In our first article in this ETF Strategist series, we discussed a number of common current concerns among financial planning clients. These concerns can be collectively described as the “portfolio problem,” and more briefly recapped as follows:

- Equities are, arguably, the single most essential component of client portfolios — they represent the growth engine, the asset class most likely to keep clients ahead of inflation and allow their financial plans to succeed — but equities are subject to substantial volatility and significant downside risk

- The other asset classes in the portfolio — a primary purpose of which is to buffer the risk of the equity asset class — have become problematic and detrimental to portfolio performance

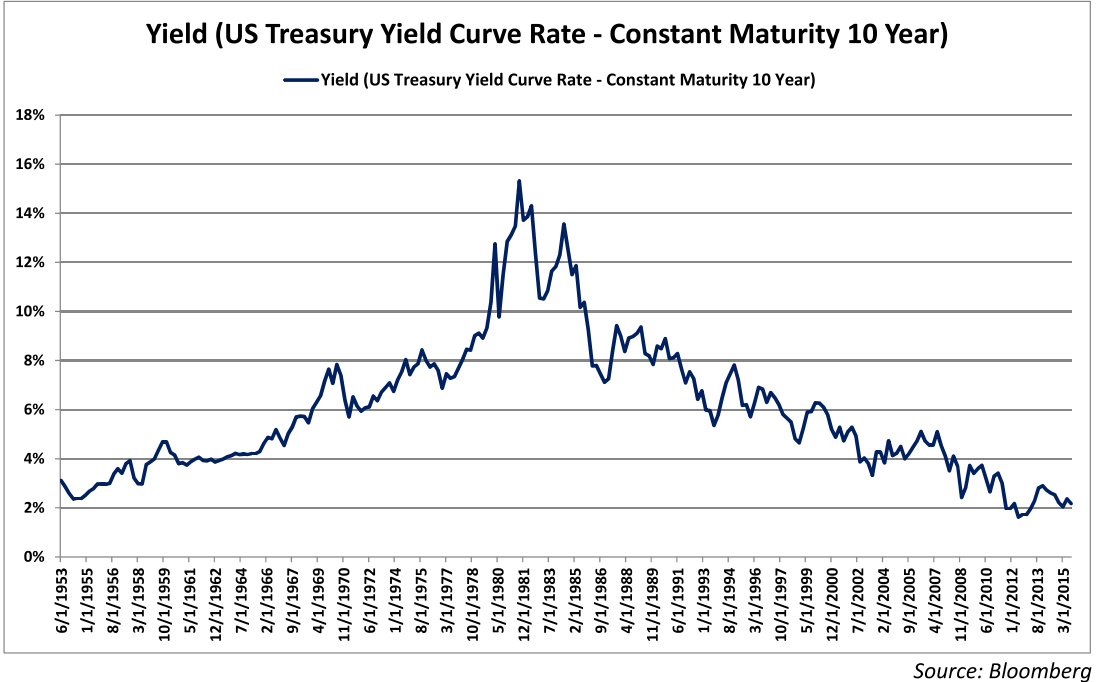

This second phenomenon is especially pronounced in the asset class that has long been the principal source of non‐equity exposure — fixed income investments. Fixed income, by virtue of prevailing interest rates having fallen from their heights in the early 1980s to their historically low levels of the last few years (see graph below), has enjoyed a 30‐year bull market.

{kind=link}

Interest rates cannot fall much further; they almost literally have nowhere to go but up. The Federal Reserve has “officially” ushered in the new chapter of rising interest rates with its long‐awaited hike in the Fed funds rate just before Christmas.

Rising interest rates are not good news for the total return of traditional fixed income investments, as the market value of bonds moves in the opposite direction from rates. In the language of those that track market valuations, bonds currently are historically overpriced. Others phrase this as bonds being on the precipice of a sustained bear market. Whatever terminology you prefer, you cannot escape the conclusion that we are in for a long period of dismal fixed income performance.

The problem is particularly acute for bond mutual funds. Shareholders in these funds tend to redeem their shares when the funds show disappointing results. To honor these redemptions, fund managers need to liquidate some underlying individual bond holdings before maturity, thus locking in their market value losses. This, in turn, puts further downward pressure on fund performance, leading to more redemptions — and a downward spiral for the shareholders that remain.

This phenomenon in fixed income — which is likely to persist for years, perhaps decades — is, again, unique in the last 30 years. This is why the portfolio problem as outlined above is a first in the careers of most financial advisors. And it may be the most critical financial planning issue their clients will ever face.

Efforts to reach for additional yield in fixed income investments introduce their own problems. These efforts, which generally involve sliding down the credit‐quality scale toward (and sometimes reaching) junk bond status, increase the risk of the fixed income component of the portfolio. This compromises the purpose of this asset class, and makes the portfolio riskier than customary. It gets worse. The graph below shows the rolling 60‐month correlation of the US High Yield Bond Index with the S&P 500 Stock Index. This correlation is high, and has been in the neighborhood of 75% since the financial crisis of 2008‐2009.