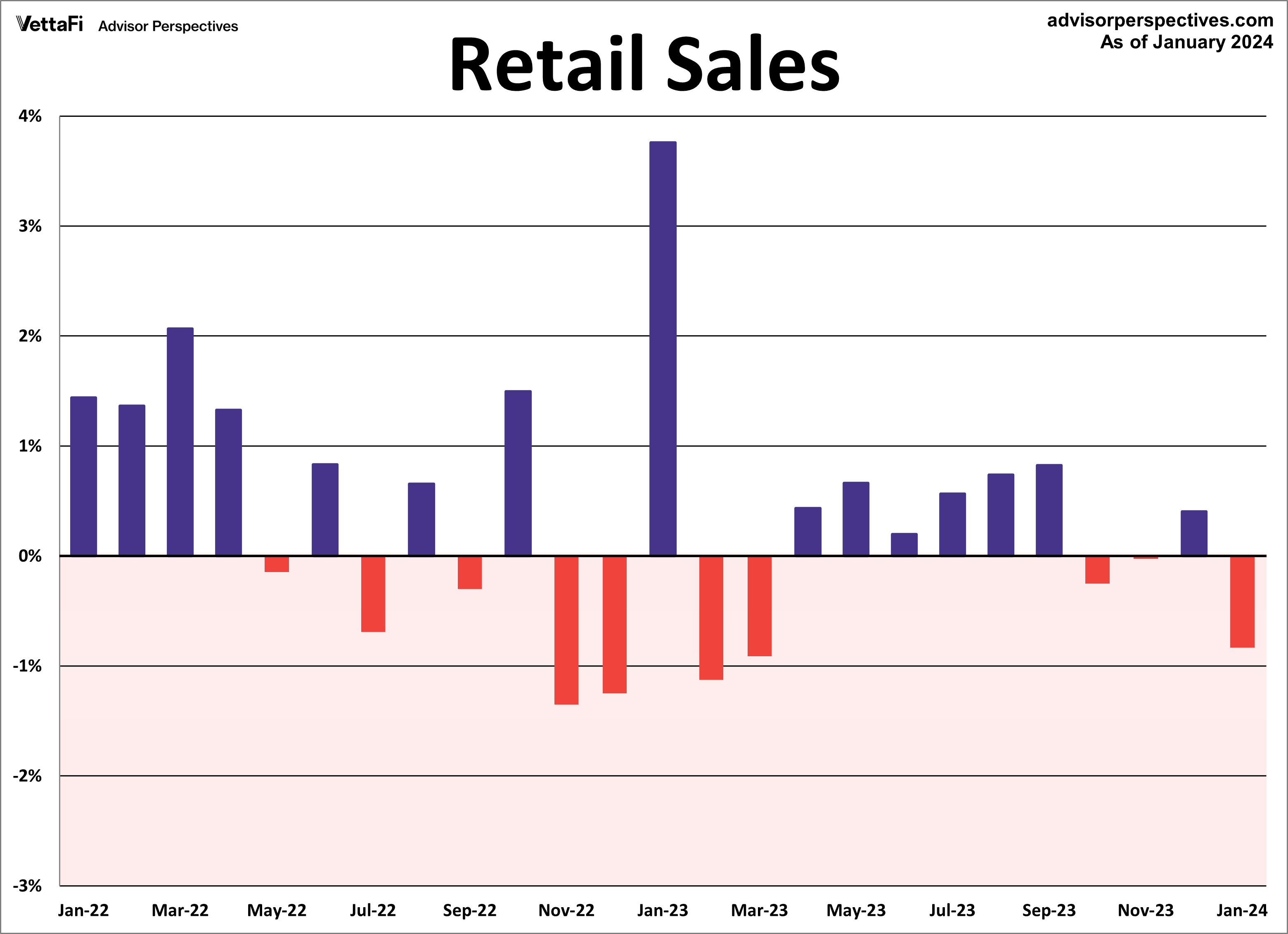

The Census Bureau’s Advance Retail Sales Report for January revealed a 0.8% drop in headline sales compared to December. That was the largest monthly pull back in consumer spending since March. The latest decline was much larger than the anticipated 0.2% monthly decline.

For an inflation-adjusted perspective on retail sales, take a look at our Real Retail Sales commentary.

Here is the introduction from today’s report:

Advance estimates of U.S. retail and food services sales for January 2024, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $700.3 billion. That’s down 0.8 percent (±0.5 percent) from the previous month, and up 0.6 percent (±0.7 percent)* above January 2023. Total sales for the November 2023 through January 2024 period were up 3.1 percent (±0.5 percent) from the same period a year ago. The November 2023 to December 2023 percent change was revised from up 0.6 percent (±0.5 percent) to up 0.4 percent (±0.3 percent).

Retail trade sales were down 1.1 percent (±0.5 percent) from December 2023, and down 0.2 percent (±0.5 percent)* below last year. Nonstore retailers were up 6.4 percent (±1.6 percent) from last year, while food services and drinking places were up 6.3 percent (±2.3 percent) from January 2023.

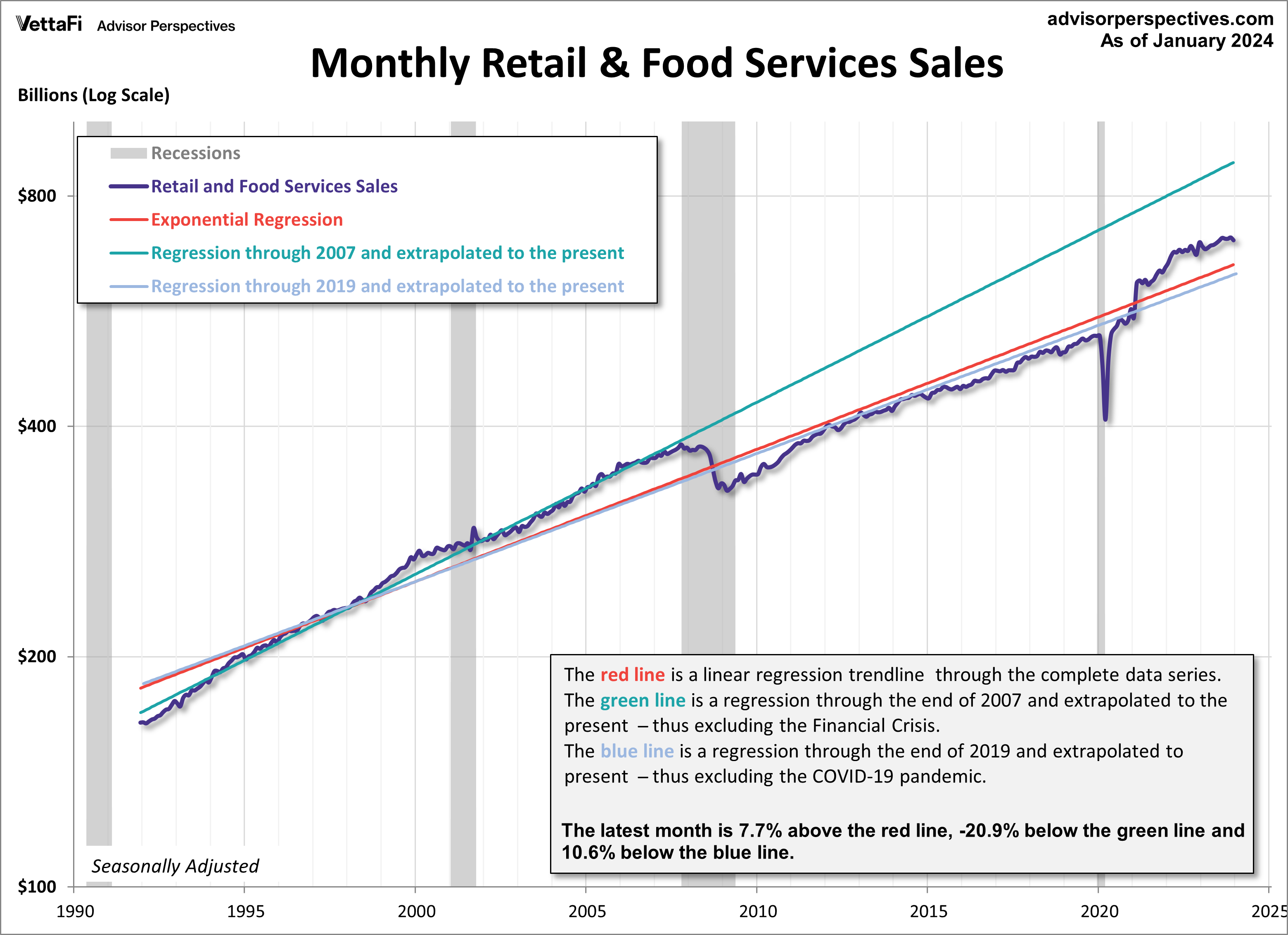

The chart below is a log-scale snapshot of retail sales since the early 1990s. The three exponential regressions through the data help us to evaluate the long-term trend of this key economic indicator.

- The red line is a linear regression through the complete data series.

- The green line is a regression from the start of the series through the end of 2007. It is then extrapolated to the present – thus excluding the Financial Crisis.

- The blue line is a regression from the start of the series through the end of 2019. It is then extrapolated to the present – thus excluding the COVID-19 pandemic.

Monthly retail sales have been above the red and blue line since March 2021. That signals increased consumer spending that was most likely pent up as a result of the pandemic.

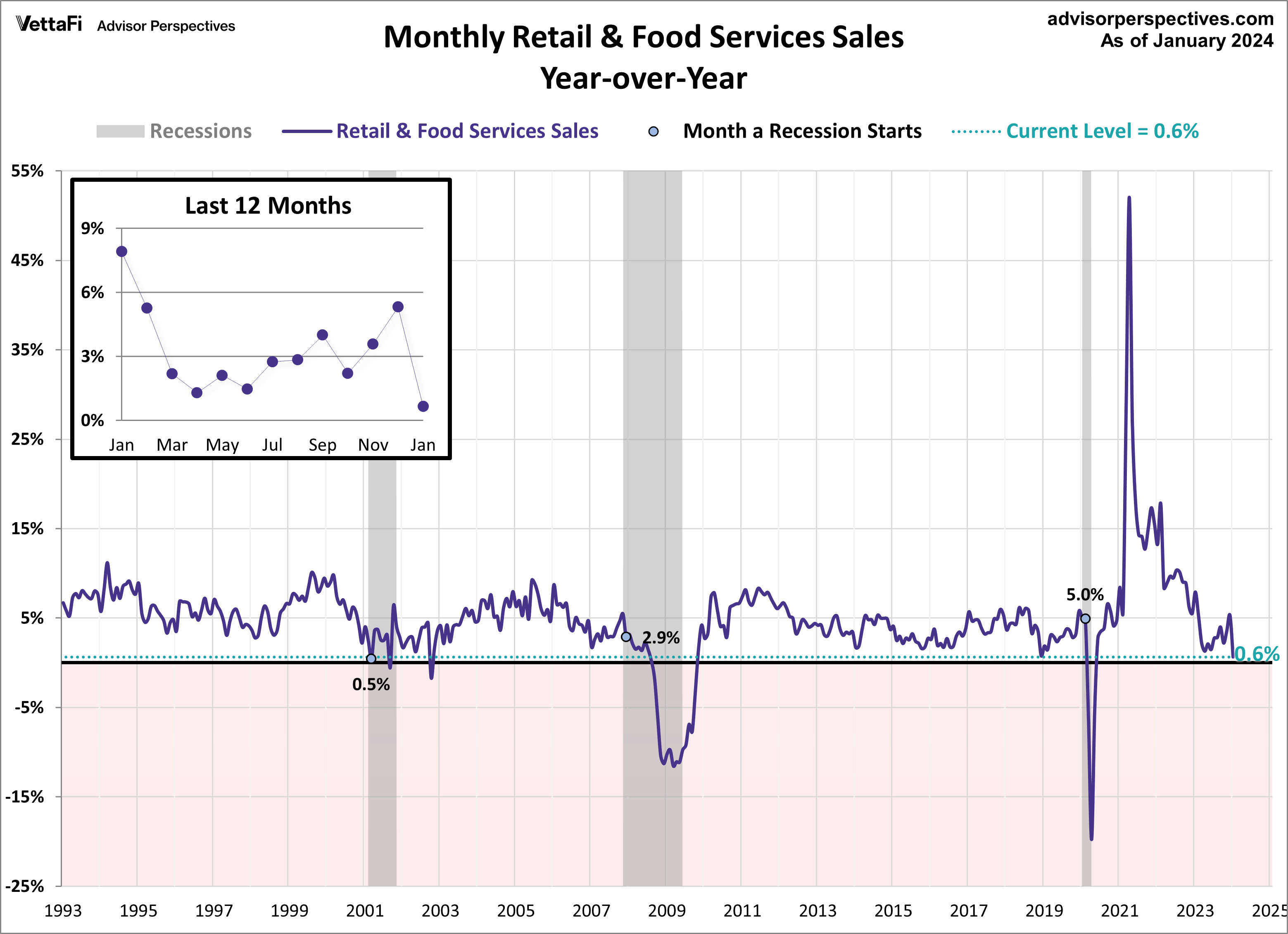

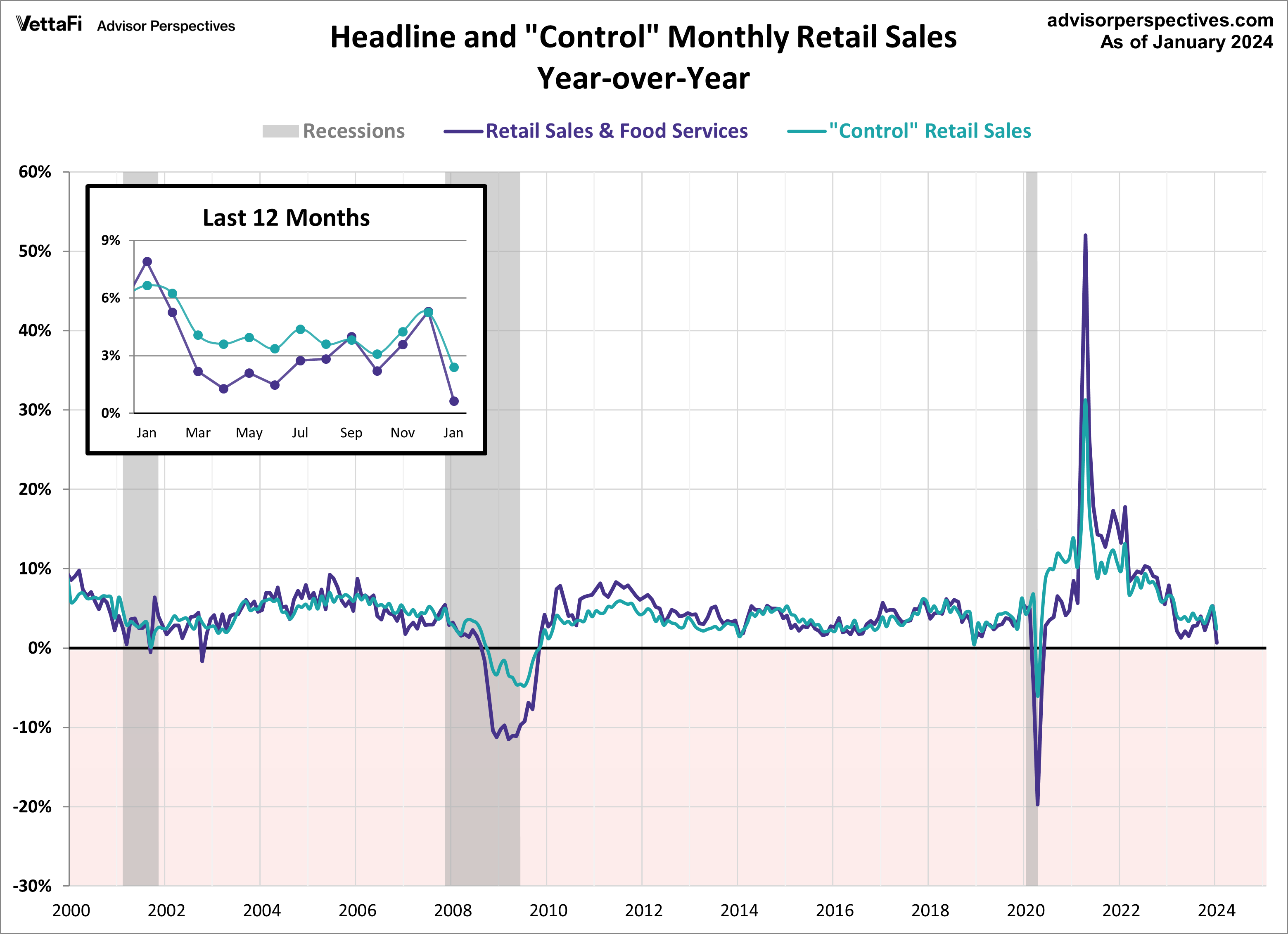

The year-over-year percent change provides another perspective on the historical trend. Current retail sales are up 0.6% compared to January 2023, the lowest level since May 2020. Here is the headline series with a callout to the most recent 12 months.

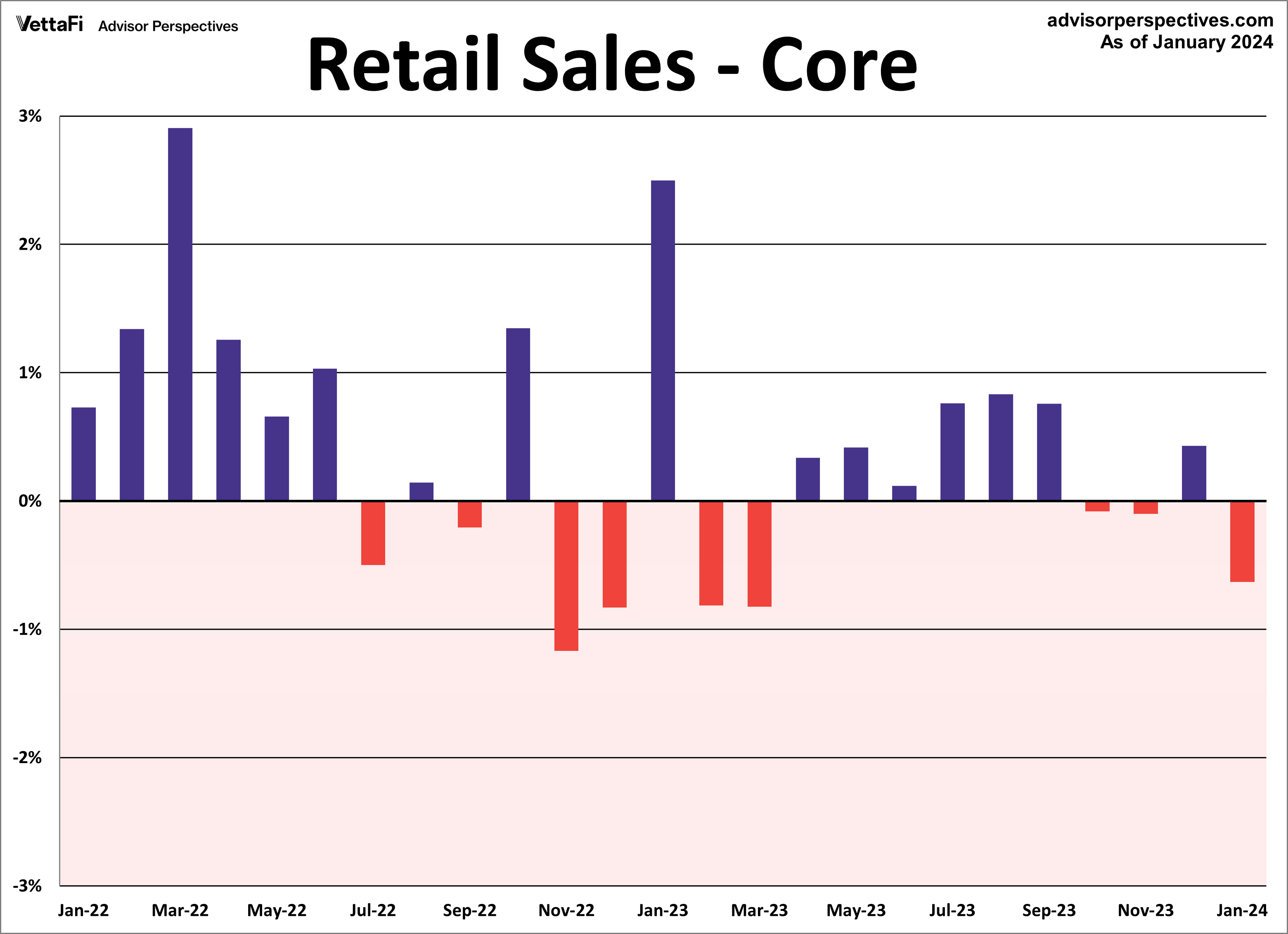

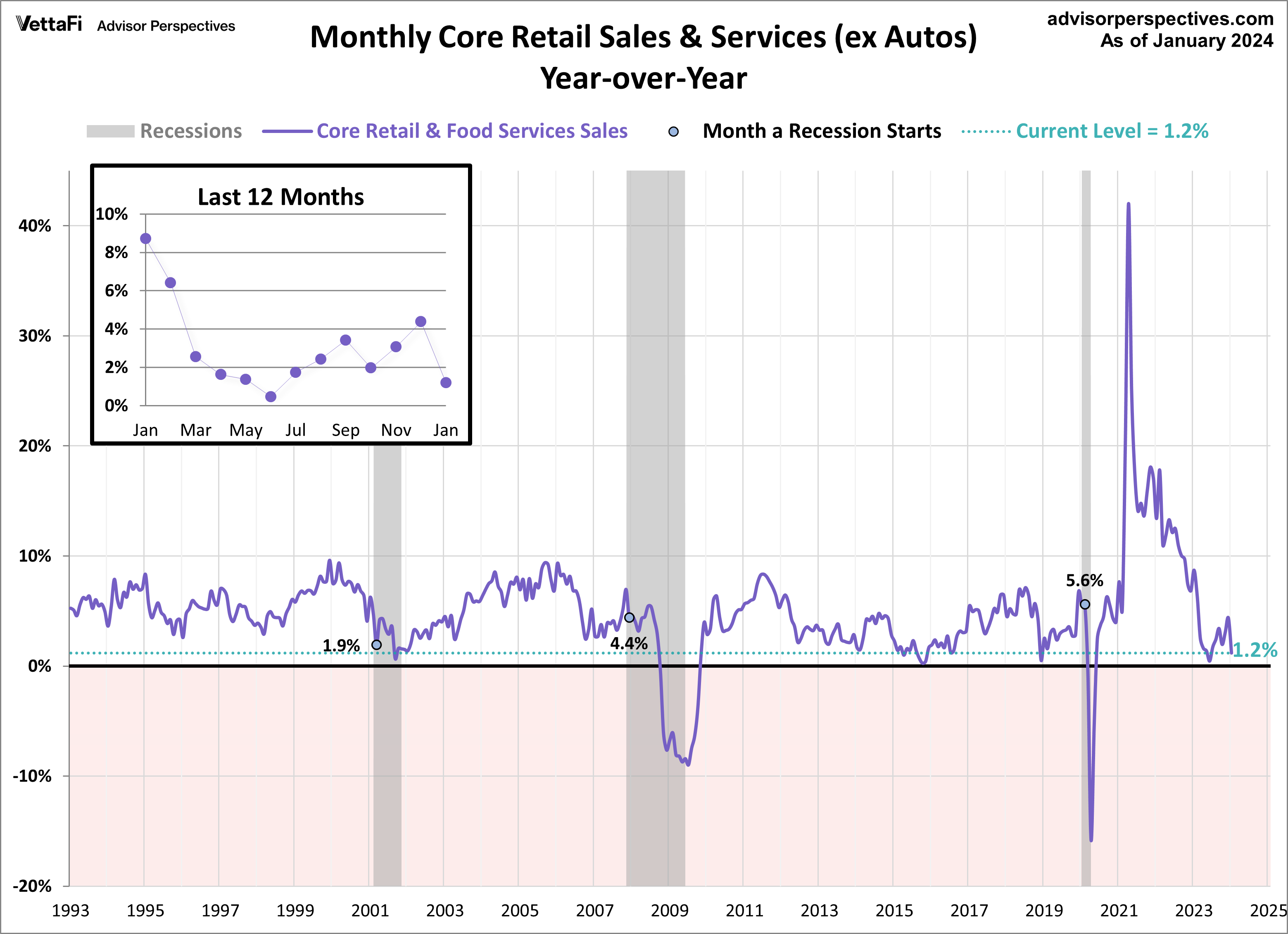

Core Retail Sales

Core sales (ex Autos) also fell short of expectations by decreasing 0.6% in January compared to the expected 0.2% growth.

And core retail sales are up 1.2% compared to January 2023. Here is the year-over-year chart of core retail sales with a callout to the most recent 12 months.

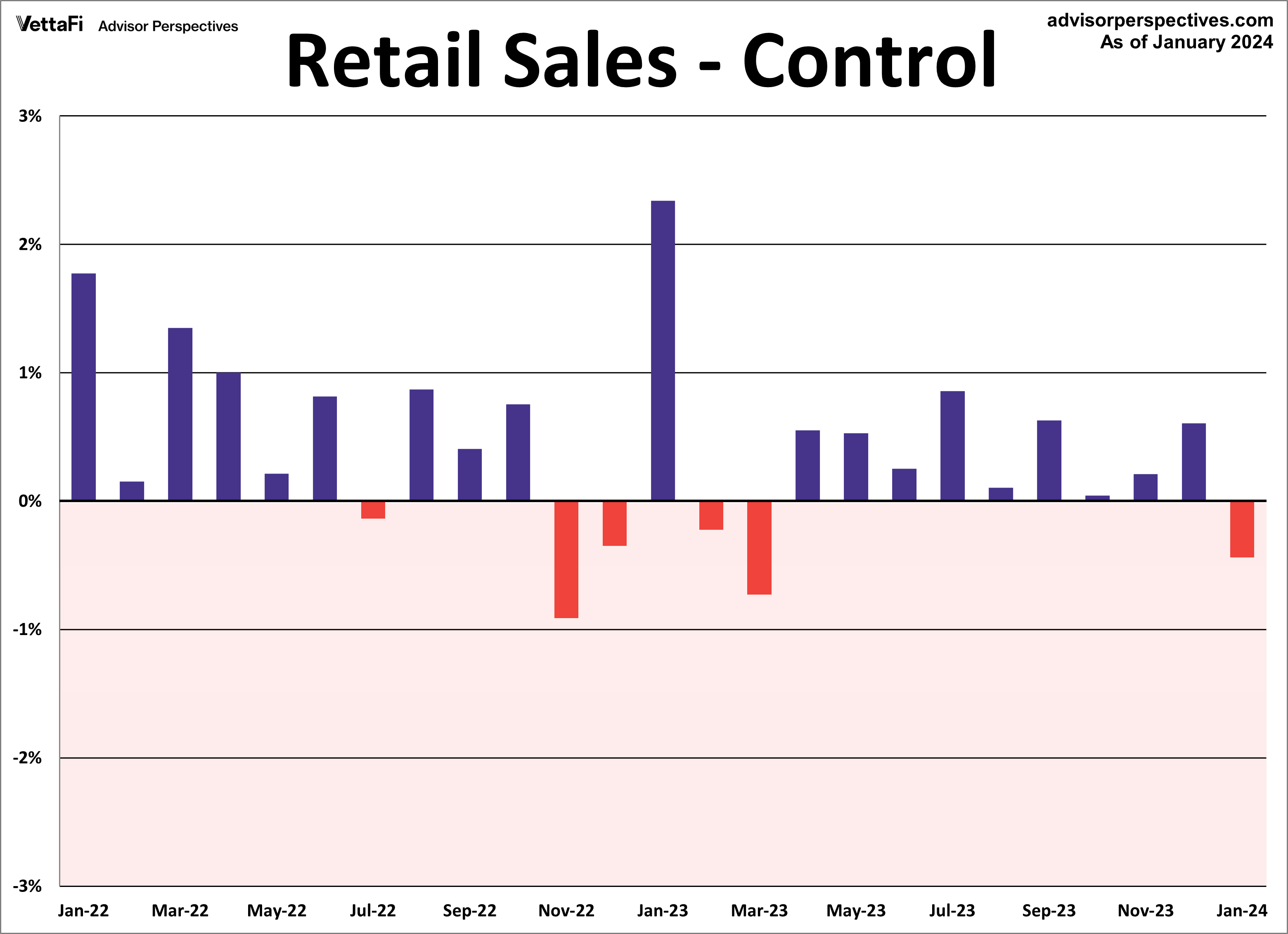

Retail Sales: “Control” Purchases

The next two charts illustrate retail sales “control” purchases, which is an even more “core” view of retail sales. This series excludes motor vehicles & parts, gasoline, building materials as well as food services & drinking places. The popular financial press typically ignores this series, but it’s a more consistent and reliable reading of the economy. Retail sales control purchases decreased 0.4% in January, lower than the expected 0.2% growth.

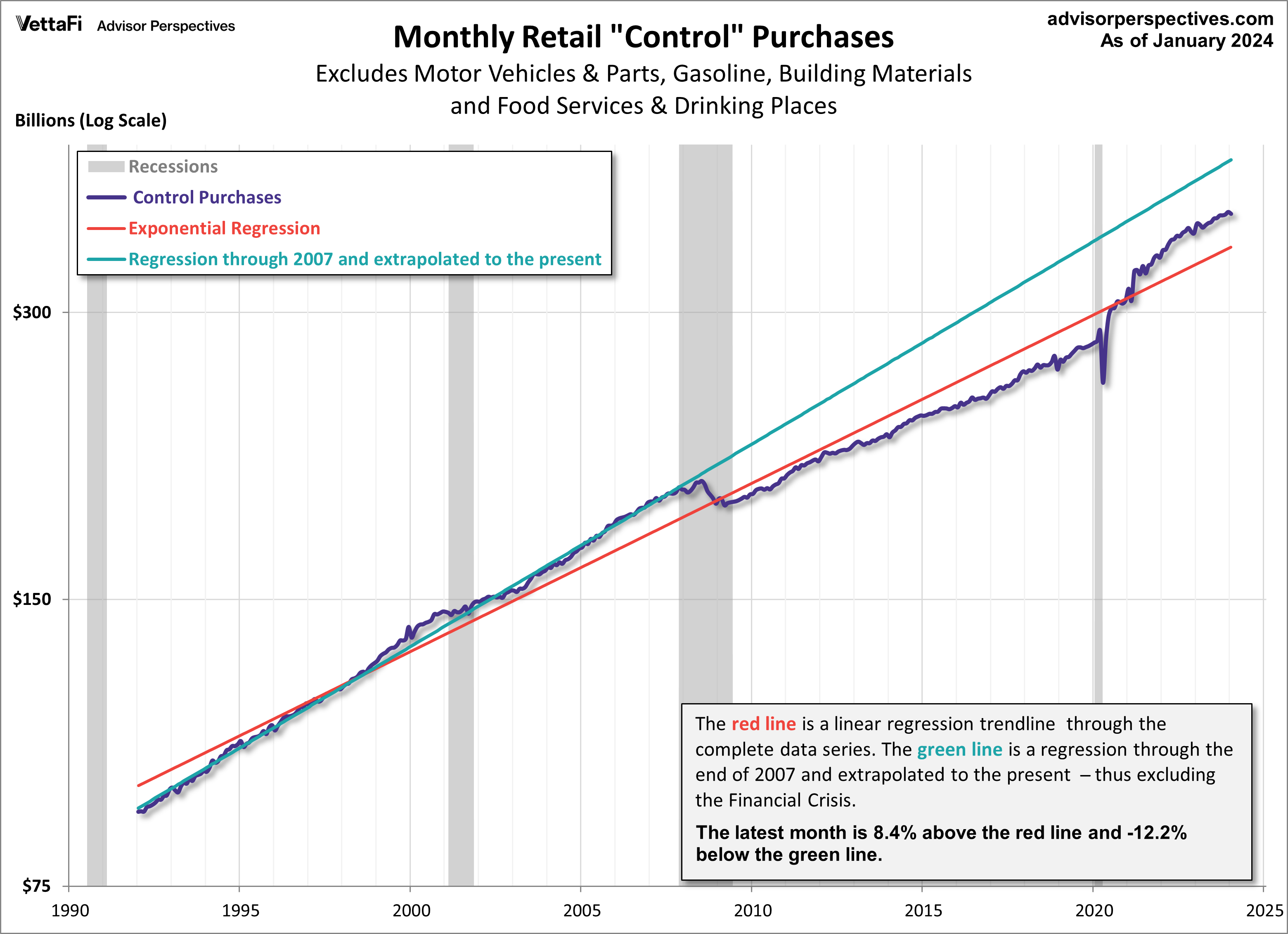

Similar to the retail sales snapshot chart earlier, the chart below is a log-scale snapshot of control purchases since the early 1990s. It includes two of the exponential regressions previously mentioned.

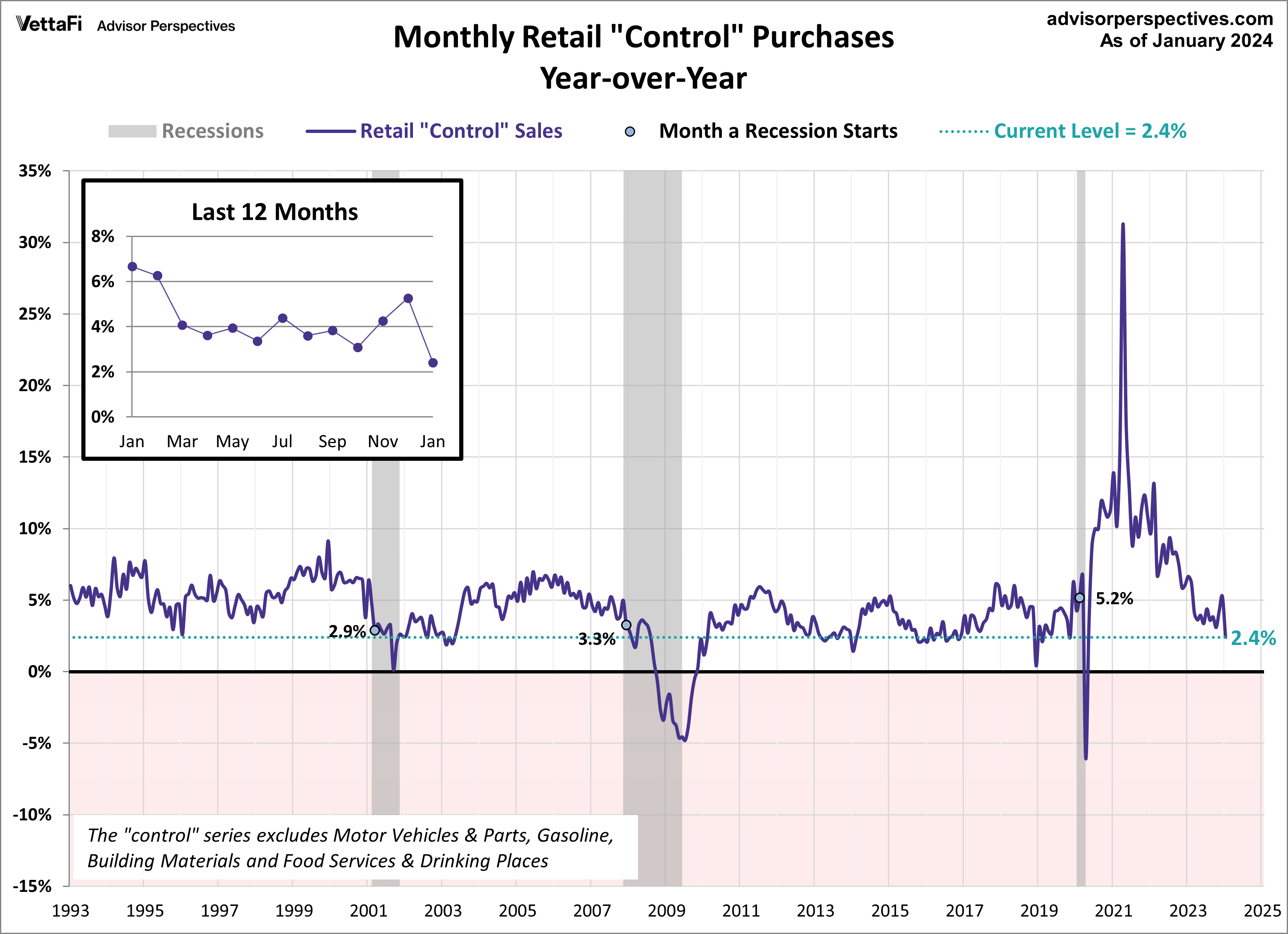

Here is the same series year-over-year. Current control purchases are up 2.4% compared to January 2023, the lowest level since April 2020.

For a better sense of the reduced volatility of the “control” series, here is a YoY overlay with the headline retail sales. Note that the two series follow each other closely. But headline sales have more extreme highs and lows than the control series.

Bottom Line: Retail sales fell more than expected in January. All three series (headline, core, and control) revealed decreased consumer spending.

Retail sales will impact interest in the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

VettaFi LLC (“VettaFi”) is the index provider for IBUY, for which it receives an index licensing fee. However, IBUY is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of IBUY.

For more news, information, and strategy, visit the Beyond Basic Beta Channel.