Note: This article appears on the ETFtrends.com Strategist Channel

By Glenn S. Dorsey, CFA

Investors face a two part problem: how to generate income in today’s low-interest rate environment and how to protect their principal if rates start to increase. High yield bonds may be able to solve both challenges. Let’s dissect the problem into its two constituent parts.

First, how can investors generate income in today’s low rate environment? Treasury bonds offer little help in this regard. The 10- year U.S. Treasury note currently offers a pedestrian 1.75% return. A 10-year laddered Treasury portfolio provides a paltry 1.24% return. Conversely, high yield bonds, as represented by the Barclays High Yield index, have a 7% current yield. This 5.25% yield advantage over Treasuries is quite enticing.

Related: Collaboration — the New Model for High-Net-Worth Investors?

The second part of the problem: how does one protect principal if rates start to rise? We all know the irrefutable relationship between bond prices and interest rate — if rates go up, bond prices go down (all else being equal) and vice versa. The magnitude of this price change can be quantified by a bond’s duration. You can think of duration as beta for bonds. For example, a bond with a duration of 5 should decrease by 5% if rates increase by 1%. At the risk of being yet another voice in the choir calling for the eventual rise in rates, rates will eventually go up!! A quick review of the drivers of a bond’s performance exposes two components — income and principal. Going back to our 10-year Treasury with a 1.75% coupon and a duration of just over 9 suggests your return is wiped out with a mere .19% increase in rates (9 x 0.19 = 1.75). High yield bonds on the other hand have a 7.5% yield and a duration of 4.18. This combination offers a positive return with up to a nearly 1.8% increase in rates, a doubling from current levels (4.18 x 1.79% = 7.5).

Related: Central Banks Policies… Everyone Gets a Trophy

Voila, problem solved? Not so fast. High yield bonds are not without their risks. They can often behave a lot like stocks, moving in the same direction and offering little in the way of portfolio diversification. For example, high-yield bonds returned a negative 26.16% in 2008, offering little offset to the 37% decline in the S&P 500 that same year. In fact, since 1984, the high-yield index has declined in value in six years (1990, 1994, 2000, 2002, 2008 and 2015). The S&P 500 declined in 4 of those same years (1990, 2000, 2002, and 2008). Stocks generated small positive returns in 1994 and 2015.

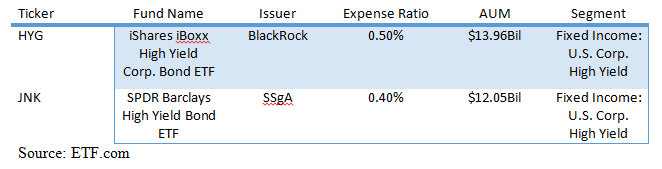

Additionally, buying individual bonds is not for the faint of heart. The markup associated with buying small quantities of bonds makes this route expensive for retail investors. High yield bonds have a fraction of the liquidity provided by stocks or Treasuries. For these reasons, we believe gaining exposure to this asset class is best achieved through the use of ETFs. A list of the largest high yield bond ETFs follows:

{kind=link}

The current environment for high yield bonds is still attractive in our opinion. The current spread on high-yield bonds versus Treasuries is about 556 basis points, slightly more attractive than the 499 basis point average since 1983.

{kind=link}

Despite the carnage in the energy sector, default rates were only about 3.8% at the end of the first quarter, far better than the 12% level experienced in 2009.

{kind=link}

There are no magic potions in the investment arena, but the thoughtful use of high-yield bonds in the right dosage in your portfolio may be just what the doctor ordered.

Glenn S. Dorsey, CFA, is the SVP, Client Portfolio Manager, at Clark Capital Management Group, a participant in the ETF Strategist Channel.

Disclosure Information:

Past performance is not indicative of future results. This is not a recommendation to buy or sell a particular security. The opinions expressed are those of the Clark Capital Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Clark Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no guarantee of the future performance of any Clark Capital investment portfolio. It should not be assumed that any of the investment recommendations or decisions Clark Capital makes in the future will be profitable or equal the performance of the securities discussed herein. Material presented has been derived from sources consider to be reliable, but the accuracy and completeness cannot be guaranteed. The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services can be found in its Form ADV, which is available upon request. CCM-978