By Natalia Gurushina

Chief Economist, Emerging Markets Fixed Income

Central banks in EM Europe now have to take into account the ECB’s liftoff. Brazil’s inflation gives some credence to the “Q2/Q3 peak inflation” thesis. China’s foreign trade was growth-positive at the margin.

ECB Liftoff and EM Europe

The European Central Bank (ECB) had spoken today, signaling a liftoff next month (+25bps now fully priced in), and potentially accelerating the pace of rate hikes to 50bps in September. The ECB also confirmed that its asset purchase program will end from July 1. Of course, many observers are asking why the ECB is tightening just as the economy is facing multiple (and multiplying) growth headwinds – one classic policy blunder (ECB’s 2011 rate hike) immediately comes to mind – but the ECB’s mandate is to target inflation, so here we are. The “no drama” liftoff should probably reassure central banks in emerging markets (EM) Europe that their decision to slow the pace of rate hikes was correct – note that Hungary made no change in its 1-week deposit rate today – but the bond market is getting antsy, with local rates under pressure across Central Europe.

Peak Inflation In LATAM?

“Peak inflation” is another important component of the global macro narrative. The consensus timing is Q2/Q3, and so today’s downside inflation surprise in Brazil drew a lot of attention. The surprise in question was tiny – 11.73% year-on-year vs. 11.88% – but it did show deceleration from 12.13% in April. Further, the diffusion index (which shows how widespread inflation pressures are) moderated as well. This definitely leaves room for the Brazilian central bank to slow the pace of rate hikes to 50bps next week. However, we (and the central bank) keep an eye on the fiscal “price tag” of lowering utility prices, which keeps grinding higher and can create.

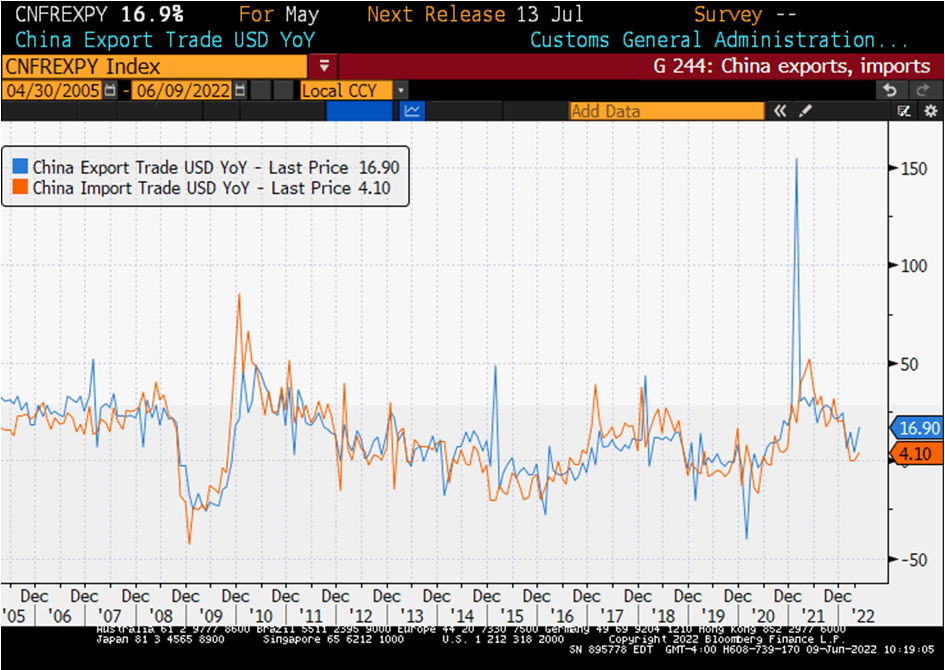

China Growth Expectations – Bottoming Out?

China’s growth outlook is an important component of any global “big picture” (as the only independent global growth driver in EM). And the latest foreign trade numbers looked growth-positive at the margin – pointing both to easing global supply chains (stronger than expected export growth) and improvements in domestic activity (some pickup in imports). Subsequent reports about the new lockdowns in Shanghai, however, raised some concerns about Chinese ports’ reopening and the continuation of exports’ rebound – the latter can also be affected by the impact of higher interest rates on GDP growth in China’s main trade partners. The next batch of China’s credit and monetary aggregates should provide more color on domestic growth headwinds/tailwinds – the consensus believes that May should show a major rebound. So, stay tuned!

Chart at a Glance: China Foreign Trade – Growth-Positive?

Source: Bloomberg LP

Originally published by VanEck on June 9, 2022.

For more news, information, and strategy, visit the Beyond Basic Beta Channel.

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan’s index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG – JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.