The Weekly Chart: Emerging Markets & Commodities Linked

{kind=link}

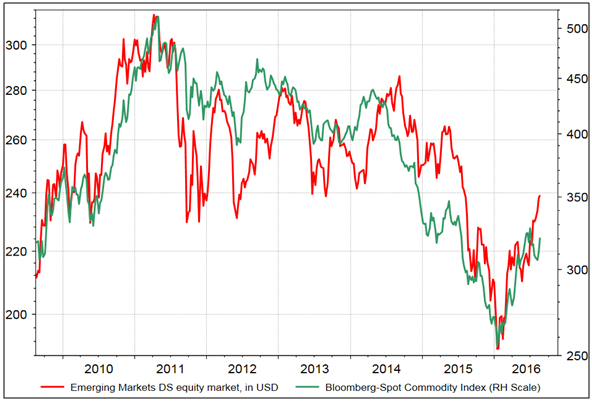

Source: Thomson Reuters Datastream, Riverfront Investment Group. Data as of 8/19/16. Past performance is no guarantee of future results. It is not possible to invest directly in an index. The Bloomberg-Spot Commodity Index measures the price movements of commodities included in the Bloomberg Commodity Index and select subindexes. It does not account for the effects of rolling futures contracts or the costs associated with holding physical commodities and is quoted in USD. It is not possible to invest directly in an index.

EPILOGUE: EMERGING MARKETS STORY MORE THAN JUST THE 3 C’s.

Clearly, our 3 C’s explanation is a simplification of sorts (strategists have never met a catchy acronym that they don’t like). Other positive near-term drivers of the EM story include the fact that EM economies are not likely to be as affected as developed markets by Brexit issues and controversies surrounding European and American politics. In addition, in EM regions such as Latin America and India, there is growing potential for positive structural reforms, though lasting reform has often proven elusive in developing countries. Eventually, we believe that for the cyclical (near-term) bull market in EM stocks to develop into a secular (long-term) one, we need to see the positive macro drivers discussed above start to improve earnings, margins and return on equity at the corporate level, where EM has generally struggled since 2011. Some encouraging early signs of this include recent improvements of relative macro growth and earnings-per-share expectations of EM vs. DM, trends we will continue to watch closely going forward.

Chris Konstantinos is the Director of International Portfolio Management at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities. In a rising interest rate environment, the value of fixed-income securities generally declines.

Using a currency hedge or a currency hedged product does not insulate the portfolio against losses.

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Buying commodities allows for a source of diversification for those sophisticated persons who wish to add this asset class to their portfolios and who are prepared to assume the risks inherent in the commodities market. Any commodity purchase represents a transaction in a non-income-producing asset and is highly speculative. Therefore, commodities should not represent a significant portion of an individual’s portfolio.

Diversification does not ensure a profit or protect against a loss.

RiverFront’s Price Matters® discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation.

RiverFront Investment Group, LLC, is an investment advisor registered with the Securities Exchange Commission under the Investment Advisors Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

Index Definitions

The Markit PMI (Purchasing Managers’ Index) series provides advance insight into the private sector economy by tracking variables such as output, new orders, employment, and prices across key sectors.

It is not possible to invest directly in an index.