By Rod Smyth, RiverFront Investment Group Chief Investment Strategist

This is not a timing piece, this is a gut check. We think it makes little sense that the world’s most indebted major economy, the one with arguably the worst growth prospects due to its rapidly aging population, should have borrowers lining up to give it money and pay for the privilege of owning the debt. We are referring to Japan to make a point, but some of the same reasoning applies anywhere that long-term government bond yields are negative, such as Germany and Switzerland.

A buyer of long maturity bonds with negative interest rates could simply want to own the currency, or they may have a pessimistic outlook for long-term economic growth/ inflation. At RiverFront, we regard bonds with negative yields as unattractive Think about it: a portfolio of negative yielding bonds could be regarded as a liability, not an asset.

Negative rates in practice

Governments issuing debt at negative interest rates are not expecting their bond holders to mail in monthly checks; rather, the buyers pay a premium for a bond that pays no interest, recognizing that the bond will mature at a price below what the buyer paid. That way, the loss (or negative interest rate) is built in.

If you borrow from the Japanese government in yen, then there should be no risk that they fail to pay you back in yen (as they control the printing press) so let’s assume no risk of default. The risks instead are absolute and relative. In absolute terms, the prices of these bonds will likely fall if either economic growth or inflation accelerates. In relative terms, the risk is that there is the opportunity to make a positive return in something else, rather than locking in a negative return.

Why buy?

The reason an independent, impartial investor has historically demanded to be paid interest is to compensate them for inflation or a loss of purchasing power while owning the bond. Thus, an investor buying a government bond at a negative yield is likely doing so in the belief that inflation will fall by more than the decline in the value of the bond. In other words, the buyer expects a positive return relative to inflation or positive real interest rates.

This is perhaps easier to understand in a world of rising inflation and positive interest rates, but the principal is the same. Until recently, Japan had much lower interest rates than other countries, but it also had falling prices (deflation), so the spread between its interest rate and inflation – its real interest rate – was comparable (see Chart below). At current interest rates, who is buying negative interest rate bonds? We suggest the following:

- The Central Bank: The Bank of Japan is still actively increasing its holdings, ironically with the goal of creating the inflation that will make the purchasing of bonds a bad investment.

- Natural owners of yen (i.e. domestic savers and financial institutions): A yen-based saver who wants or is required to keep a portion in yen, and who wants a government guarantee, has to accept prevailing negative rates. (The option for the same investor to buy US dollar debt with a positive interest rate and hedge out the currency risk is part of why we think US rates can continue to fall. In a relative world, we believe it is a compelling trade.)

- Speculators: Those who believe Japanese rates will go more negative before they turn, and those who simply trade on momentum. Also those expecting further yen appreciation, since currency moves often dwarf interest rate levels.

- Investors: Those who believe the vice grip of deflation has its lock on Japan and that the central bank doesn’t have the fortitude to resort to more bold money printing to turn the tide.

We choose not to be among the buyers of negative interest rate debt. We believe deflation, if not reversed, will continue to damage Japan’s economy, and thus Japan’s ability to pay back its debt, making further drastic monetary policy likely. As mentioned, Japan is not the only country with negative interest rates. Switzerland was the first country to take interest rates negative, in part to try and penalize speculators who were bidding up the value of the Swiss franc.

SEE MORE: In Uncertain Times, Cash is King in Investing

Like gold, the Swiss currency is seen as a safe-haven and investor’s desire to own it, despite negative rates, is easier to understand. Germany is arguably the strongest, best managed economy in the Euro block, and as a result has the lowest 10-year bond yield. Relative to the other Eurozone countries this seems rational, but as with Japan, we have no desire to own German bonds, especially when US bond yields are positive. US yields are currently positive, which we think merely makes them relatively attractive in a world of unattractive choices.

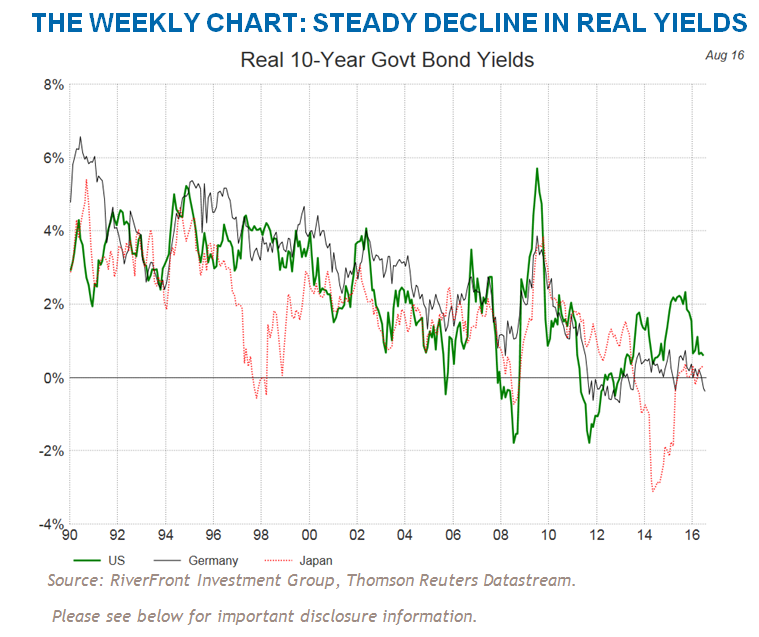

Click to enlarge chart:

{kind=link}

Our chart above shows real 10-year government bond yields (adjusted for local headline inflation rates) for the US, Germany, and Japan. Japan’s low nominal yields were offset by deflation and low inflation during most of this timeframe, making real interest rates comparable. We suggest focusing on the trends, as headline inflation is volatile.

In the 1990’s, US and German real interest rates averaged 4%, and Japan’s were slightly lower. The memory of high inflation during the previous 15 years caused investors to be vigilant about its potential return. How investors would love those yields now! Since 2000, real interest rates have gradually declined towards zero as central banks have become sustained buyers and investors appear to have no concerns about future inflation. We think this makes for poor risk/reward to anyone buying at current yield levels.

Rod Smyth is the Chief Investment Strategist at RiverFront Investment Group, a participant in the ETF Strategist Channel.

[related_stories]Important Disclosure Information