metaphor here because, in Japan’s case, a little inflation is actually a “good” thing.

Since the 90s, when the asset price bubble collapsed, Japan has faced economic stagnation and price deflation. Since then, the BoJ has pursued a campaign of “rock-bottom” interest rates intended to drive inflation in workers’ wages and boost growth. For the most part, that’s failed to boost inflation – until now.

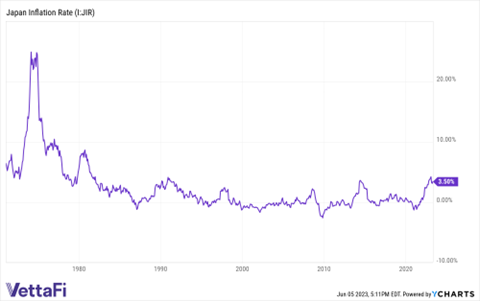

Japan’s historic inflation rate dating back to 1970. The current rate is 3.50%. Source: YCharts.com

Several factors have seen Japanese inflation rise to as much as 4.3% earlier this year, but determining whether inflation stems mainly from “cost-push” inflation or demand inflation is the key question that will determine whether the BoJ will take have to deflate the cake.

On the one hand, there are those who argue that post-pandemic COVID commodities demand and the war on Ukraine are not the main culprits here. Instead, those voices argue, demand-driven inflation has already become the prominent force in raising prices. It creates a scenario that might require rate hikes. For others, “cost-push” inflation remains the villain, a transient issue already ebbing.

BoJ governor Kazuo Ueda, for his part, has warned against rushing into tightening. Ueda recognizes the risks posed by raising rates – letting the cake deflate. Right now, Ueda and the BoJ are hesitating to raise rates unless it becomes clear that demand, not transient commodities costs, is the main culprit for inflation.

That makes sense, too, because a rate hike could absolutely destroy the Japanese economy. For example, the share of variable-rate mortgages rose from 39% to 74% between 2014 and 2022, according to the Japan Housing Finance Agency. Those homeowners are relying on those low, low rates to stay that way. A shift would obviously wreak havoc. Japan’s debt situation, too, would worsen significantly with rate hikes.

That’s why I’m not very worried about a serious shift in monetary policy. Can demand-driven inflation really take Japanese inflation higher overall than commodity and Ukraine-related costs have already? What amount of inflation merits crushing millions of homeowners? Investors who, like me, see Japanese inflation peaking are intrigued by the benefits of an end to decades of deflation and the return of meaningful growth.

Whether in wages or reinvigorated corporations, I think Japan is sitting right in the “Goldilocks” zone of just enough “good” inflation, with Ueda and the BoJ steadily whipping air into some delicious soufflé pancakes.

The BoJ is steadily whipping air into the Japanese economy, like souffle pancakes.

The Issue of Sticky Inflationary Pressures

Gordon: If the economy is like a Japanese soufflé pancake, what happens when too much air gets mixed in? That’s basically what seems to be happening right now with BoJ Governor Ueda and the inflation data.

Speaking last month, Ueda acknowledged that the BoJ inflation forecast could be wrong. It’s a big deal after so much certainty and commitment to an accommodative monetary policy under his predecessor.

Ueda also hinted at the growing stickiness of inflationary pressures and “activity that could lead to sustained inflation.” The bank then eliminated forward guidance regarding interest rates in another historic move. It also reduced GDP forecasts for the year due to lower private consumption and forecasted higher CPI due to rising wages.

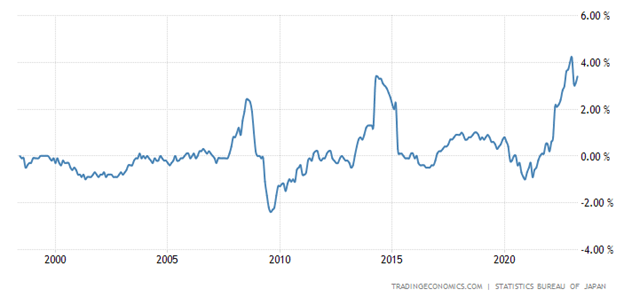

Japan’s core CPI rate over the previous 25 years

Image source: Trading Economics

But let’s talk about what’s actually happening right now. Headline inflation declined in recent months in Japan on falling energy prices, but that doesn’t signal inflation is over. Core consumer inflation (minus most energy and fresh food) gained in April to 3.4%. This is after falling and holding at 3.1% year-over-year in February and March. It’s currently at multi-decade level highs and looks to continue rising.

What’s more, individual inflation measurements continue to rise — 80% of items measured for CPI have been on the rise in the last three months. Inflation expectations hit all-time record highs this year as well. 65.8% of households anticipate at least 5% price gains in the next year as of February. Businesses also forecast 2.3% inflation in the next three years, the highest forecast on record.

Annual wage negotiations (shunto) look to set wage gains at 3.7% for the next year. Actual wage gains generally fall short of the negotiated level, but a 3% rise in wages isn’t unreasonable. Altogether, the big picture looks pretty incompatible with the 2% inflation the BoJ wants.

Governor Ueda has good intentions, but despite caution, too much sticky inflationary pressure is added into the mix. Like too much air in a soufflé pancake, it’s all likely to collapse once the BoJ is forced to raise rates in response to sticky, rising inflation.

But what happens if the BoJ makes sad pancakes instead?

Investors looking to capture recovery potential in the region but want to address targeted Japan exposure separately have options. The iShares All Country Asia Ex-Japan ETF (AAXJ) is one fund to consider that offers exposure to countries like China, Taiwan, India, and South Korea and is up 3.95% YTD. The Franklin FTSE Asia ex-Japan ETF (FLAX) is another fund to consider and is up 3.01% YTD.

Capitalizing on Broad Economic Recovery

Peters-Golden: Now, if the BoJ and Japanese government manage to bake a lovely cake, what can investors expect from it? We can already see some attributes of a positive inflationary environment in wages, on top of strong tourism and robust dividends. Let’s take a look.

First, let’s recognize that more than half of Japan’s GDP stems from consumer spending. Specifically, private consumption accounted for 55.2% of nominal GDP this past December. The U.S. relies even more on private consumption at 68.5% by similar analysis, but it’s clear that both lean on consumer spending as a key pillar of overall economic health.

With that in mind, market watchers should cheer the latest wage news. This spring’s annual “Shunto” wage negotiation period has yielded some of the biggest wage hikes in a quarter century. Big auto companies, including Honda, are talking up wage hikes – in Honda (STOCK) ‘s case, as much as 5%. That doesn’t mean that the tight labor market and inflation have already solved a prolonged lack of wage growth. I’d say wages are moving in the right direction, however.

Interestingly, a nonzero amount of this wage hike campaign owes to Prime Minister Fumio Kishida’s “New Capitalism” policy. While perhaps lacking concrete government actions, Kishida’s call for firms to raise wages appears to be working on its own to some extent. The late former Prime Minister Shinzo Abe’s corporate governance reform push also seems to be helping, with firms learning to love buybacks again. That helps given how many big-name Japanese firms are sitting on tons of cash.

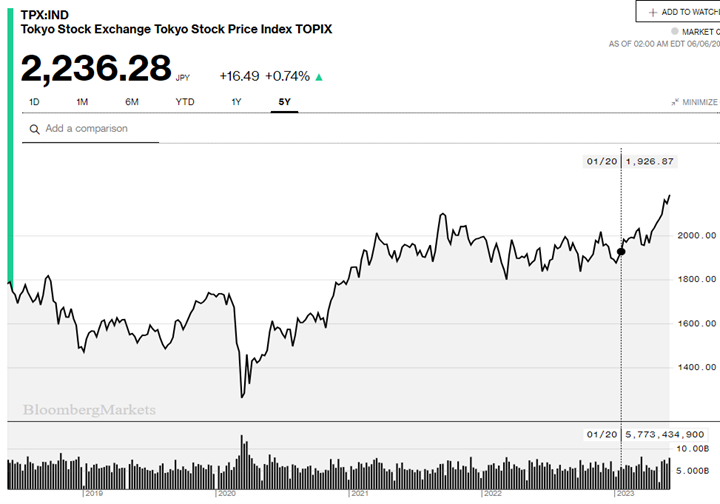

There are some obvious green shoots here that, barring rate hikes, can appeal to investors. Add a booming tourism industry that owes at least some credit to foreign currency strength and robust dividends, and a nice picture starts to develop. Specifically, this picture of the Tokyo Stock Price Index (TOPIX) hitting a five-year high:

The TOPIX has hit a five year high.

Image source: Bloomberg

Too Much Uncertainty Impacts Foreign Investment

Gordon: Japan certainly has attractive investment qualities right now for foreign investors and garners a fair amount of media attention, but actual investment continues to pull back. The Japanese Ministry of Finance reported foreign direct investment in Japanese equities of 867.5 billion yen (USD 6.2 billion) between May 14-20. This is compared to 2.4 trillion yen in the first full week of April, a striking falloff.

What’s more, the BoJ’s admitted uncertainty regarding the path of inflation and potential monetary policy changes alongside the global macro environment means that the biggest players are sitting out for now. As an island nation, Japan relies heavily on imports and exports to sustain its economy.

Slowing global demand in the second half will likely weigh heavily on Japan’s economy. The BoJ acknowledged that there would probably be downward pressure on recovery due to previously high commodity prices and global economic slowing this year.

All of this means asset managers like BlackRock are currently underweight in Japan. BlackRock states forecast monetary policy changes and the impact of global developed market economic weakness for their current positioning. Where the giants fear to tread seems a strong indicator that investors should beware.

Beyond just the short-term risk, however, Japan’s long-term prognosis is grim. The population has been both aging and declining since 2009. A quarter of the population is currently 65 and older, and the Japanese National Institute of Population and Social Security Research forecasts that it will increase to a third by 2033.

Meanwhile, birth rates hit record lows in 2022, falling for the seventh year in a row. It’s a brewing crisis, and thus far, government attempts to reverse the trend remain unsuccessful.

That said, there are options for investors that want to capture short-term opportunity while hedging for risk potential. The KraneShares S&P Pan Asia Dividend Aristocrats Index ETF (KDIV) is a fund to consider that diversifies across several countries. KDIV offers better dividend yields than U.S. dividend aristocrats YTD and is up 6.08% for the year.

Peters-Golden: You make some compelling points, Karrie, but I’m sticking with my support for Japan as a market. As one of the world’s largest, most complex economies, it has plenty to offer investors. ETFs like DXJ and the WisdomTree Japan Hedged SmallCap Equity Fund (DXJS) can now provide compelling alpha to portfolios.

Gordon: Nick, the idea of your Japanese soufflé pancakes sounds absolutely delicious. However, the reality seems full of too much air and ripe for collapse for my liking. If there is any opportunity in Japan, it could be said to be in this bubble happening right now. However, markets and history have taught us the cost of bubbles and getting caught on the wrong side of a trade when it pops.

Thanks so much for chatting Japan with me; it’s been great, as always.

For more news, information, and strategy, visit the Modern Alpha Channel.