While concentration has overall increased over the past few months, some sectors have seen more dramatic changes than others. Many investors opt for an equal-weight strategy when getting sector exposure to reduce concentration risk in portfolios. By weighting each constituent company equally, a small group of companies is not able to have an outsized impact on the index.

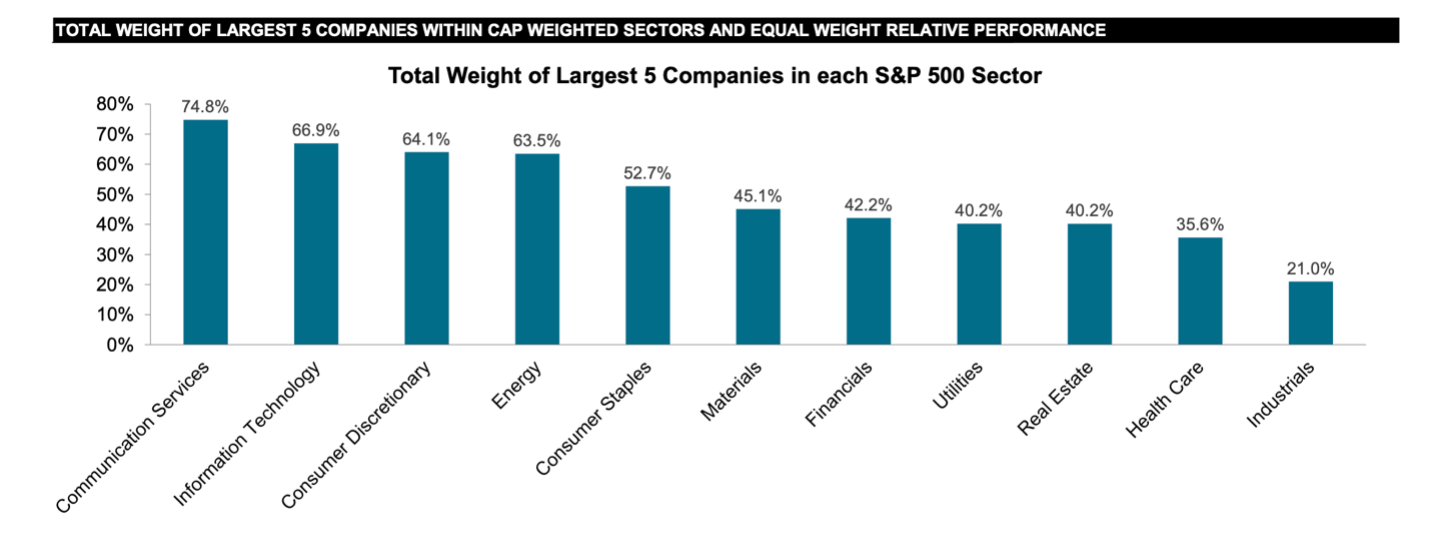

The five sectors with the greatest total weight of the largest five companies include communication services, information technology, consumer discretionary, energy, and consumer staples, as of June 30. Conversely, the sectors with the lowest concentration in the largest five names are industrials, healthcare, and real estate, according to S&P Dow Jones Indices.

Over the past two months, the biggest changes in concentration happened in the consumer discretionary and communication services sectors.

The weight of the largest five companies within the consumer discretionary sector has grown by over 4% between April 30 and June 30. Meanwhile, the top five names in the communication services and consumer staples sectors gained 2.1% and 1.5%, respectively. The top names in the information technology sector gained 0.7%.

See more: “Tech Sector Concentration Reaches Historical High”

Conversely, the weight of the top five companies in the industrials and energy sectors declined by 1%. Meanwhile, the weight of the top names in real estate and utilities each declined by 0.2%.

Get Balanced Exposure With Equal-Weight Sector ETFs

Investors can use equal-weight strategies for more balanced exposure to sectors with the highest concentration risk. These strategies include the Invesco S&P 500 Equal Weight Communication Services ETF (RSPC), the Invesco S&P 500 Equal Weight Technology ETF (RSPT), and the Invesco S&P 500 Equal Weight Consumer Discretionary ETF (RSPD).

The simple arithmetic of rebalancing connects equal-weight strategies to anti-momentum effects. If the price of a constituent increases by more than the average of its peers, its weight will increase. Therefore, the position will be trimmed at the next rebalance as the portfolio returns to equal weights.

Conversely, if a stock falls by more than the average of its peers, its weighting will fall too. The index will add more weight to the security at the next rebalance. Thus, equal-weight indexes sell relative winners and purchase relative losers at each rebalance, adding a value tilt to portfolios.

For more news, information, and analysis, visit the Portfolio Strategies Channel.