While aerospace and defense ETFs have recently caught investor interest, space ETFs have been quietly gaining traction. The space sector shares some overlap with the aerospace industry. But it remains a distinct segment with a large thematic appeal. Here’s what investors need to know about the space industry, how it differs from the broader aerospace and defense industry, and what the future holds for space.

Space ETFs: Early-stage industry with unique growth opportunities

Space ETFs gained significant attention in recent years, largely driven by the surge in private sector involvement in space exploration and tourism. Companies like Virgin Galactic (SPCE) and Rocket Lab (RKLB) were popular among retail investors following their launches as special purpose acquisition companies (SPACs). SPACs were viewed as a faster, more flexible alternative to traditional IPOs. They were typically used by high-risk, high-reward companies in emerging, disruptive technologies like space exploration (see my previous note here). Many of the companies that entered the market through SPACs have experienced significant volatility, and investor enthusiasm has diminished. Additionally, several high-profile companies in the space sector, including SpaceX, have remained private, limiting investor access. But recent investor attention to broader disruptive technology themes like artificial intelligence and robotics has rekindled interest in emerging space technologies.

In contrast, a larger but less visible segment of the space industry includes satellite manufacturing, satellite communications, and space-based imagery. Notable players in this space include Echostar Corp (SATS), which focuses on satellite services, ViaSat (VSAT), a provider of satellite broadband services, SiriusXM (SIRI), a satellite radio service, Iridium Communications (IRDM), which operates satellite communication services, and Garmin (GRMN), which provides GPS technology and satellite-based navigation systems.

The mix of innovation in space exploration and tourism along with the real-world application of satellite and imaging companies has intriguing appeal for investors. As measured by the space ETFs listed in the table below, the space segment is up in the ~20% range YTD compared to broader equities (the S&P 500 index), which is up only ~6% so far this year.

The space industry differs from the aerospace industry

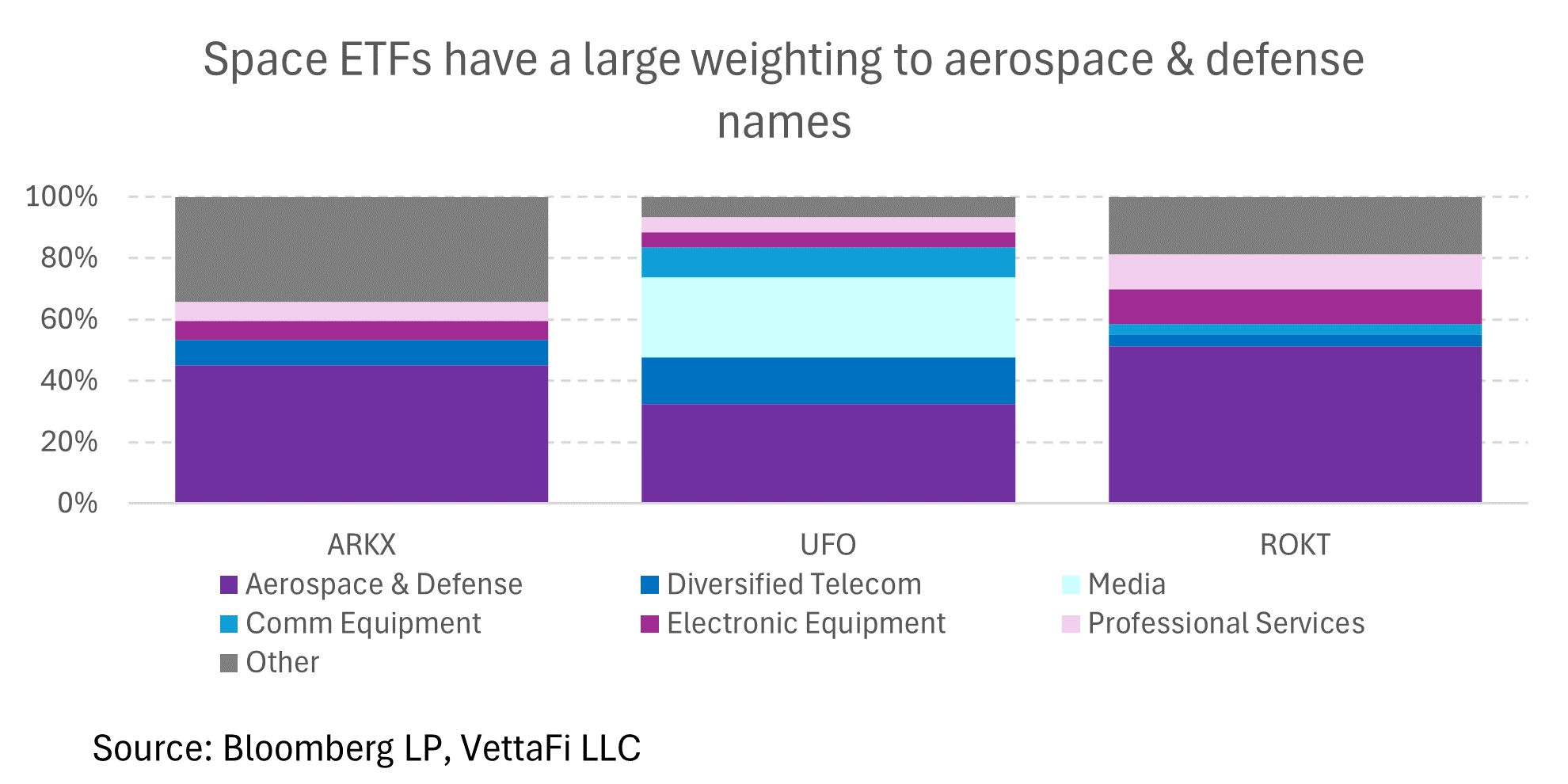

Although there is significant overlap between the aerospace and space industries, the two are distinct industries. The aerospace sector includes all companies involved in the design and production of aircraft and spacecraft, focusing both on air and space travel. In comparison, space focuses primarily on activities beyond Earth’s atmosphere, such as satellite deployment, space exploration, and space tourism. According to Procure, space begins at the Karman Line, located 62 miles above Earth’s surface. In terms of ETFs, the crossover between aerospace and space exposure is typically limited but still significant — less than 50% of a space ETF’s weight — which is an important consideration for investors seeking exposure to the more specialized space sector.

A few options exist for space ETFs although each has a distinct strategy:

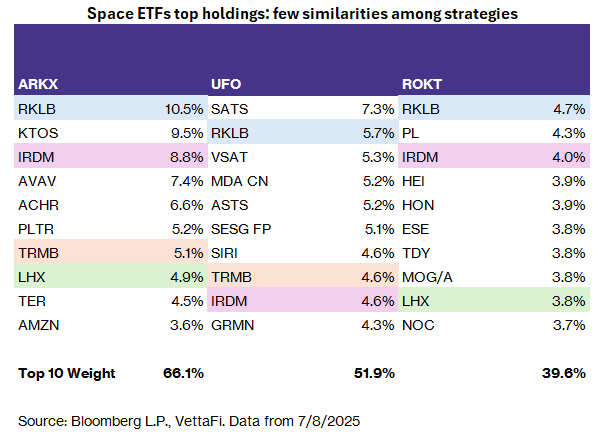

- ARK Space Exploration & Innovation ETF (ARKX): This active ETF targets companies driving innovation in space exploration and related technologies. These include autonomous mobility, intelligent devices, 3D printing, reusable rockets, and more. The ETF has around 10% weight each to Rocket Lab (RKLB) and Kratos Defense & Security (KTOS). But it also includes some more diversified holdings like Amazon (AMZN) and Alphabet Inc (GOOG). Interestingly, this ETF also holds passenger air mobility and eVTOL (electric vertical take-off and landing) companies like Joby Aviation (JOBY) and Blade Air Mobility (BLDE).

- Procure Space ETF (UFO): UFO invests in a range of companies involved in space technology, space-based imagery, satellite communications, and rocket manufacturing. With just over $80 million in assets, this ETF is smaller than ARKX. However, its holdings seem more directly space-related since ARKX includes some Magnificent Seven names. And unlike its peers, UFO contains a large allocation to the communication sector — companies that focus on the broader theme of connectivity in a global world. Its top holding, Echostar Corp (SATS), is a satellite communication company with recognizable subsidiaries like Boost Mobile, Dish Network, and Sling TV.

- SPDR S&P Kensho Final Frontiers ETF (ROKT): ROKT differs slightly from ARKX and UFO in that it also contains exposure to deep sea exploration in addition to space exploration. This means the ETF holds some unique companies like Oceaneering Intl (OII). The ETF, however, still contains more than 50% weight in aerospace and defense.

- Other ways to gain space exposure: While not a space ETF, the ERShares Private-Public Crossover ETF (XOVR) provides access to entrepreneurial U.S. companies and has a 9% allocation to SpaceX private security.

- Future launches: Tuttle has filed for the Tuttle Capital UFO Disclosure AI Powered ETF, which targets companies that potentially have exposure to alien technology as outlined by government disclosures about UFOs. These companies include aerospace and defense contractors, semiconductor/electronics companies, and companies specializing in detection/counter-UAP (unidentified anomalous phenomena) solutions.

Aerospace & defense ETFs: Stability with growth opportunities

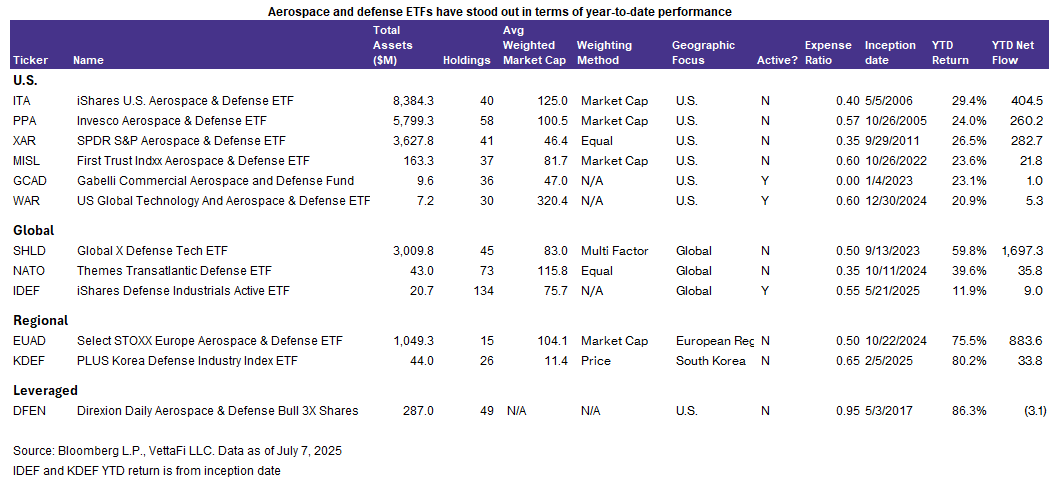

Broader aerospace and defense ETFs have continued to pick up steam in 2025 on top of geopolitical tension, technological advancements, increased international defense spending, and investor appetite for more stable yet high growth sectors. Aerospace and defense ETFs primarily focus on companies involved in the design, production, and service of aircraft, missiles, defense systems, and other military technologies. Some of the largest and most recognizable names in the U.S. aerospace & defense sector include General Electric (GE), RTX Corp (RTX), Boeing Company (BA), Lockheed Martin (LMT), and Northrup Grumman Corp (NOC).

These companies often receive more investor interest during times of geopolitical conflict due to increased demand in defense systems. What makes the industry attractive to many investors is that defense companies tend to be less cyclical due to their dependence on long-term sales contracts with the government. So far this year, the performance of aerospace & defense ETFs remains steady. That reflects continued government investment in military and defense technologies. Growth is even more apparent in global and European regions, as NATO countries play “catch-up” with defense spending to U.S. defense spending levels.

Some of the largest aerospace and defense ETFs include:

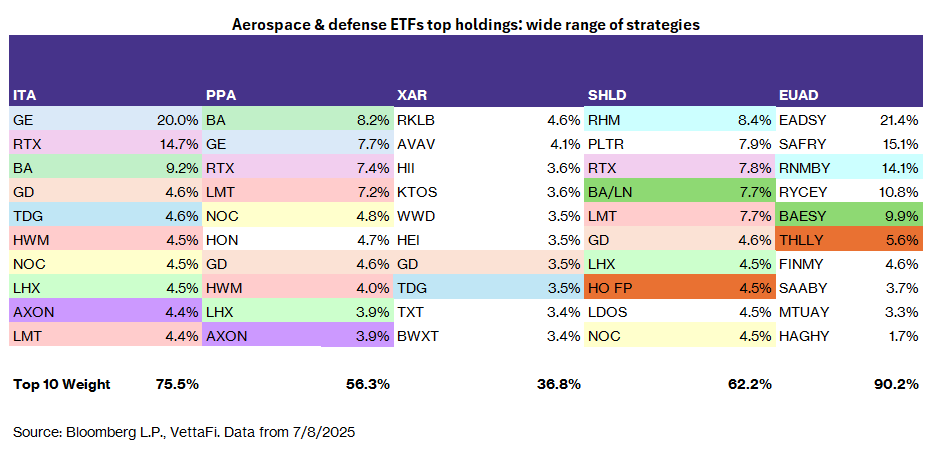

- iShares U.S. Aerospace & Defense ETF (ITA): This ETF is currently the largest aerospace and defense ETF, with over $6 billion in assets. ITA focuses on U.S. companies that manufacture commercial and military aircrafts and other defense equipment. The ETF uses a market cap weighting methodology, which results in a top-heavy portfolio. GE is currently 20% of weight, followed by RTX Corp at almost 15% weight, and Boeing at 9% weight.

- Invesco Aerospace & Defense Portfolio (PPA): This is the oldest ETF in the sector (but only six months older than ITA). It consists of companies involved in development, manufacturing, operations, and support of U.S. defense, homeland security, and aerospace operations. The index uses a proprietary weighting methodology called TrueCap. This reduces overweighting of diversified companies — in this case, GE; 20% of ITA is only around 8% of PPA.

- SPDR S&P Aerospace & Defense ETF (XAR): This is another ETF with a relatively straightforward selection process based on industry classification. Unlike its peers, XAR uses a modified equal-weight methodology. This methodology has offers greater exposure to small-cap components like Rocket Lab and Kratos Defense.

- Global X Defense Tech ETF (SHLD): Unlike its peers, SHLD does not include commercial aerospace exposure. The ETF focuses on pure-play defense technology, cybersecurity, and advanced military systems. While many of its top holdings are similar to other ETFs, SHLD has a larger exposure to Palantir Technologies (PLTR) — which was up 83% YTD. This ETF also has exposure to international names like Bae Systems (BA LN), Rheinmetall AG (RHM GR), and Thales SA (HO FP), while the above ETFs all focus on U.S. stocks.

- Select STOXX Europe Aerospace & Defense ETF (EUAD) is the only U.S.-listed ETF focused on the European defense sector. The ETF only contains 13 stocks of European companies that are listed as ADRs. These companies derive at least 50% of their revenues from civil and military defense efforts. The ETF has a heavy concentration to its top two holdings — Airbus (EADSY) and Safran (SAFRY). Together, those two make up 36% of the ETF’s weight.

- For additional details, see this research note on the broader defense industry and this research note on the European/global defense industry.

Bottom Line: Aerospace and defense ETFs offer a mix of stability and growth. They have seen stronger YTD returns relative to space ETFs. Space ETFs, however, remain an interesting niche with some overlaps with the aerospace and defense industry. While space ETFs come with higher volatility, they offer unique long-term growth potential in commercial space exploration and emerging technologies.

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for UFO, for which it receives an index licensing fee. However, UFO is not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of UFO.

For more news, information, and analysis, visit VettaFi | ETF Trends.