We are finding pockets of opportunity domestically, though we think that the broad U.S. equity market is expensive relative to its history. Our strategies are generally overweight the consumer discretionary, financials, and health care sectors. Moreover, we maintain our value bias despite it lagging growth this year. The outperformance of domestic growth stocks relative to domestic value this year has gotten extreme by historical standards, and it is rare to have this much divergence. Reversion to the mean is a powerful force in the equity markets, so we think that the recent outperformance of growth compared to value has mostly run its course. We expect our style to soon be in favor again.

Related: Why Investors Shouldn’t Fear Coming Volatility, But Use It To Their Advantage

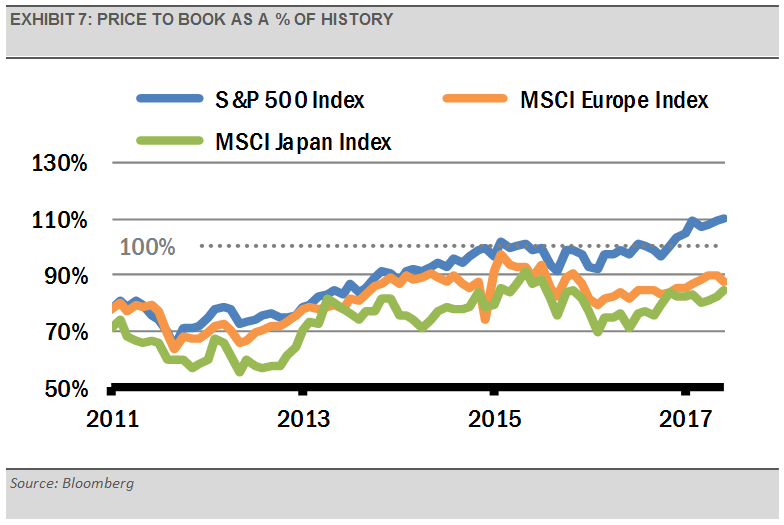

In addition, we see interesting opportunities in Europe and Japan, where economic fundamentals are improving over the near-term and valuations remain attractive (exhibit 7). We are not long-term bulls on either Europe or Japan, but find them favorable for the time being.

Stock market volatility has been subdued lately and is currently well below its historical average. Political headlines and other sources of potential risks will likely have a greater impact on the markets, so we expect a corresponding uptick in equity market volatility going forward.

These risks may translate to negative days or weeks in the global equity markets. We think that investors should take advantage of down markets as long as developed market fundamentals remain solid.

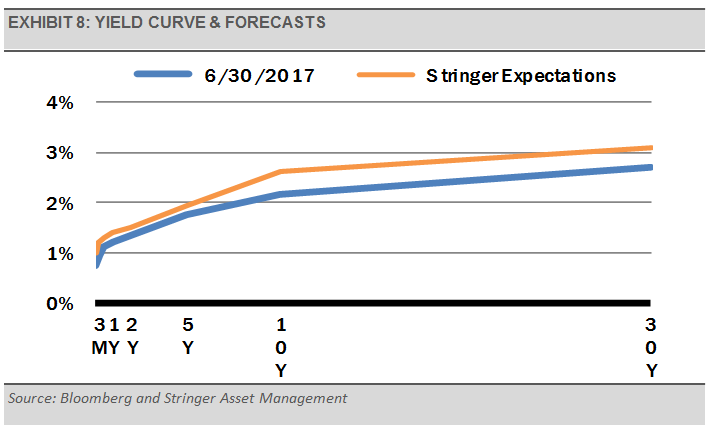

In the fixed income market, short-term interest rates should stabilize from here while long-term interest rates should be range bound near the current level (exhibit 8). As the Fed lets its balance sheet shrink, we expect some areas of the fixed income market, such as mortgage-backed securities, to underperform the broad fixed income market as that space adjusts to the new reality. We are finding more attractive investment opportunities elsewhere in traditional fixed income and in the alternative investments area.

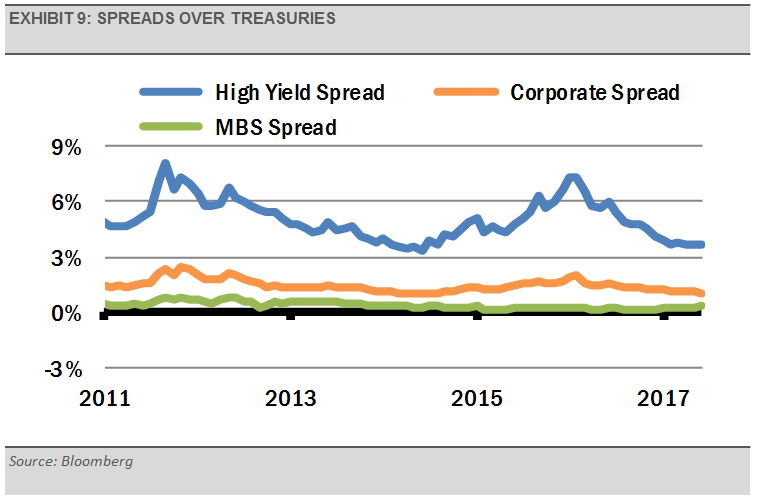

Credit spreads, which is the difference between the Treasury Bond yield and the yields of other fixed income investments of similar duration, are one measure of relative value. We think that credit spreads are tight (exhibit 9), so we have pared back our corporate bond and mortgage-backed exposures and have little allocation to high-yield bonds. We are finding several potential return enhancing and risk management opportunities in broadly diversified ETFs that blend allocations to REITs, MLPs, dividend-paying equities, and corporate bonds, as well as more focused, outside of the mainstream holdings, like convertible bonds, bank loans, and preferreds.

In summary, with an eye towards risk management, we are positioned to benefit from solid global economic growth. We expect volatility and market dips, but as long as fundamentals remain solid, we see potential dips as buying opportunities.

THE CASH INDICATOR

The Cash Indicator (CI) has declined to the low end of its historic range. While we expect market volatility to increase, the current level of the CI suggests that the environment for raising significant cash is a long way off.

This article was written by Gary Stringer, CIO, Kim Escue, Senior Portfolio Manager, and Chad Keller, COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.