By William Sokol, Director of Product Management

Bond investors typically look to their core bond portfolios to provide a ballast against market volatility. However, core fixed income asset classes continue to feel the impact of “higher for longer” this year, as market expectations for rate cuts have adjusted to what the Fed has been telling us all along. Robust economic data over the past few weeks, and some upside inflation surprises, continue to support that outlook. By early April, the yield on the 10-year U.S. Treasury had risen by almost 50 basis points since their recent lows at the end of December. We don’t know if long-term bond yields will continue rising or decline from here, but we do expect rate volatility to remain elevated relative to the decade prior to this most recent rate hiking cycle.

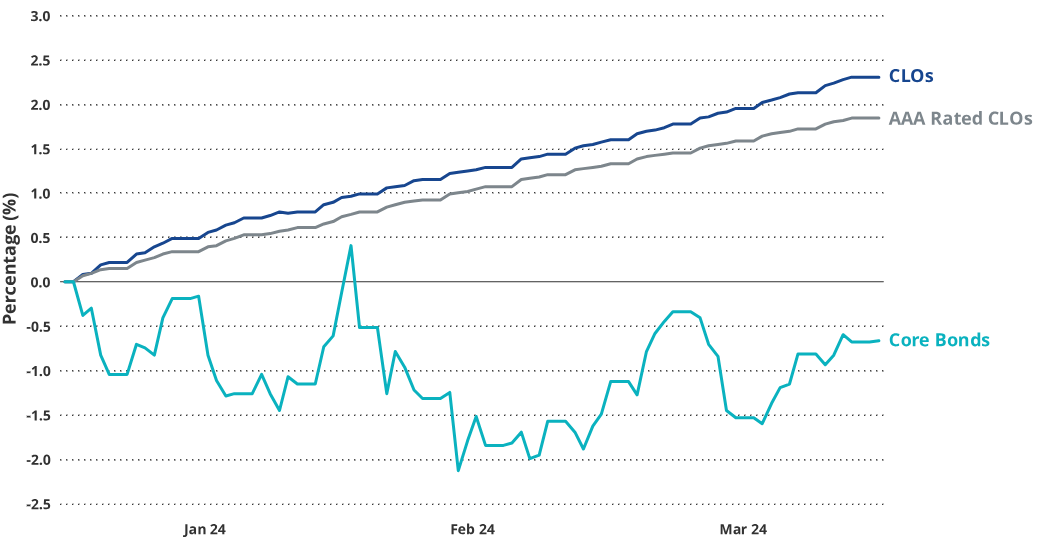

This recent volatility is yet another reminder that core bond returns, even U.S. Treasuries, are heavily impacted by interest rate duration. Collateralized loan obligations (“CLOs”) are generally not included in “agg”-type indices that most core bond managers benchmark to, and therefore allocations tend to be relatively small or non-existent. However, CLOs provide the attributes that investors look for in their core bond portfolios: attractive yield, safety, and diversification, and have continued to outperform core fixed income through this most recent volatility. As a result, an allocation to CLOs in a core bond portfolio has provided better outcomes year to date.

Source: J.P. Morgan and ICE Data Indices as of March 31, 2024. CLOs represented by J.P. Morgan CLO Index; AAA CLOs represented by the AAA subset of the J.P. Morgan CLO Index; Core Bonds represented by the ICE BofA US Broad Market Index.

In fact, CLOs have provided the best risk-adjusted returns versus other fixed income asset classes over the past decade, through various rate and credit cycles. CLO returns benefit from high yields and spreads versus similarly rated bonds, structural protections that have resulted in extremely low default risk, and rate insensitivity. More recently, strong technical and fundamentals have provided a tailwind to credit spreads. CLOs have outperformed core bonds as well as the broad high yield bond market this year.

For investors looking to add CLO exposure, we believe a broad investment grade exposure provides better opportunities versus one that is constrained to AAA CLOs. Today’s currently benign credit environment favors capturing higher carry outside of AAAs, while remaining cautious due to tighter valuations in CLOs rated BBB and below. The ability to take advantage of higher yields in lower-rated tranches also provides the opportunity to earn attractive absolute yield levels even in a declining environment. Looking forward, any weakening in the credit environment could create attractive total return opportunities for CLO tranche managers that can opportunistically add risk when value is pushed further into lower-rated tranches. Constraining a CLO investment strategy to only one rating category significantly reduces these opportunities.

An actively managed approach, in both top-down portfolio construction as well as rigorous bottom-up security selection, can add significant value in CLO investing. Right now such an approach, we believe, falls into a sweet spot of high carry with relative safety and stability – the attributes most investors look for in their core bond portfolio.

VanEck has partnered with PineBridge Investments on the VanEck CLO ETF (CLOI), which provides access to investment grade floating-rate CLOs. CLOI benefits from PineBridge’s decades of CLO market experience, both as a CLO manager and CLO tranche investor, and deep leveraged finance expertise.

Originally published 10 April 2024.

For more news, information, and analysis, visit the Beyond Basic Beta Channel.

Disclosures

ICE BofA U.S. Broad Market tracks the performance of U.S. dollar denominated investment grade debt publicly issued in the U.S. domestic market, including US Treasury, quasi-government, corporate, securitized and collateralized securities.

J.P. Morgan Collateralized Loan Obligation Index tracks U.S. dollar denominated broadly-syndicated, arbitrage CLOs.

This is not an offer to buy or sell, or a recommendation to buy or sell any of the securities, financial instruments or digital assets mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, tax advice, or any call to action. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results, are for illustrative purposes only, are valid as of the date of this communication, and are subject to change without notice. Actual future performance of any assets or industries mentioned are unknown. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. VanEck does not guarantee the accuracy of third party data. The information herein represents the opinion of the speaker(s), but not necessarily those of VanEck or its other employees.

The Fund’s benchmark is the JP Morgan CLOIE Index which is the first rules-based total return benchmark for broadly-syndicated, arbitrage US CLO debt. Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The Index is used with permission. The index may not be copied, used or distributed without J.P. Morgan’s written approval. © 2024, J.P. Morgan Chase & Co. All rights reserved. Index performance is not representative of Fund performance. It is not possible to invest directly in an index.

An investment in the VanEck CLO ETF (CLOI) may be subject to risks which include, but are not limited to, risks related to Collateralized Loan Obligations (CLO), debt securities, LIBOR Replacement, foreign currency, foreign securities, investment focus, newly-issued securities, extended settlement, affiliated fund investment, management and capital preservation, derivatives, cash transactions, market, Sub-Adviser, operational, authorized participant concentration, no guarantee of active trading market, trading issues, fund shares trading, premium/discount, liquidity of fund shares, non-diversified, and seed investor risks, all of which may adversely affect the Fund. Investments in debt securities may expose the Fund to other risks, such as risks related to liquidity, interest rate, floating rate obligations, credit, call, extension, high yield securities, income, valuation, privately-issued securities, covenant lite loans, default of the underlying asset and CLO manager risks, all of which may impact the Fund’s performance. Derivatives may involve certain costs and risks such as liquidity, interest rate, and the risk that a position could not be closed when most advantageous.

Investing involves substantial risk and high volatility, including possible loss of principal. An investor should consider the investment objective, risks, charges and expenses of the Funds carefully before investing. To obtain a prospectus and summary prospectus, which contain this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.

© Van Eck Securities Corporation, Distributor, a wholly owned subsidiary of Van Eck Associates Corporation.