• Risk Reduction: Removing the euro risk from the equation significantly lowered the beta of European equities compared to U.S. equities. In fact, over the one-, three- and five-year periods, this index had a beta of less than 1, and the beta was approximately equal to 1 over the 10-year period.

• Incremental Risk of Euro Exposure: It is worth noting that for the 10-year period ending February 28, 2013, exposure to the euro increased the beta of European Equities by nearly 40%. Over shorter periods, this additional risk was even more pronounced.

Why Be 100% Unhedged?

When it comes to a currency such as the euro, I believe there will be cycles of both appreciation and depreciation against the U.S. dollar. Given the difficulty in predicting exactly when these cycles will turn, we question why typical allocations should always fully assume this currency risk. To me, an allocation that is 50% hedged and 50% unhedged—especially for someone without a strong view as to a currency’s future performance—would seem a better baseline to dial up or down from, depending on one’s conviction regarding the direction of any future currency trend.

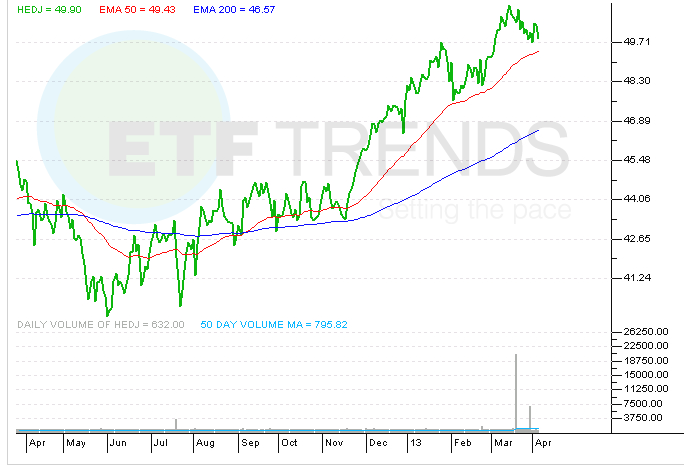

WisdomTree Europe Hedged Equity Fund (NYSEArca: HEDJ)

{kind=link}

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.

12/28/2003–2/28/2013.