Note: This article appears on the ETFtrends.com Strategist Channel

By Glenn S. Dorsey, CFA

Investors face a two part problem: how to generate income in today’s low-interest rate environment and how to protect their principal if rates start to increase. High yield bonds may be able to solve both challenges. Let’s dissect the problem into its two constituent parts.

First, how can investors generate income in today’s low rate environment? Treasury bonds offer little help in this regard. The 10- year U.S. Treasury note currently offers a pedestrian 1.75% return. A 10-year laddered Treasury portfolio provides a paltry 1.24% return. Conversely, high yield bonds, as represented by the Barclays High Yield index, have a 7% current yield. This 5.25% yield advantage over Treasuries is quite enticing.

Related: Collaboration — the New Model for High-Net-Worth Investors?

The second part of the problem: how does one protect principal if rates start to rise? We all know the irrefutable relationship between bond prices and interest rate — if rates go up, bond prices go down (all else being equal) and vice versa. The magnitude of this price change can be quantified by a bond’s duration. You can think of duration as beta for bonds. For example, a bond with a duration of 5 should decrease by 5% if rates increase by 1%. At the risk of being yet another voice in the choir calling for the eventual rise in rates, rates will eventually go up!! A quick review of the drivers of a bond’s performance exposes two components — income and principal. Going back to our 10-year Treasury with a 1.75% coupon and a duration of just over 9 suggests your return is wiped out with a mere .19% increase in rates (9 x 0.19 = 1.75). High yield bonds on the other hand have a 7.5% yield and a duration of 4.18. This combination offers a positive return with up to a nearly 1.8% increase in rates, a doubling from current levels (4.18 x 1.79% = 7.5).

Related: Central Banks Policies… Everyone Gets a Trophy

Voila, problem solved? Not so fast. High yield bonds are not without their risks. They can often behave a lot like stocks, moving in the same direction and offering little in the way of portfolio diversification. For example, high-yield bonds returned a negative 26.16% in 2008, offering little offset to the 37% decline in the S&P 500 that same year. In fact, since 1984, the high-yield index has declined in value in six years (1990, 1994, 2000, 2002, 2008 and 2015). The S&P 500 declined in 4 of those same years (1990, 2000, 2002, and 2008). Stocks generated small positive returns in 1994 and 2015.

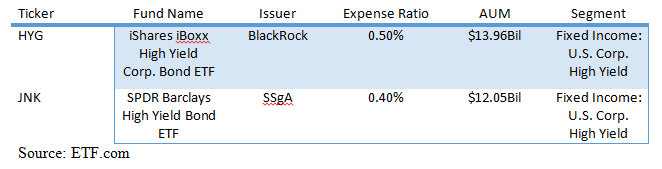

Additionally, buying individual bonds is not for the faint of heart. The markup associated with buying small quantities of bonds makes this route expensive for retail investors. High yield bonds have a fraction of the liquidity provided by stocks or Treasuries. For these reasons, we believe gaining exposure to this asset class is best achieved through the use of ETFs. A list of the largest high yield bond ETFs follows:

{kind=link}