By Joe Foster, Portfolio Manager and Strategist for VanEck

Consolidation Looms but Risks Loom Larger

Since June, the gold price has enjoyed a relentless advance of over $250 per ounce, to a six-year high of $1,557 on September 4, then spent the rest of September consolidating around the $1,500 level. The gold price found support on September 12 when the European Central Bank (ECB) joined the U.S. Federal Reserve Bank (Fed) in a monetary about-face by easing policy nine months after signaling it was done with ever-looser policies. The ECB cut deposit rates to minus 0.5% and will start buying $22 billion worth of debt beginning in November to try to avoid a Euro-zone recession. Also, gold was supported by a missile and drone attack on a large Saudi oil facility that knocked out 5% of global oil supply.

Systemic risk surfaced when the overnight repo market lacked the liquidity to handle the confluence of a corporate tax payment with the settlement of a U.S. Treasury debt auction on September 17. Banks refused to lend as repo rates trended as high as 10% and the Fed was forced to inject billions of dollars into the financial system to address the squeeze. Post-crisis banking rules, the Treasury’s voracious appetite for cash and the Fed’s management of its trillions of dollars of balance sheet securities created unintended consequences that have been resolved for now. However, it begs the question as to how financial markets will behave under a less benign variety of systemic stress.

The gold price was kept in check as trade tensions with China eased somewhat when the two sides agreed to talks in October. Gold faced further headwinds as the S&P 500[1] came within a hair of its all-time high on September 19 and the U.S. Dollar Index (DXY)[2] trended to a new 28-month high on September 30. We wonder who is investing in U.S. assets amid all of the impeachment chaos, systemic stress, and fiscal irresponsibility. Perhaps the machines really have taken over.

The gold market showed resilience until September 30, when dollar strength seemed to overwhelm the metal. We have been wondering whether an interim correction in the gold price would come at $1,500 or at higher levels. We now have the answer as gold fell $47.91 (3.2%) in September to $1,472.39, and it looks like October is shaping up to be a month of correction. Gold stocks also gave back some gains as the NYSE Arca Gold Miners Index (GDM)[3] fell 10.0% and the MVIS Global Junior Gold Miners Index (MVGDXJ)[4] declined 11.2%.

Gold Continues to Beat Expectations

The upward move in gold prices so far this year has caught most investors by surprise. There have been strong inflows to the bullion exchange traded products (ETPs), yet anecdotally, we have seen little flows into gold equity funds. For many, this move harkens back to the first half of 2016 when the gold price advanced $260 and the GDM doubled. However, the 2016 move wasn’t sustained, and gold and gold stocks pulled back and went nowhere for three years. Equity investors are now understandably cautious and reluctant to step in. With the correction now in motion, it looks like we will soon find out whether 2019 was another flash-in-the-pan or the beginning of a new bull market. The macro backdrop today is much more supportive than it was in 2016. Both the expansion and the general equity bull market are now the longest on record. Global growth is slowing materially. Real rates have been falling and are expected to continue falling for the foreseeable future. Negative-yielding debt has reached an astronomical $15 trillion globally and is growing. Global leadership seems to keep getting worse.

Prior to 2019, $1,365 was the established upside resistance level for gold. Once upside resistance is broken, it often becomes downside support. Therefore, in the current correction, gold could pull back to $1,365 and still maintain a strong bull market trend. It is equally possible that gold might consolidate at higher levels, say in the $1,400 to $1,450 range. The duration of this correction might take as little as a month or continue to year-end. While we will only know the details in hindsight, the strong macro drivers in place suggest this correction will only be a bump in the road, not the end of the line. Also, given gold’s 2019 performance, we will not be surprised if it continues to beat our expectations.

Capital Discipline a Welcome Surprise

We attended the Denver Gold Forum in September and met with a range of companies. Despite the high gold prices, there was no sense of euphoria, and the overall message was one of sound business fundamentals. We asked every producer we met with how they would deal with the generous cash flows they would enjoy this year and possibly beyond. Some plan on reducing debt further, while others are deciding on proper dividend policies. We expect exploration budgets to increase and some reinvestment into sustaining the business. Companies expect to hold the line on costs by maintaining cutoff grades and continue using a $1,200 price to plan their operations. We therefore believe profit margins may increase with gold prices.

A priority was placed on organic growth through brownfields expansion and/or increasing reserve lives. Companies were not talking about expansions through M&A or large greenfields development. These were the main sources of value destruction in the last bull cycle when companies overpaid for acquisitions and developed properties that required too much capital. Given the newness of $1,500 gold, the real test will come at the next Denver Gold Forum. If the gold price remains elevated and if companies are still exhibiting strong capital discipline while containing costs, we will be very happy investors.

Gold’s Top Producers Showcase Impressive Developments

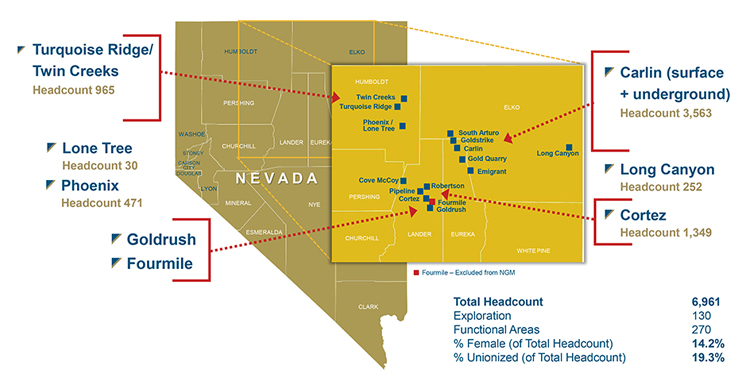

After a week of meetings at the Denver Gold Forum and the Precious Metals Summit, we traveled to northern Nevada to attend the first analyst tour of Nevada Gold Mines (NGM), the joint venture (JV) between Barrick (61.5%) and Newmont (38.5%) that was created in July. Barrick is the operator and led the three-day tour that covered most of NGM’s operations. The map shows NGM has three major mining centers – Carlin, Cortez, and Turquoise Ridge/Twin Creeks. The three centers are roughly a one- to two-hour drive from each other. Each has open pit and underground mines and multiple processing facilities that are able to treat a variety of ore types.

Barrick announced a maiden five-year production guidance of 3.5 – 3.8 million ounces per year, making NGM one of the largest gold producers in the world. It looks to us like the drilled footprint of several high-grade underground deposits should enable the operations to maintain this level of production for at least 10 years. The most impressive upside, in our view, is from the Goldrush and Fourmile deposits at Cortez. Goldrush has a high-grade resource of 14.3 million ounces and plans are being made to start mining in 2022. Fourmile is a Barrick deposit adjacent to Goldrush that will probably eventually be vended into NGM. The Fourmile resource is only 700,000 ounces, but recent drill results suggest it may ultimately rival Goldrush in size.

Barrick has implemented a huge change in corporate culture at NGM. Layers of management have been eliminated with a shift in focus to key leaders. Silos have been broken down and inter-departmental communication, problem solving, idea generation, and profitability are driving the company. Geoscience has been elevated in importance with the aim of building better, more efficient mines and processing alternatives. An aggressive exploration program should result in more discoveries. A motto of the company is “run hard, expose your weakness, fix your weakness”.

The changes in management and culture have created employee turnover and challenges for some to adapt. However, we found that Barrick is building a team that is technically superior, working together and enthusiastic—a workforce that will transform Nevada from a tired old mining jurisdiction to a vibrant model of efficiency. So far we believe the operational synergies they have found are impressive. This year NGM has realized $240 million in savings from integrated planning, supply chain, transport and general/administrative. As we toured the Carlin operations, where most of the processing capacity is located, we could see first-hand how moving equipment, managing stockpiles, transporting ore and processing options have all become more efficient in the JV. Ultimately the company aims to find another $240 million in savings.

Download Commentary PDF with Fund specific information and performance.

IMPORTANT DISCLOSURE

All company, sector, and sub-industry weightings as of September 30, 2019, unless otherwise noted.

[1] S&P 500 Index measures the stock performance of 500 large companies listed on stock exchanges in the United States and covers approximately 80% of available market capitalization.

[2] U.S. Dollar Index (DXY) indicates the general international value of the U.S. dollar by averaging the exchange rates between the U.S. dollar and six major world currencies.

[3] NYSE Arca Gold Miners Index (GDMNTR) is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining for gold.

[4] MVIS Global Junior Gold Miners Index (MVGDXJTR) is a rules-based, modified market capitalization-weighted, float-adjusted index comprised of a global universe of publicly-traded small- and medium-capitalization companies that generate at least 50% of their revenues from gold and/or silver mining, hold real property that has the potential to produce at least 50% of the company’s revenue from gold or silver mining when developed, or primarily invest in gold or silver.

Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

Any indices listed are unmanaged indices and include the reinvestment of all dividends, but do not reflect the payment of transaction costs, advisory fees or expenses that are associated with an investment in a Fund. Certain indices may take into account withholding taxes. An index’s performance is not illustrative of a Fund’s performance. Indices are not securities in which investments can be made.

Please note that the information herein represents the opinion of the author, but not necessarily those of VanEck, and this opinion may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

About VanEck International Investors Gold Fund (INIVX): You can lose money by investing in the Fund. Any investment in the Fund should be part of an overall investment program, not a complete program. The Fund is subject to the risks associated with concentrating its assets in the gold industry, which can be significantly affected by international economic, monetary and political developments. The Fund’s overall portfolio may decline in value due to developments specific to the gold industry. The Fund’s investments in foreign securities involve risks related to adverse political and economic developments unique to a country or a region, currency fluctuations or controls, and the possibility of arbitrary action by foreign governments, or political, economic or social instability. The Fund is subject to risks associated with investments in Canadian issuers, commodities and commodity-linked derivatives, commodities and commodity-linked derivatives tax, gold-mining industry, derivatives, emerging market securities, foreign currency transactions, foreign securities, other investment companies, management, market, non-diversification, operational, regulatory, small- and medium-capitalization companies and subsidiary risks.

Diversification does not assure a profit or protect against loss.

Please call 800.826.2333 or visit vaneck.com for performance information current to the most recent month end and for a free prospectus and summary prospectus. An investor should consider a Fund’s investment objective, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this as well as other information. Please read them carefully before investing.

©2019 VanEck