By Chris Konstantinos, RiverFront Investment Group Director of International Portfolio Management

Following five years of emerging market (EM) equities being the worst performing major asset class, the MSCI Emerging Markets Index has truly “emerged” in 2016 (pun intended), up 16.6% YTD through last Friday.

We have been generally cautious on EM for the last few years, but since March of this year we have been building our weightings up, especially in our longer timeframe portfolios. We are now overweight relative to our composite benchmarks, though our shorter timeframe portfolios still have only a small absolute weighting for now.

While we have long believed that EM was “cheap” and possessed potential for positive mean reversion, we viewed fundamentals as poor and lacking catalysts for that mean reversion. Our improved outlook on EM is related to recent changes in three major macro pillars – the “3 C’s”: China, Central bank policy in the developed world, and Commodities.

CHINA: MACRO DATA STABILISING, CURRENCY POLICY LESS CONCERNING

Almost every emerging market economy is influenced by China. Latin American and African regions sell commodities to China (the world’s largest commodity importer), and emerging Asian countries both compete with China for manufacturing and depend on them for aggregate demand. Therefore, we think it’s fair to say that as China’s economy goes, so goes EM.

So where does China’s much-maligned economy find itself today? We describe it as stabilizing, albeit at a much lower growth level than in times past.

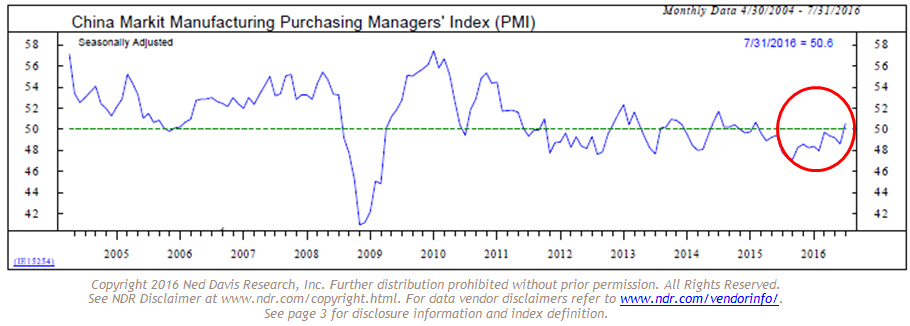

Important indicators of the “smokestack” part of China’s economy, such as electricity usage and railway freight, have all shown signs of improvement recently, as has the Markit Manufacturing PMI (a survey of manufacturers), which is now just back in expansion for the first time in roughly a year (see chart below). “New China” indicators, related to services sectors and the burgeoning middle class consumer, have remained solidly in expansionary territory, with areas like consumer confidence rebounding and home prices in Tier One cities making new highs.

Click to enlarge:

{kind=link}

A surprise? Not if you look at financial conditions in China, which are finally easing after a general period of tightening from 2011 to mid-2015. Taking a page out of the developed nation playbook, China is now using accommodative policy (lower interest rates, a cheaper currency, and targeted government spending) to help stimulate aggregate demand, and it appears to be having some positive impact.

Last but not least, another major difference in China today versus 2015 is that policymakers now appear keen to avoid further sharp volatility in the yuan exchange rate to the US dollar. While the yuan continues to depreciate, it has done so in a much more gradual fashion than last autumn; this lessened slope of decline has likely acted as a calming factor for markets.

CENTRAL BANK POLICY

Dovish Fed (and BoE, ECB and BoJ) is bullish for EM currencies and equities. As developed world interest rates sink due to aggressive central bank measures, global demand for higher rates of return (the “quest for yield”) will likely drive investor behavior, in our view.

We think this quest is likely to continue to drive capital from developed market (DM) rates and currencies into EM ones, where rates tend to be higher even after adjusting for relative rates of inflation. This capital inflow tends to provide support for emerging market currencies, which in turn improves the creditworthiness of many sovereign and corporate borrowers in the emerging world (who often have liabilities denominated in currencies like the dollar and euro). This lowering of default risk also can drive the risk premium down for EM stocks, causing higher valuation multiples.

SEE MORE: In Uncertain Times, Cash is King in Investing

Due to this relationship, EM equity prices have often exhibited positive correlation to their currencies, which suggests that US investors can benefit from a virtuous circle of appreciating currency exposure and higher stock prices in EM as this demand for yield plays out.

It helps that EM currencies, which entered 2013’s Taper Tantrum period mostly overvalued relative to long-term purchasing power, are now more reasonably valued, and thus have the potential for further strength if the Fed and other major central banks remain accommodative, in our opinion. EM equities still trade below their long-term averages on a price-to-book basis, a condition that suggests multiples could also continue to re-rate higher.

COMMODITIES

“Goldilocks” environment for commodity prices a positive for EM equities. We believe that commodity prices likely bottomed in 2016. As stated in Riverfront’s most recent Strategic View published on August 2, we believe that commodity prices are now in a “Goldilocks” environment for equities, with prices neither low enough to create default concerns for energy companies nor so high that they choke off global economic growth. We believe this a positive for EM equity prices, which are historically correlated to both commodity prices (see The Weekly Chart below) and to global growth trends.