By Gary Stringer, Kim Escue and Chad Keller, Stringer Asset Management

Achieving financial independence during retirement is the most important and most difficult part of the financial planning process. Investors have one chance to get retirement right, so their retirement plan must be robust and able to withstand a wide range of potential outcomes.

We think there are two portfolio metrics that are often overlooked by investors but have a significant impact on the success of their investment journey. These metrics, salvageable and sustainable, can be used to help guide the transition from one allocation to the next. Salvageable considers a worst-case scenario and whether an investor has sufficient time to recover. Sustainable considers the income level that can be achieved without depleting the portfolio’s principal over the long-term.

While an investor cannot predict or prevent a market downturn and may need to take principal from their retirement portfolio from time to time, we think that considering both market drawdown and sustainable income as part of the planning process can help investors determine the appropriate allocations and acceptable levels of risk in their investment plan.

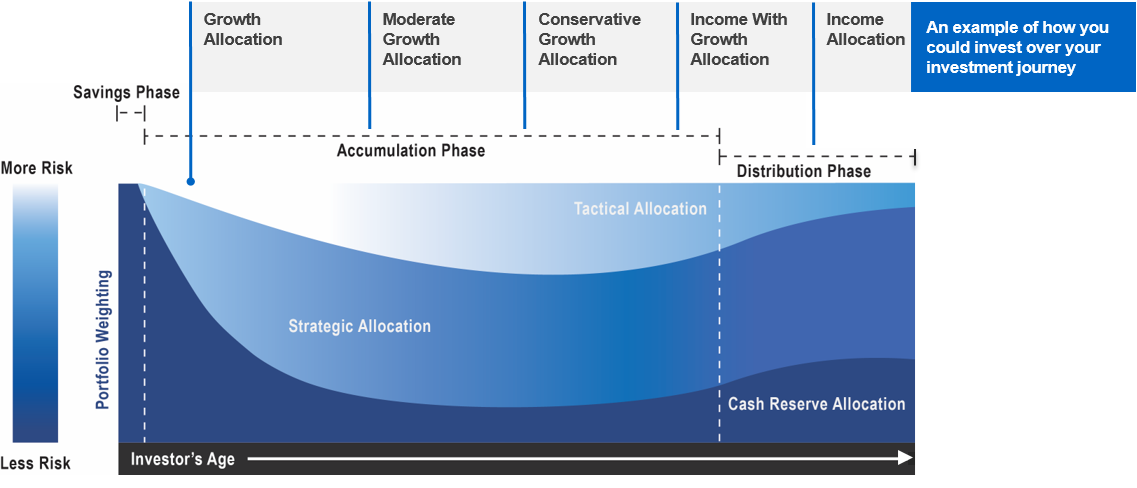

![]() As an investor’s goals and time horizon change, so should their investment mix. For example, an investor’s tolerance for market risk decreases as their need to draw consistent income increases. We refer to this concept as the investment journey and we like to represent the retirement goal as three different phases on the journey: early accumulation, late accumulation, and the distribution phase.

As an investor’s goals and time horizon change, so should their investment mix. For example, an investor’s tolerance for market risk decreases as their need to draw consistent income increases. We refer to this concept as the investment journey and we like to represent the retirement goal as three different phases on the journey: early accumulation, late accumulation, and the distribution phase.

In general, the accumulation phase is the first phase where the investor starts to build an investment portfolio and emergency cash account. The investor can aggressively allocate within their investment portfolio during the early stages of the accumulation phase, which lasts until they have around 15 years until retirement. During this phase, an investor can afford to take more risk within their portfolio with the expectation they may achieve higher rates of return since they have ample time to recover from any major market declines.

Once the investor is within about 15 years of retirement, they are still accumulating assets and growing their portfolio, but may begin to reduce risk exposures as the date of their first distribution nears. In this part of the late accumulation phase, the investor is still primarily focused on asset growth, but the need for risk management is increasing as the ability to recover from a significant market decline is limited due to the reduced time horizon until their first distribution. The final period is the distribution phase, during which an investor is taking money from their investment portfolio to help fund their retirement.

As simple as this seems, the difficult part is moving from one asset allocation to the next during the journey in an efficient and fluid manner. We think there are two portfolio metrics that are often overlooked by investors but have a significant impact on the success of their investment journey. These metrics, salvageable and sustainable, can be used to help guide the transition from one allocation to the next.

SALVAGEABLE

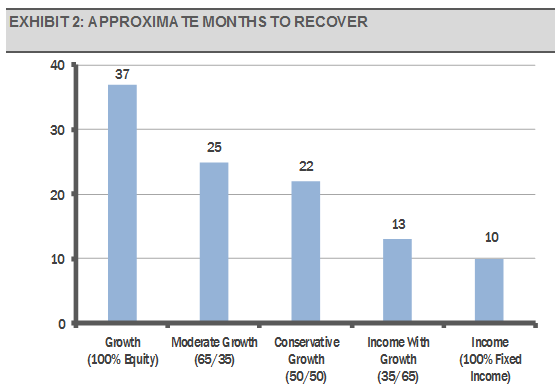

The first metric is the worst-case scenario, or how much money is at risk. Essentially, we are looking to see if an investment goal is still salvageable if a maximum loss occurs. Importantly, while these loss numbers are historically accurate, what happens in an actual portfolio maybe even worse. Using blends of the S&P 500 Index and Bloomberg Barclays U.S. Aggregate Bond Index, we have found that over the past 25-years, the following figures represent the largest drawdown and the approximate time it took the market to recover to its previous level. As you will see, while equity investing has generated significant long-term returns, it entails taking substantial risk. Equity market risks can be mitigated by including other asset classes, such as high-quality bonds, in the investment mix.

![]()

Source: Bloomberg and Stringer Asset Management The results in Exhibits 1 and 2 are based on index blends using the S&P 500 Total Return Index to represent equities and the Bloomberg Barclays U.S. Aggregate Bond Index to represent fixed income in their stated blends. Past performance is not a guarantee of future results. The performance represented uses daily rebalancing of the index blends using total returns series that include the reinvestment of dividends and other earnings. The indices represented do not bear transaction costs or management fees. To the extent a shareholder pays sales charges, advisory fees, brokerage commissions and other expenses, the performance shown would be less. All indices are unmanaged and investors cannot invest directly in an index. This material is for informational purpose only and has not been verified or audited by an independent accountant. For index definitions, see the Index Definitions section at the end of this document.

We think an investor should work backwards from the date of their first retirement distribution in an attempt to ensure there remains enough time to recover from a significant negative return from the more aggressive allocations. For example, investors in a Growth allocation probably want to have at least 15 years before the date of their first distribution in order to reduce the risk of not having enough time to recover from a significant equity market decline. We refer to this period as the early accumulation phase. Once an investor is within a 15 to 10-year window, or in the late accumulation phase, they might consider toning down equity market risk by moving to a Moderate Growth or Conservative Growth allocation to further reduce the risk of substantial loss near their retirement. Finally, when an investor is roughly 10-years from needing retirement income all the way through their retirement, or distribution phase, they should likely consider Conservative Growth, Income with Growth, and Income allocations to help reduce the risk of significant loss near and during the distribution phase.