By Giralda Advisors

This is the capstone of our series on Risk-Managed Investing (RMI). In our initial piece, The Time Has Come for RMI, we described the RMI approach to equities as embedding volatility dampening and/or downside risk mitigation directly within the equity investment itself. In two other early installments, RMI and Investing in a Rising Rate Environment and RMI and the Liquid Alternatives Landscape, we outlined how RMI could be part of a solution to “the Portfolio Problem” caused by the disappointing prospects for non-equity asset classes. With the background provided by all the subsequent articles (see archive here) — which spanned addressing such financial planning challenges as volatility drag and sequence risk; adding long-term alpha over complete market cycles; calibrating how low the cost of risk management needs to be in order to be worthwhile; exploring a range of RMI solutions in the marketplace; optimizing portfolios once RMI solutions are introduced into the picture; and examining the implications for portfolio performance measurement and benchmarking — we would like to return now to the Portfolio Problem and explore the profound impact that RMI can have in attempting to solve it.

The Portfolio Problem Revisited

We framed the Portfolio Problem as follows: Equities are essential for most client portfolios but are subject to severe downside risk, and (this is the crux of the problem) what’s worked to buffer that risk over the last 30 years — diversifying into non-equity asset classes — is extremely unlikely to work well over the next decade or more.[1] This is a phenomenon unique in the careers of most financial advisors.

A backdrop to this Portfolio Problem is another issue, and one of long standing. Diversification itself is unreliable. It always has been. Diversification benefits are not guaranteed. The low (or even negative) correlation among various “diversifying” asset classes is merely a tendency, not a law of nature. And it’s a tendency that tends to disappear when the investor needs it most to prevail, i.e., when markets enter a period of extreme stress. Now, diversification — in its most effective form, which includes scientific asset allocation and rigorous rebalancing — remains a prudent portfolio construction approach in our view, but it should be recognized that it was never designed to manage severe market risk and contagion. In other words, simply assuming that asset classes that diversify each other in calm markets will continue to do so when you most need them to do so has never been a sound assumption, and is one made at the investor’s significant peril.

And now, against this backdrop, the asset classes that advisors have spent their careers relying upon appear to be poised for historic levels of disappointing performance. The Portfolio Problem is a significant one indeed, and it should be clear that counting on solutions that may have worked in the past is an imprudent strategy for a professional financial advisor.

A Different Solution Is Needed

We need a new solution. It should come as no surprise to followers of our series thus far that Risk-Managed Investing (RMI) — the attempt to embed downside risk management directly into the equity investment itself — is by far the most promising approach to the Portfolio Problem that we have examined. (Practical RMI solutions available in the marketplace are reviewed in RMI Applications: Sector Rotation Using ETFs, RMI Applications: Tail Risk Hedging, and Marketplace Review of Risk-Managed Investments.)

What makes RMI an elegant solution to the Portfolio Problem?

- RMI satisfies the portfolio’s essential need for equities

- RMI addresses portfolio risk directly at its source

- RMI diminishes the reliance on “diversifying” asset classes to provide risk management

- RMI does not disrupt the tenets of asset allocation; in fact, it explicitly addresses its weakest assumption, namely, that asset classes that diversify each other in normal markets will continue to do so during periods of market stress

- RMI can raise the “efficient frontier” — as demonstrated in Risk-Managed Investing and Portfolio Optimization

As a result, RMI can allow “re-risking” of the portfolio, as we’ll now explain.

Re-Risking the Portfolio: 80/20 as the New 60/40

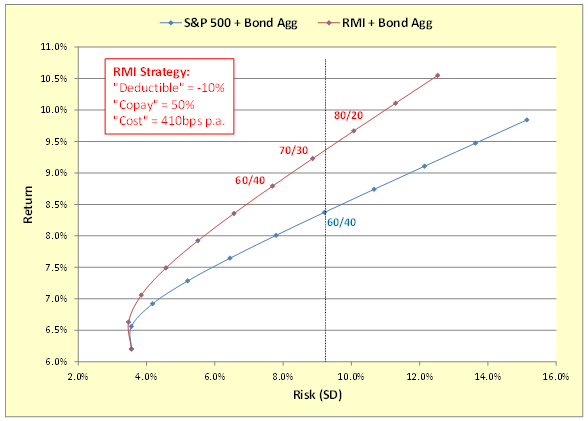

Let’s take another look at the efficient frontier graph we presented in Risk-Managed Investing and Portfolio Optimization.

{kind=link}

Recall that on this chart we plotted, in blue, the efficient frontier of a two-asset stock/bond portfolio, using the S&P 500 Total Return Index and the BarCap Aggregate Bond Total Return Index to represent the two assets. Twenty years of daily return data (December 30, 1994 through December 31, 2014) was used, and rebalancing was ignored for simplicity. On the same chart we plotted, in red, the efficient frontier obtained by substituting for the S&P 500 an RMI investment. This particular RMI investment has a “deductible” of -10%, a “copay” of 50%, and a “cost” of 410 basis points per year — that is, the downside protection kicks in when the S&P 500 Index suffers a drawdown of -10% or worse, the protection mitigates 50% of any subsequent decline net of the cost of the protection, and the performance drag relative to the S&P 500 during periods when the protection is not needed is 410 basis points per annum.

Comparing the two 60/40 portfolios, it is evident that the RMI-infused portfolio has a higher return and lower risk than, and therefore clearly dominates, the traditional 60/40 portfolio over this period. This is due to the superior risk management afforded by RMI as encapsulated in the bullet points of the prior section. In fact, the graph shows that an RMI-based portfolio of roughly 73/27 delivers a much higher return, at the same level of risk, than the traditional 60/40 portfolio in this particular example.

Note that the RMI strategy displayed here is not a very robust one — its assumed cost is right at the breakeven level — and there are RMI investments outlined in our prior pieces that we judge to be materially more cost-efficient. Also, this efficient frontier is based on prior return history of the BarCap Aggregate Bond Index — a history that, as we discussed, likely overstates, significantly, the expected future performance of fixed income investments. Finally, the two-asset portfolio in this analysis is admittedly a very simple one — adding the next-most popular asset class, alternatives, to the mix would likely make the case stronger still, given the problems with alternatives noted above. For all these reasons, we expect that a cost-effective RMI strategy would elevate the frontier higher still, allowing investors to move to an 80/20 (or even more aggressive) portfolio and enjoy a substantially better potential return, with the same or less risk, than a traditional 60/40 portfolio[2].

This finding is significant. It represents, we believe, a paradigm-shifting way to consider portfolio construction in today’s environment and the years ahead.

To recap: Replacing a sizeable portion of traditional equities within the portfolio with cost-effective RMI counterparts can reduce the portfolio’s need to rely on non-equity asset classes to manage downside risk. The investor can therefore lower the allocation to non-equity assets and correspondingly raise the allocation to (risk-managed) equities. Based on our findings, an 80/20 portfolio could actually be safer in down markets and better performing in up markets than a traditional 60/40 portfolio is likely to be, particularly given the challenges ahead for non-equity asset classes.

This is why we believe that 80/20 could be the new 60/40.

This article was written by Jerry Miccolis, Gladys Chow and Rohith Eggidi of Giralda Advisors, a participant in the ETF Strategist Channel.

[1] This is particularly true of traditional fixed income investments, for which we believe it is a virtual mathematical impossibility, in the current and prospective interest rate environment, to achieve performance anywhere near that of the 30-year bond bull run. And attempts to improve return through sacrificing credit quality would serve to increase the risk and decrease the diversification benefit of this asset class, thereby compromising its mandate. Liquid alternatives are also challenged due to an abundance of funds chasing too few good ideas, resulting in a long-term trend of declining returns and increasing correlation with equities.

[2] We use “80/20” and “60/40” in this instance and subsequently as a shorthand reference to asset allocations among two or more asset classes. For example, “60/40” could represent a 60/20/20 allocation to equities/fixed-income/alternatives, respectively. This is consistent with general industry usage.

Disclosure Information

This material is for informational purposes only. Nothing in this material is intended to constitute legal, tax, or investment advice. Investing involves risk including potential loss of principal.

Giralda Advisors, located in New York City, is an asset management firm that focuses on providing risk-managed exposure to the equity markets with a goal of limiting asset depreciation during both protracted and catastrophic market downturns while allowing substantial asset appreciation in up-trending markets. The Giralda Advisors team welcomes your inquiries. Call (212) 235-6801 or visit us at https://www.giraldaadvisors.com/.