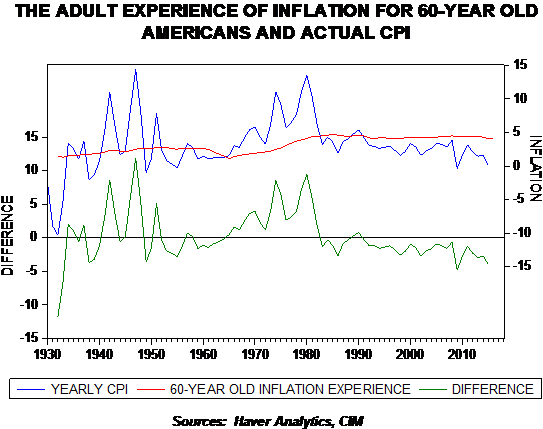

However, after peaking in 1981, bond yields began a steady drop into the current year despite the relatively high level of inflation experience. On the other hand, T-note yields exceeded the inflation experience of 60-year-olds in absolute terms until 2002.

{kind=link}

This chart shows the actual inflation rate compared to an average 60-year-old’s adult experience of inflation. In general, bull markets in bonds tend to occur when the actual inflation rate is persistently below the average rate. Bear markets happen when the opposite condition is in place.

Currently, the actual inflation rate is still well below the average rate, suggesting that the bull market in bonds should have more time to run. However, our worry is that the average 60-year-old is unusually sensitive to inflation fears and thus may overreact to the incoming president’s policies.

In other words, inflation expectations may become unanchored rather quickly, forcing the Federal Reserve to turn unexpectedly hawkish. Thus, we are taking a more cautious stance on fixed income into 2017, expecting higher yields and greater duration risk.

At the same time, we will be closely monitoring the economy in light of less accommodative monetary policy. Most recessions occur because the Fed tightens too much. We don’t expect that to become a problem until late next year or early 2018 if the Fed continues to raise rates. So, for the upcoming year, we expect a weak fixed income environment.

This article was written by the Asset Allocation Committee at Confluence Investment Management, a participant in the ETF Strategist Channel.

Disclosure Information

Past performance is no guarantee of future results. Information provided in this report is for educational and illustrative purposes only and should not be construed as individualized investment advice or a recommendation. The investment or strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Opinions expressed are current as of the date shown and are subject to change.

This report was prepared by Confluence Investment Management LLC and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change. This is not a solicitation or an offer to buy or sell any security.

[1] For example, the two-year deferred Eurodollar futures, which measure three-month LIBOR two years into the future, have jumped nearly 50 bps since the election.

[2] http://fortune.com/2015/12/13/oldest-ceos-fortune-500/