By Bradley Krom, Head of U.S. Research

Over the last 11 weeks, nearly every major foreign currency (FX) has declined against the U.S. dollar. For many investors, the key question we sought to answer in an earlier piece was will the trend in dollar appreciation continue or is now the time to bet on a weaker dollar going forward. But for globally allocated investors, there is no neutral. Investing abroad involves currency risk—and we suggest strategies for understanding and managing those risks below.

The primary reason we say there is no neutral is because of the benchmarks that most investors choose. As perhaps an accident of history, many U.S. investors benchmark their returns against the MSCI All Country World Index, unhedged.

This decision means that in addition to comparing performance against global equity markets, returns are also impacted by movements in the U.S. dollar. Year-to-date, this decision has basically been a wash, but most allocators think longer term when making strategic asset allocation decisions. In an ideal world, currency risk and foreign equity risk would be managed independently. Unfortunately, in the U.S., the rise of currency-hedged ETFs didn’t really take hold until 2014. However, this means that investors need to be cognizant of these implicit bets going forward.

Cumulative FX Impact

Developed Markets

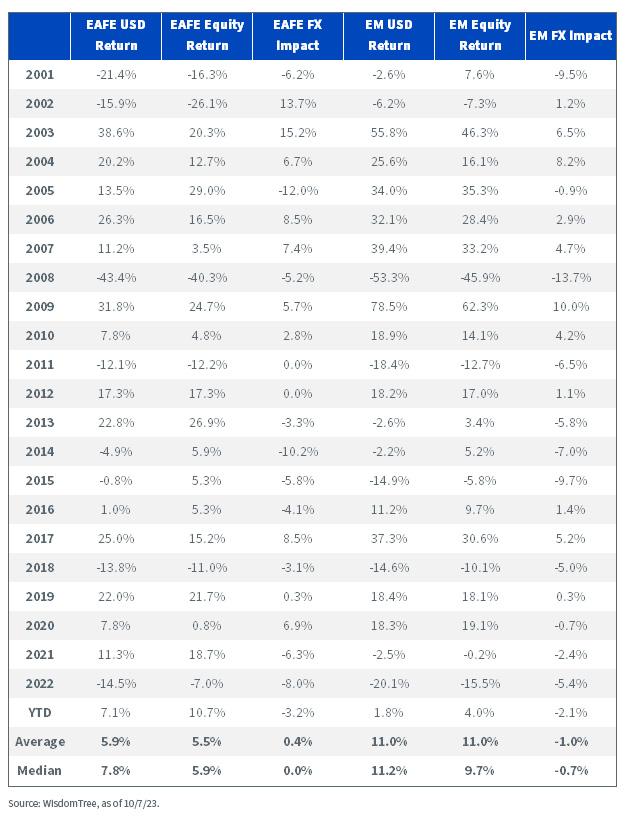

Since the early 2000s, FX has only contributed a negligible amount to developed international total returns. But this also misses the important point that up until 2010, FX had contributed 38.5% to total returns. Investors that initiated positions in developed international at that time have seen nearly 27% of their investment evaporate due to erosion from a stronger dollar.

Emerging Markets

In emerging markets (EM), the pain trade has been even more acute, falling by over 24% in the last 20+ years. From the peak in 2010, investors are down 31.8%. While currency-hedged ETFs do exist in emerging markets, we’re generally not a proponent of currency hedging on a strategic basis due to the significant costs associated with executing the hedge. The primary cost of hedging is driven by interest rate differentials. Since many emerging markets have structurally higher rates than the U.S., these costs can be significant over the total holding period. In most instances, if an investor has a positive outlook for the dollar versus emerging markets, they should perhaps rethink their bullish view for EM equities.

Digging Deeper into Calendar Year Returns

Developed Markets

Over market cycles for the last two decades, developed market currencies have experienced a lot of volatility, but no strong long-term return. Over time, currencies tend to cycle from over- to fair- to undervalued and back again, depending on differences in the outlook for growth, inflation and capital flows. This is broadly reflected when looking at calendar year returns hovering around zero over the last 22 years. But a few things are striking.

The primary driver of total returns is equity risk, but with the exception of 2002, investors would have significantly reduced their drawdowns during the worst periods of performance by currency hedging. In the best years for performance, with the exception of 2013, equities and currencies appreciated together. When investors align their views on equities and FX, they can increase not only their frequency of positive outcomes, but also magnify their gains. During years of mediocre returns, FX tends to act as a drag.

Investors benefitted by being underweight developed markets relative to the U.S. over the last 10 years. With the exception of 2017, investors could have enhanced total returns by currency hedging. While we know why investors get compensated to earn a risk premium for owning stocks, we are less confident there is a risk premium to be earned by being long foreign currencies all the time. Being hedged can help reduce volatility for international investments.

Emerging Markets

In emerging markets, currencies tend to trade at discounts to their long-term expected value (as measured by purchasing power parity , or PPP). However, as we’ve seen over the last 20 years, EM currencies can continue to trade at even higher discounts to long-term fair value, which erodes returns. In our view, if investors are concerned about another leg higher in the dollar impacting their international investments, hedging a portion of that exposure could make sense.

While equity risk also tends to be the primary driver of total returns in EM, in only one instance (2013) did EM FX depreciate during a strong year for emerging markets. It’s possible that 2023 could end the year in this situation, but it has been rare. More commonly, FX tends to be magnify returns in both directions.

What’s perhaps most striking is that despite a higher frequency and magnitude of negative total returns in FX, EM equities delivered total returns nearly double that of developed markets over the period, on average. This can largely be explained by the outsized gains in China, whose currency has been comparatively stable against other markets. However, as China is now the largest weight in EM benchmarks, it may be possible to conclude that allocations to EM are more about finding attractive stocks than owning significantly undervalued currencies.

Due to the high cost of carry in emerging markets, we have only implemented hedging using a multifactor process that dynamically hedges currencies. As my colleague pointed out, that model was approximately 90% hedged in October due to the strength of the dollar. But these hedge ratios will adjust over time as the momentum returns. Notably, this multifactor strategy had considerably lower volatility than standard EM funds due to the high volatility of the currencies.

Originally published 20 October 2023.

For more news, information, and analysis, visit the Modern Alpha Channel.