Note: This article appears on the ETFtrends.com Strategist Channel

By Chris Konstantinos

The unexpected result of the Brexit vote in the UK on June 23 unleashed a litany of uncertainties into the global economy. While Friday’s US payroll number (+287k headline) was strong enough to push US markets within sight of all-time highs, we believe the sheer number of things about Brexit we won’t know for months will likely weigh on sentiment. In times like this, we find the following approach helpful to formulating an investment strategy:

- Take a deep breath (apparently, more oxygen is good for you).

- Amidst uncertainty, focus on the handful of things about which you are relatively certain.

The most “certain” thing in our mind right now is that global interest rates will likely stay lower for longer than most of us thought prudent (or even possible) 6-12 months ago. To us, one of the most important implications of a protracted period of low interest rates is that the need for yield is likely to drive demand for high-quality, dividend-paying equities. The reason is fairly straightforward – when interest rates are below the cost of living, investors with any time horizon longer than the near term will likely be forced eventually to trade up into assets that can provide not only positive real cash flow, but also growth of that cash flow. In uncertain times, cash (in the hand) is king.

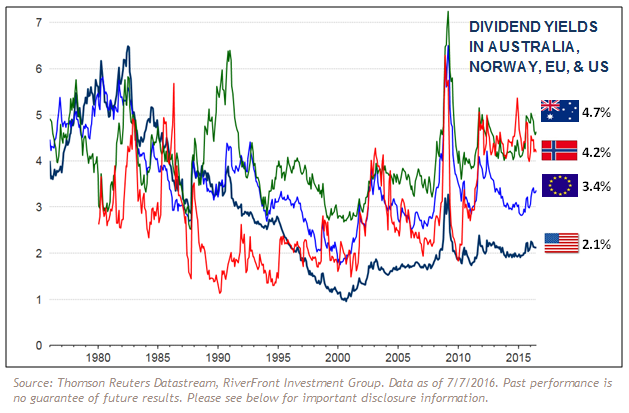

While we continue to take advantage of quality dividend payers in the domestic side of our portfolios, we increasingly believe the really compelling dividend story is now overseas. Many US investors may not be aware that higher dividend yields are available outside of the US (see chart below). To this end, we have focused our international investing on high-quality global franchises that have a history of paying dividends and, more recently, in regions whose dividend yields are well in excess of global interest rates, such as Australia, Norway, and broad emerging markets.

{kind=link}

DIVIDENDS > BOND YIELDS: A FAMILIAR TUNE, NOW PLAYING IN EUROPE

This strategy should sound familiar; high quality dividend stocks in the US enjoyed quite the bull market from 2009-11, when the Fed first took rates low, and these stocks have continued to reach new absolute highs since. At the outset of that bull market in 2009, the differential gap between the US stock dividend yield and 10-year Treasury yield had gone positive (meaning the dividend yield was actually higher than the bond yield) for the first time in many decades. Interestingly, the differential between bond yields and stock dividend yields in European stocks is now similarly at all-time positive spreads (see Chart of the Week, below).

Related: Japan’s 2016 Monetary Policy: Mistakes and Missed Opportunities