This year is already looking brighter for China than last, with projections of around 5% growth seen as the result of the country ending its zero-COVID rules and rebounding in 2023. Within that growth is a deeper trend, however, that speaks to the country’s changing relationship with foreign markets that may produce more durable growth moving forward. According to new insight from Franklin Templeton, China’s domestic consumption could be a key driver for growth this year and moving forward.

The research from Christy Tan, investment strategist at the Franklin Templeton Institute, explained three key factors to this trend story in China: The country’s domestic consumption offers the biggest upside, its new administration may be looking at a consumption-led model for growth, and that government spending has a more natural relationship with consumer spending.

See more: “China Valuations, Alibaba News Boosts the Case for FLCH”

For one, China’s gross savings rate is one of the highest in the world, and savings grew by a whopping $2.5 trillion last year, perhaps as millions stayed home rather than going out to spend as part of the country’s zero-COVID safety measures. Per Tan, this may reflect the period between 2010 and 2019 when private consumption grew 5% despite almost no movement in household income as a share of GDP.

That comes as China’s government is turning towards a consumption-driven model for the economy, with tax and fee costs dropping for businesses by $261 billion and extended cuts and boosts for companies worth $173 billion on top of that. Finally, a possible recessionary environment in Europe and the U.S. could be mitigated for a traditionally export-driven Chinese economy if it does indeed lean more on consumer spending.

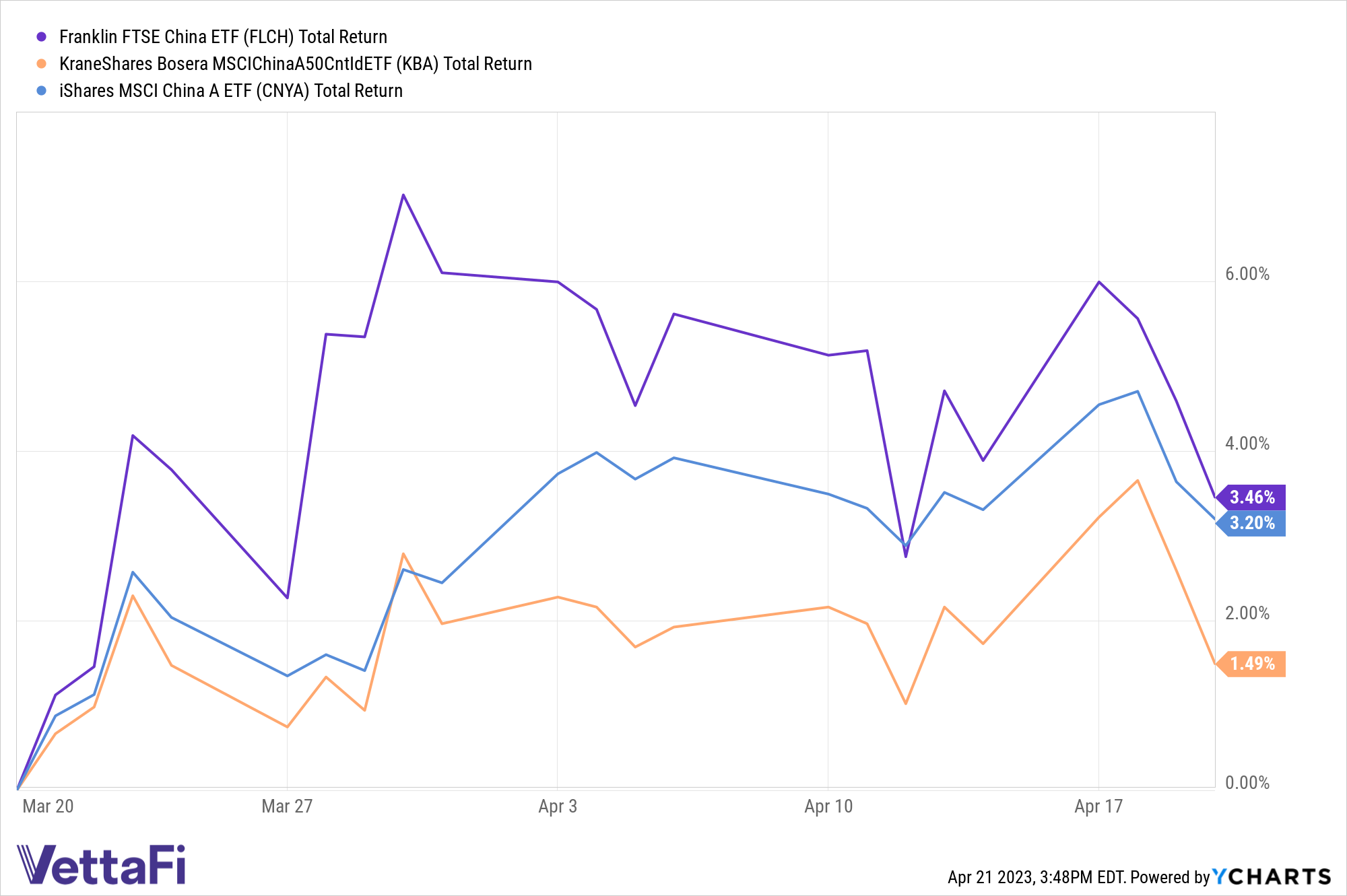

All of these trends are worth watching, and for those investors looking at an allocation to China this year, it may be worth considering a low-fee China ETF like the Franklin FTSE China ETF (FLCH), which charges just 19 basis points to track the FTSE China RIC Capped Index. With exposure to mid- and large-cap firms, it returned 3.5% over the last month, according to YCharts:

China may be one of the bright spots this year if the U.S. does face a recession, and with slowing earnings representing the central “yes or no” narrative in earnings season right now, stressed out investors and market watchers may want to consider how FLCH can ride China’s domestic consumption.

For more news, information, and analysis, visit the Volatility Resource Channel.

VettaFi is an independent publisher and takes responsibility for our edit staff, research, and postings. Franklin Templeton is not affiliated with VettaFi and was not involved in drafting this article. The opinions and forecasts expressed are solely those of VettaFi and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.