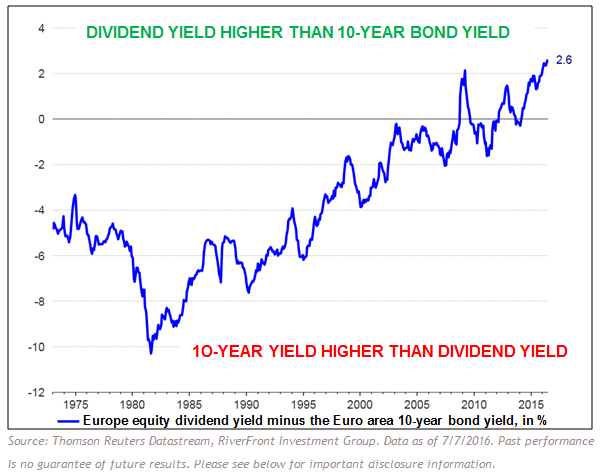

In fact, there is right now a whopping +2.6% advantage for the European equity dividend yield relative to the Eurozone 10-year government bond yield. If we instead used a larger European country’s 10-year government bond yield, such as Germany’s, the gap would be even more positive. The US gap is now positive again as well, though the absolute level is not quite as compelling at +0.70%. This attractive spread now extends to corporate bonds as well; corporate bond yields of many high-quality European exporters are now also lower than their respective dividend yields. The meta-message is clear to us: in this environment, it is best to continue to own quality dividend payers in all geographies; and, if you don’t have any international dividend exposure at all, now might be a historically advantageous time to start fishing.

CHART OF THE WEEK: GAP BETWEEN EURO INTEREST RATES AND DIVIDEND YIELDS AT ALL-TIME WIDES

{kind=link}

CAUTION: NOT ALL GLOBAL DIVIDENDS ARE CREATED EQUAL

Importantly, RiverFront views the ability to pay and grow dividends on an ongoing basis as a much more attractive long-term trait than simply offering investors a high dividend yield now. To be sure, there is no “free lunch” – across countries, regions, and industries, there is a clear correlation between level of yield and level of risk, often in the form of more cyclical characteristics, higher dividend payout ratios and greater leverage. In the current kind of environment, where tail risk is alive and well, we believe it is best to avoid reaching for yield and searching for outsized dividends in areas with disadvantaged fundamentals such as European banks, certain energy-related industries and some highly indebted emerging market countries.

Chris Konstantinos is the Director of International Portfolio Management at RiverFront Investment Group, a participant in the ETF Strategist Channel.

[related_stories]Important Disclosure Information

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Dividends are not guaranteed and are subject to change or elimination. Strategies seeking higher returns generally have a greater allocation to equities. These strategies also carry higher risks and are subject to a greater degree of market volatility. Diversification does not ensure a profit or protect against a loss. High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities. In a rising interest rate environment, the value of fixed-income securities generally declines. Using a currency hedge or a currency hedged product does not insulate the portfolio against losses. RiverFront Investment Group, LLC, is an investment advisor registered with the Securities Exchange Commission under the Investment Advisors Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.