By Mike Clark, Consulting Actuary, the Principal Financial Group

Much of my role as an actuarial blogger is explaining the behavior of numbers through words, but it takes a lot of words to explain numerical behavior sometimes which leads unfortunately to acronyms.

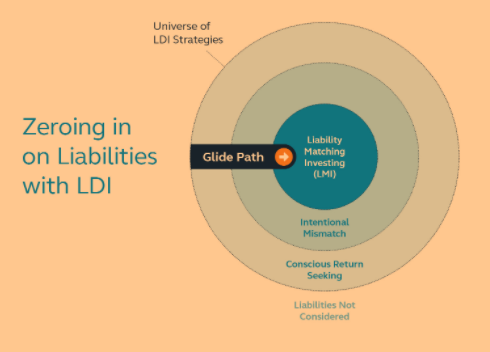

One of the most significant acronyms used in managing pension risk is “LDI” for “liability driven investing”. LDI is often described as using long duration bonds to reduce the risk of defined benefit (DB) plans. I have no objection to this definition (I use it myself frequently in the blog) as long as we all recognize it is an oversimplification.

Literally reading the words behind LDI indicates investments are merely driven by liabilities’ reaction to bond rates, but matching duration is not explicitly mentioned. This suggests LDI strategies need only take liability behavior into account, which is quite different from immediately matching asset and liability durations.

Yeah! Another Acronym!

As a public service to correct this semantical confusion, I would like to formally propose a new acronym: “LMI” for “liability matching investing”. LMI is what many people believe LDI to be, that is the maximum hedging of a pension liability with bonds of matching duration and quality.

The distinction between LMI and LDI is important these days, because the misunderstanding is interfering with fiduciaries’ implementation of sound risk management strategies. I often hear sponsors and advisors make comments like, “We’re not ready to do LDI now because bond rates and our funding ratio are too low.”

Unfortunately, this is a letter off. What they mean is that they don’t want to implement LMI (catching on yet?) because it essentially locks in their underfunded position and forfeits potential benefits if rates rise in the future. I fully understand the sentiment.

However, the literal meaning of the “not ready” statement is that investment decisions should not even take liability volatility into account, a comment no fiduciary this side of Y2K should ever make. The only investment strategy that is not LDI from a literal viewpoint is total ignorance of plan liabilities, which I’m sure isn’t what the speaker intended.

Everyone Needs LDI

So while not everyone is ready to implement LMI today, all pension sponsors need LDI in some form. Funding and economic circumstances may vary widely across plans and sponsors, but each one should weigh their need and ability to take investment risk in the context of the liabilities of their plans.

Whether it’s understood or not, the conscious decision to not match duration is still driven by the liabilities and qualifies as LDI. A glide path increasing duration matching as funding ratios improve and/or interest rates rise is also driven by liabilities and counts as LDI. Actually hedging risk by matching duration immediately is both LMI and LDI (since it is both matched and driven by liabilities.)

So LMI and LDI are related, but different. (All LMI is LDI, but not all LDI is LMI.) Understanding this difference is an important first step to building an effective risk management strategy, and helping decision makers understand when and if a move to LMI is appropriate.

So please join me in welcoming LMI to the crowded field of pension acronyms! Hopefully the benefits of making the distinction outweigh adding one more to the list.

Mike Clark is a fellow of the Society of Actuaries (SOA) and a member of the American Academy of Actuaries (AAA), though he was still taking exams during the pre-Y2K total return era.

Originally published by Principal, 11/23/20

The subject matter in this communication is educational only and provided with the understanding that Principal® is not rendering legal, accounting, investment advice or tax advice. You should consult with appropriate counsel or other professionals on all matters pertaining to legal, tax, investment or accounting obligations and requirements.

Insurance products and plan administrative services are provided by Principal Life Insurance Company, a member of the Principal Financial Group® (Principal®), Des Moines, IA 50392.

1411957-112020