In our first article in this ETF Strategist series, we discussed a number of common current concerns among financial planning clients. These concerns can be collectively described as the “portfolio problem,” and more briefly recapped as follows:

- Equities are, arguably, the single most essential component of client portfolios — they represent the growth engine, the asset class most likely to keep clients ahead of inflation and allow their financial plans to succeed — but equities are subject to substantial volatility and significant downside risk

- The other asset classes in the portfolio — a primary purpose of which is to buffer the risk of the equity asset class — have become problematic and detrimental to portfolio performance

With respect to these other asset classes, our second article in the series focused on fixed income investments. In this third article, we turn our attention to the next most prominent non-equity asset class in most client portfolios: liquid alternatives.

Alternatives represent quite a diverse asset class, but generally include investments whose purpose is to provide a return (and risk) between that of equities and fixed income, and behavior uncorrelated with either asset class. We have heard some portfolio managers characterize their ideal “alt” as having an expected return of two-thirds that of equities but with only half the volatility. Alts had their birth in the world of hedge funds, and populating that space are such strategies as market neutral, absolute return, long/short (or hedged) equity, global macro, and various others, including hybrids. Liquid alts are those available to retail investors in forms such as ’40 Act mutual funds, which do not require the level of accreditation on the part of the investor, the lengthy lock-up periods, the exit gates, the high fees, or the large minimum investment amounts that typify hedge funds.

Over the last few decades, and spurred in part by the widely reported success of illiquid alts in the portfolios of several prominent university endowments, liquid alts have achieved mainstream status in the portfolios of non-institutional investors. They are now considered the third major asset class among retail investors, along with equities and fixed income.

In the context of the portfolio problem above, there are two concerns we have with the current state of liquid alts.

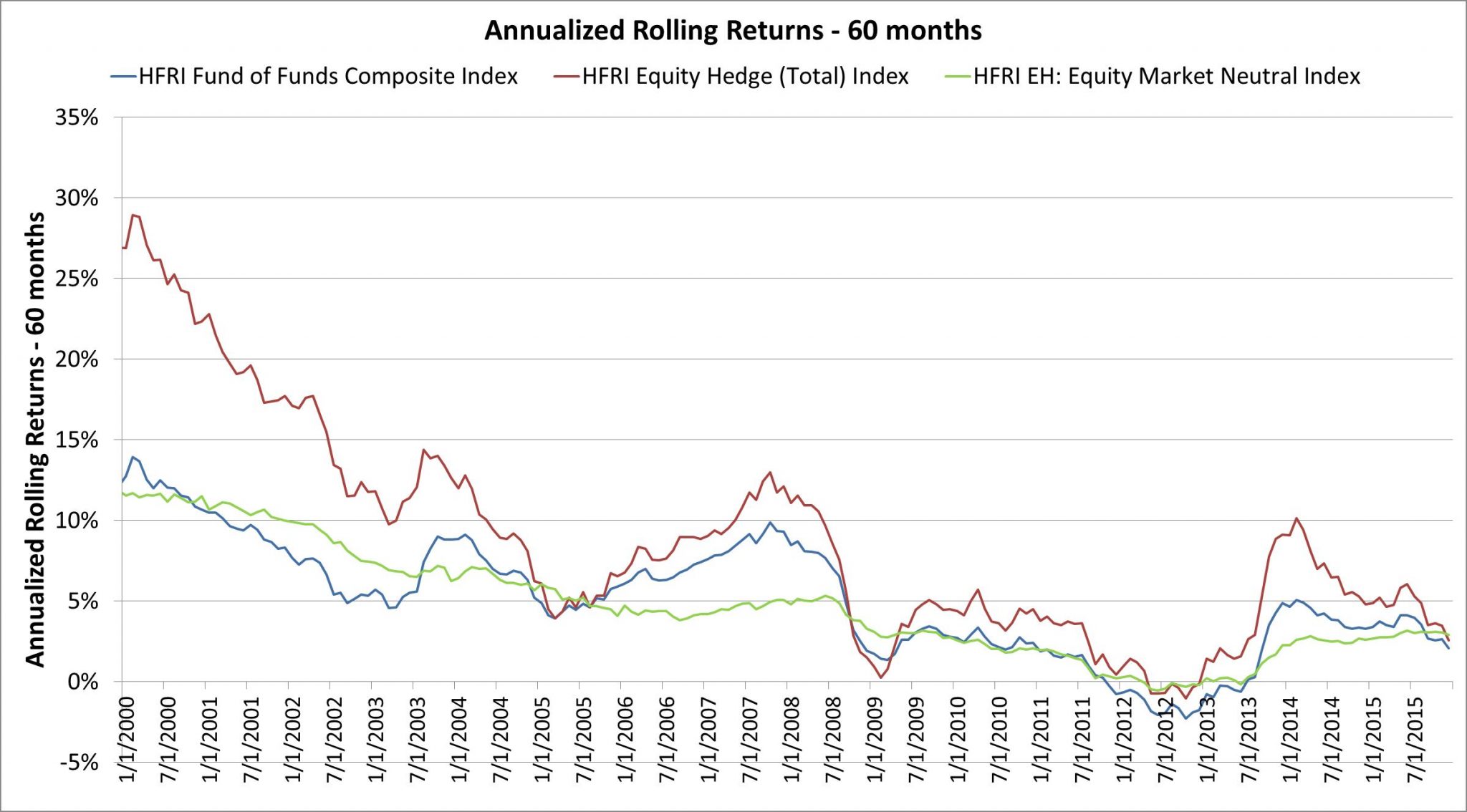

Our first concern is that with the growth in popularity of liquid alts has come a disturbing trend toward mediocrity. Now, given the diversity of strategies within this asset class, one must be careful not to paint its picture with too broad a brush; but, there is sufficient evidence based on the aggregate indexes that attempt to track performance of this class to give a discerning investor pause. The chart below plots the total return of three prominent indexes in the alt space compiled by Hedge Fund Research, Inc. (HFRI): the Equity Hedge Index, the Equity Market Neutral Index, and the Fund of Funds Composite Index. The returns shown are the average annual returns calculated on a rolling 60-month basis to reduce short-term “noise,” smooth out the effects of bull/bear market cycles, and make clear the long-term trend. The data series extends through December 31, 2015.

{kind=link}

Source: Giralda Advisors analysis of Bloomberg data

This picture, while far from predictive of course, concerns us. In our view, it indicates that liquid alts are co-culprits with fixed income investments in being prime contributors to the portfolio problem we cited above.

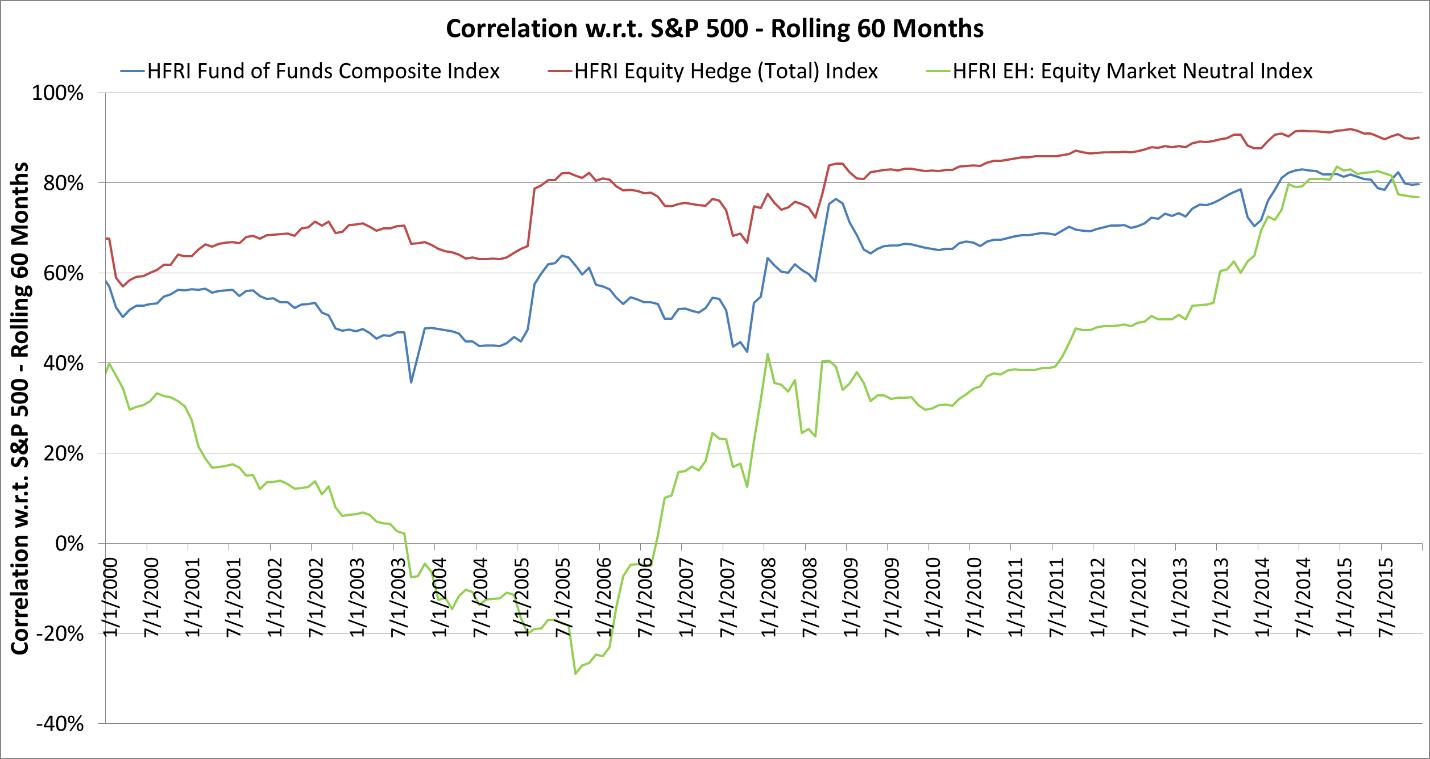

Our second concern is that liquid alts appear to be losing whatever diversification benefit they may have had. The chart below, using the same three HFRI indexes we just introduced, plots the rolling 60-month correlations of each of these indexes with the S&P 500 Stock Index.

{kind=link}

Source: Giralda Advisors analysis of Bloomberg data

Here again, the picture is disturbing. The correlations have trended upward over time into the neighborhood of 80% to 90%. To the extent that portfolio managers are relying on liquid alts to buffer the risk of equities in client portfolios, it would appear from this evidence that the asset class has failed to deliver. This erosion of diversification benefit is even more concerning to us than the erosion of return when we consider the portfolio problem. Making matters more pressing for advisors is the fact that clients have become quite vocal in their impatience with the poor performance of hard-to-explain investments that do not appear to be doing their fundamental job of portfolio risk reduction.

Enter RMI, the Risk-Managed Investing approach we introduced earlier in this series. Recall that the objective of RMI is to embed downside risk management explicitly into the equity investment itself. This, as we have pointed out, makes the portfolio less reliant on non-equity asset classes to do this job and attacks the portfolio problem more directly, right at its source. We submitted that the implications of this are paradigm-shifting and may change the way we think about portfolio construction, noting that “80/20 could be the new 60/40,” with RMI investments in the 80% portfolio component replacing part of the conventional equity exposure that constitutes the traditional 60% component.

For those investors not yet prepared to shift their portfolio-construction paradigm in this way (as promised, we’ll be delving into RMI in much more detail later in this series), let’s simply consider an RMI investment in direct “competition” with a liquid alt investment. If a portfolio manager considers successful a liquid alt strategy that delivers two-thirds of an equity return with half the volatility, then how might said manager regard RMI? A successful RMI strategy would deliver near-100% of an equity return and the volatility it removes would be the “bad” (i.e., downside) volatility. RMI would thus appear to be a category-killer in the liquid alt space.

In addition to exploring RMI’s broader potential to inspire the rethinking of portfolio construction, future installments in this series will investigate RMI’s role in mitigating “volatility drag” and “sequence of returns risk,” calibrate its tolerable cost, and discuss its implementation. We trust you will continue to find this discussion thought-provoking, and we look forward to your feedback along the way.

Jerry Miccolis is the Founding Principal and Chief Investment Officer at Giralda Advisors, a participant in the ETF Strategist Channel.