I recently wrote a blog about how currency exposure—specifically to the euro—impacted volatility of European equities (the MSCI EMU Index over the last 10 years1). The central analytics of that blog measured the “beta” of European equities in local currency terms against European equities in U.S. dollars. The index measured in U.S. dollars includes the fluctuations of the euro against the U.S. dollar, which tends to increase its volatility.

I make a similar point in this blog but from a different perspective, specifically by measuring the beta of these European equities against the S&P 500 Index. This analysis highlights how sensitive European equities are to moves in the S&P 500—a common framework for evaluating investment strategies. Indexes with a beta greater than 1.0 relative to the S&P 500 Index have tended to be more sensitive, with the potential to magnify movements of this benchmark during the periods studied, while strategies with a beta below 1.0 have tended to exhibit lower sensitivity to those same movements.

Two Sources of Risk

For U.S. investors in international equities, there are traditionally two sources of volatility:

1) Volatility of equity prices

2) Volatility of the currency relative to the U.S. dollar

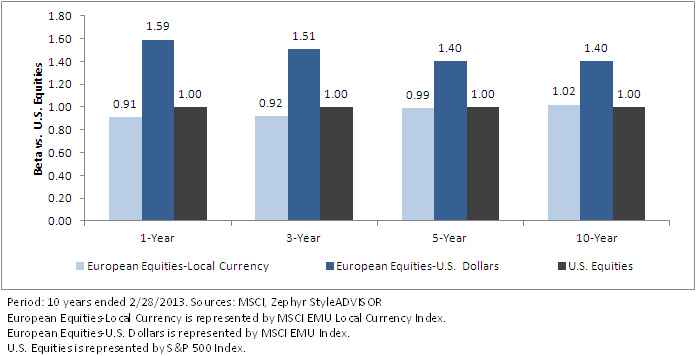

Oftentimes, U.S. equities appear less volatile than international equities—not because of volatility in their actual equity price movements, but rather because of the respective currency’s movements against the U.S. dollar. The chart below illustrates how much higher the beta (measured against the S&P 500 Index) of European equities is with euro exposure (meaning the incremental volatility from movements of the euro against the U.S. dollar) than without euro exposure.

How Euro Exposure Increased Volatility

{kind=link}