Note: This article appears on the ETFtrends.com Strategist Channel

By Corey Hoffstein

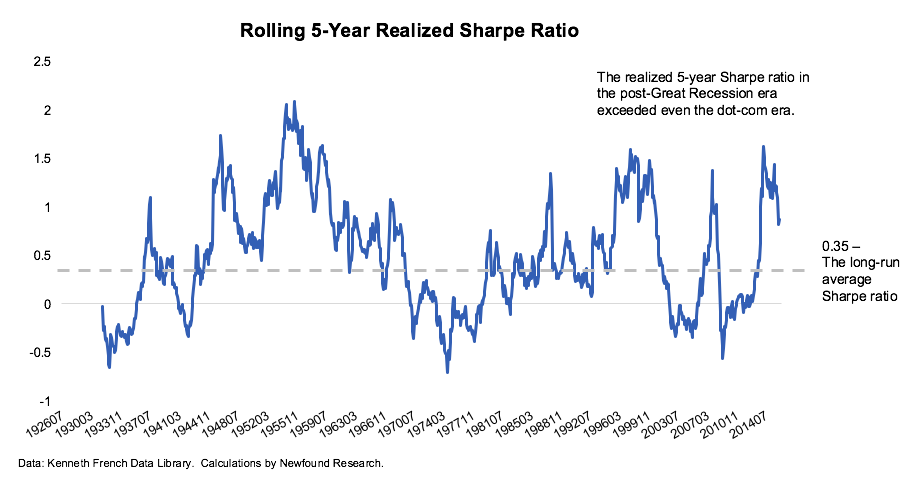

It’s been a good run – nobody can deny that. For being the most hated bull market in history, performance has been stellar on both an absolute and risk-adjusted basis.

How good? Consider this: the 5-year realized Sharpe ratio of the S&P 500 peaked in 2014 at a level higher than what it achieved during dot-com mania.

That’s how good.

{kind=link}

This performance, however, also paints a potentially worrying picture: despite over a year of sideways market action, the 5-year realized Sharpe ratio still sits well above its long-term average. The last two times the risk-adjusted return hit these levels, we saw the dot-com crash and the Great Recession.

Mind the Gap

If we break down this risk-adjusted return into its two components – excess return and volatility – we can get a sense of what is driving the elevated level we are seeing.

The answer, unfortunately, does not bring much comfort.

We can see that the annualized 5-year return is 4.60% above its long-term average and volatility is -4.72% below its average over the same period.

This has not been simply case of just volatility being lower or returns being higher: we’ve been living in a world of higher returns with less risk.

Consider that for returns to stay at this elevated level, volatility would have to climb to over 30% to bring our Sharpe ratio back in line with the historical average.

On the other hand, for volatility to stay suppressed, we would have to see annualized returns fall to 4.5% to fall back in line with the historical Sharpe ratio.

Volatility Happens

Market volatility has historically ebbed and flowed with the grand cycles of panic and mania.

Yet despite all the crises du jour over the last several years (including the European debt crisis, U.S. Budget Sequestration, Greek Bailout/Grexit, Annexation of Crimea by the Russian Federation, China’s slowdown, et cetera), volatility has been surprisingly quiet.

{kind=link}

Some may argue that this data points to U.S. equities being “due” for a correction of spectacular magnitude.

Betting for a crash, however, may not be prudent. To quote John Meynard Keynes, “markets can remain irrational longer than you can remain solvent.”

Markets need not crash for us to revert to our long-term Sharpe. Increasing volatility is only one way to decrease our Sharpe ratio. A prolonged period of depressed returns – like those we’ve seen in the last year – will also get us there just fine.

So whether our outlook is a crash or just lethargic returns: how can we fight the creeping feeling of ennui for staying invested?

We have a few ideas.

First, we believe opportunity often exists at those places outside most investors’ comfort zones. investors should get outside of our comfort zones. Asset classes that have been kicked aside by the market may present more favorable opportunities for return going forward.

Second, we believe investors should consider alternative means to portfolio construction. A traditional strategic portfolio is an obvious choice when equity valuations are low and real yields are high: but we believe there is a significant cost to holding such a portfolio going forward. Embracing strategy diversification may be a prudent play.

Third, investors might consider the role of alternative strategies that have the potential to generate return in both sideways and negative markets.

Finally, investors might consider how they can take advantage of higher yielding asset classes that derive a larger percentage of their total return from yield than from capital appreciation. In doing so, an investor can hopefully dampen portfolio volatility while simultaneously tilting their returns towards a steadier source.

Corey Hoffstein is the Co-founder & CIO at Newfound Research, a participant in the ETF Strategist Channel.