Last year proved tumultuous for markets and advisors, and money markets and cash alternative strategies proved enormously popular. Given the number of risk factors investors continue to navigate this year, short-duration bonds still hold strong appeal.

The NEOS Enhanced Income Cash Alternative ETF (CSHI) is not to be missed. CSHI recently underwent a name change and is now the NEOS Enhanced Income 1-3 Month T-Bill ETF (CSHI). CSHI launched in August 2022 and enjoyed a banner year for flows in 2023.

Market and investor uncertainty remained prominent for most of 2023 as the Fed continued aggressive interest rate hikes for much of the year. Alongside rate risk were ongoing and new geopolitical risk, recession risk, and several other factors that played into investor trepidation.

In such a volatile and rising rate environment, short-duration bonds proved enormously popular. CSHI brought in nearly $260 million in net flows last year and proved a popular cash alternatives ETF for investors. What’s more, the fund continues to see steady inflows in an environment where many investors are flooding back into longer-duration bonds. Since January 1, the fund has net flows of approximately $25 million.

CSHI a Strong Income Play in Uncertain Markets

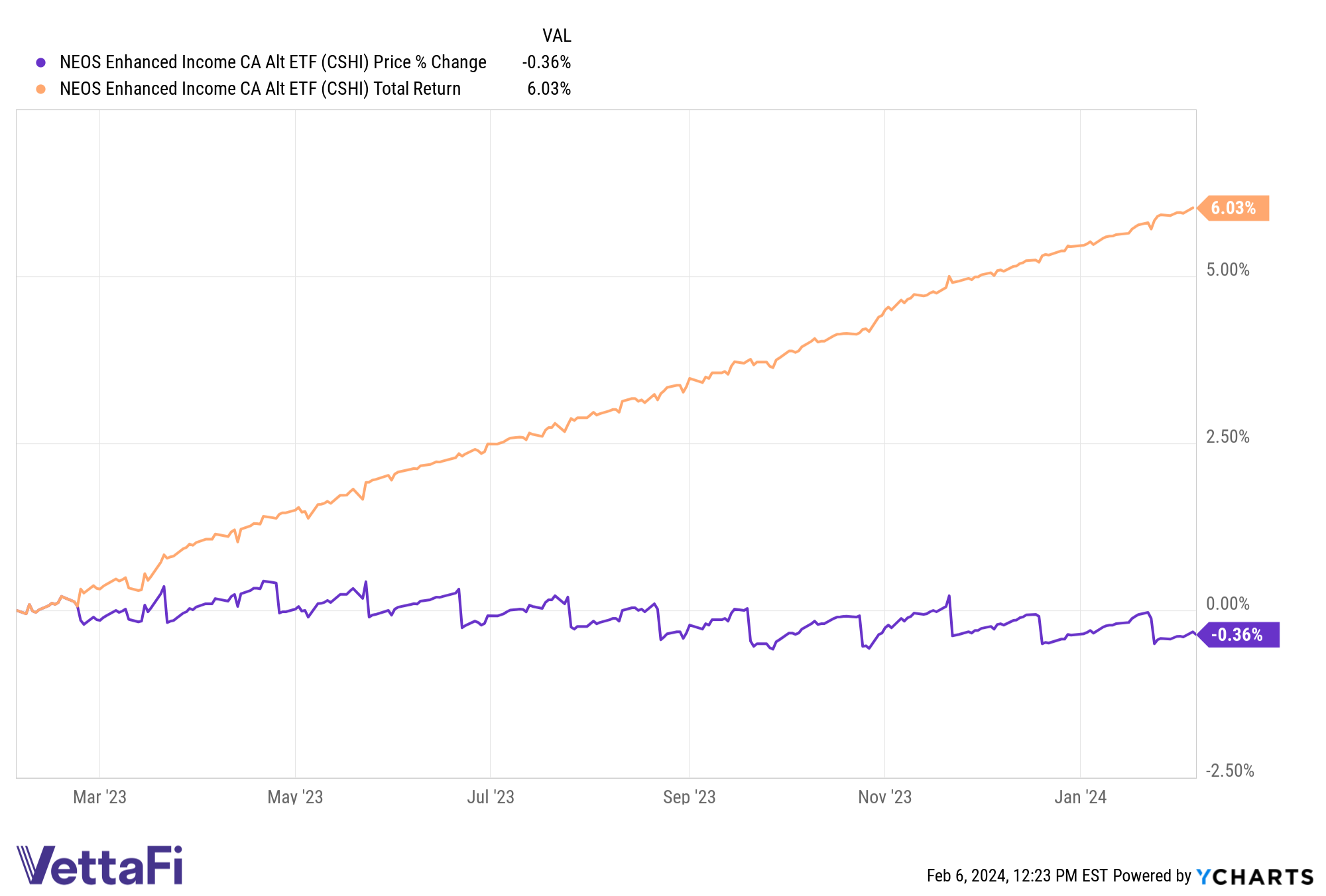

The NEOS Enhanced Income 1-3 Month T-Bill ETF (CSHI) seeks to deliver 100-150 basis points above what 1-3 month Treasuries are yielding. It’s noteworthy for its tax efficiency and monthly income-oriented strategy.

CSHI is an actively managed ETF that generates high monthly income and is options-based. It is long on three-month Treasuries and sells out-of-the-money SPX Index put spreads. These roll weekly to account for market changes and volatility.

The fund also seeks to take advantage of tax-loss harvesting opportunities and the tax efficiency of index options. CSHI currently has a distribution yield of 6.03% and a 30-day SEC yield of 5.05% as of 01/31/2024.

The put options that the fund uses are not ETF options but instead are S&P 500 index options. These options receive favorable tax treatment as Section 1256 Contracts under IRS rules. This means the options held at the end of the year are treated as if sold on the last market day of the year at fair market value.

Any capital gains or losses are taxed as 60% long-term and 40% short-term. Notably, this tax treatment applies regardless of how long the options were held. This can offer noteworthy tax advantages, and the fund’s managers also may engage in tax-loss harvesting opportunities throughout the year on the put options.

CSHI has an expense ratio of 0.38%.

For more news, information, and analysis visit the Tax-Efficient Income Channel.