Now let’s look more specifically at valuations within some select emerging market countries:

{kind=link}

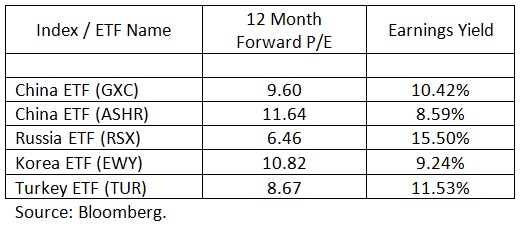

China, and even the China A Shares (if and when they become included in emerging markets ETFs), offer a compelling P/E ratio and earnings yield. Russia and Turkey offer extremely attractive valuations on paper but, of course, the degree of risk must be considered. Both Russia and Turkey represent extreme political risk, and particularly risk of currency collapse.

Even China now confronts talk by many that a crisis in its currency (and potentially a devaluation that would be a shock to global markets) is inevitable. Developed international or domestic markets simply don’t have this magnitude of risk.

The argument for emerging markets is bolstered further by the longer-term potential for mean reversion in returns.

Chart 1 below shows the difference in three year rolling performance between the MSCI Emerging Markets Index and the MSCI All Country World (ACWI) Index:

Back in 2005 and 2006 Emerging Markets outperformed the ACWI by over 20% over three years. Recently (as of Dec. 31, 2015) over a three year period Emerging Markets underperformed the ACWI by just under 15% per year.

That is dramatic underperformance, and emerging market’s comparative valuations indicate that there is at least the potential for returns to mean revert over the longer term.

Conclusions

At Clark Capital our experience has been that investing based solely on valuations can be completely ineffective over the short and intermediate terms. Rather, we look at valuations as assessments of opportunities and risk in projecting returns over the longer-term.

Given that viewpoint and the valuations picture discussed above, we would recommend the following for investors:

- Given the attractive valuations in emerging markets, investors willing to endure their substantial volatility may well be rewarded in the long-term. For long-term 10 plus year core positions, be sure that you are not underweight emerging markets. Emerging markets should represent 15 to 25% of your international allocations.

- Do not establish an overweight position in emerging markets until they have shown proven momentum and multiple quarters of outperformance.

- Consider adding the S&P Emerging Markets Small Cap SPDR (EWX) as part of an emerging markets allocation. EWX is the only emerging markets ETF that Morningstar classifies as small cap. Also, its holdings put it solidly in the mid cap / small cap value style box. Thus investors may benefit from a resurgence of the value factor and also the size factor (the small cap premium) in one holding that makes bullish bets on emerging markets.

- Consider reducing or removing currency hedges in emerging markets positions. When emerging markets equities are leading markets, often it is due to strong economic conditions in home countries and strong local currencies. Hedging the currency risk away substantially reduces potential returns.

- Consider supplemental, tactical positions in China and Korea, and for aggressive investors with strong stomachs, Russia and Turkey.

Mason Wev is a Portfolio Manager at Clark Capital Management Group, a Participant in the ETF Strategist Channel.

Past performance is not indicative of future results. This is not a recommendation to buy or sell a particular security. The opinions expressed are those of the Clark Capital Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Clark Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no guarantee of the future performance of any Clark Capital investment portfolio. It should not be assumed that any of the investment recommendations or decisions Clark Capital makes in the future will be profitable or equal the performance of the securities discussed herein. Material presented has been derived from sources consider to be reliable, but the accuracy and completeness cannot be guaranteed. The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services can be found in its Form ADV, which is available upon request. CCM-754