This is the first blog post of a three-part series on the effect of COVID-19 on the November 3rd election.

With more than 200,000 recorded U.S. COVID-19-related deaths, add in another plot twist: last night we learned that Donald and Melania Trump both contracted it.

As if Ruth Bader Ginsburg’s Supreme Court vacancy wasn’t enough drama.

As I write, the early indications are that Trump has a sniffle, some cold-like symptoms, fatigue. At 74, he finds himself in that vulnerable age group that could have him still fighting this thing – or worse – as the election approaches. You may recall that earlier this year Britain’s Boris Johnson also caught it, but he’s 18 years younger than Trump. Another notable global leader, the “Tropical Trump,” Brazil’s Jair Bolsonaro, caught Covid-19 and got over it this summer. He is 65 years old.

In a country where everything is political, our response to COVID-19 split down party lines months ago. The face of the lockdown camp is Democrat Andrew Cuomo, governor of New York. Advocating for reopening on the other side is Ron DeSantis, Florida’s Republican governor. At the federal level, the same concept: Cuomo’s reputation correlates with Joe Biden’s, while DeSantis is the state-level proxy for Donald Trump.

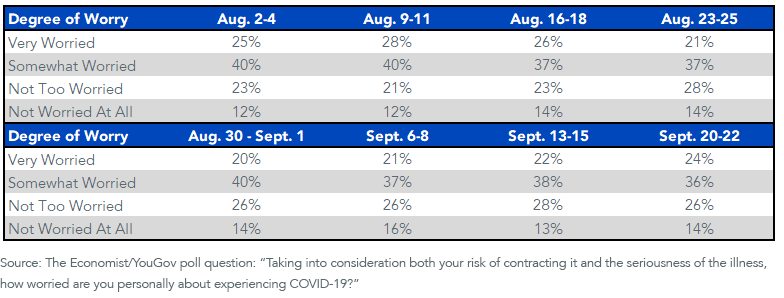

Here’s a question from the Economist/YouGov poll:

“Taking into consideration both your risk of contracting it and the seriousness of the illness, how worried are you personally about experiencing COVID-19?”

Note the wording of the question. It isn’t about your concern that you could catch it and pass it to an elderly relative. It’s about your personal health.

I have wrongly believed for months that the falling trend in hospitalizations would raise the ranks of the “Not Worried at All” respondents.

That has not happened (figure 1). Now, with Trump’s positive COVID-19 test splashed across the headlines, you have to wonder if social media’s “risk assessment via anecdote” issue will shift public sentiment. If Trump deteriorates, societal fear levels about the severity of the virus will spike. On the other side, the more likely outcome, even for a 74-year-old, is that he experiences cold symptoms and is back firing a couple weeks from now. In that circumstance, do more people have the conversation about Trump’s COVID-19 from the comfort of a restaurant booth?

Figure 1: “Worried About COVID-19”

Nevertheless, with 60% of respondents still either “Very Worried” or “Somewhat Worried” about their personal susceptibility to COVID-19, Trump has a reelection problem. If your thesis has the incumbent losing, check out my Biden blog.

For now, let’s game the other thesis: The COVID-19 situation improves between now and the election, pushing Trump to victory, an outcome that has slipped toward 2-1 odds at this point.

Do I have these market reactions about right?

Biden “On” and Trump “Off” = Alternative Energy

Trump “On” and Biden “Off” = Big Oil

And this?

Biden “On” and Trump “Off” = Regulate Wall Street

Trump “On” and Biden “Off” = Do Not Regulate Wall Street

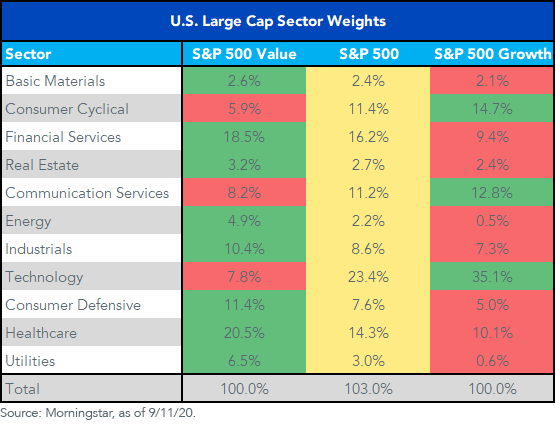

Look at the weights of Energy and Financials in the S&P 500 Value and S&P 500 Growth Indexes (figure 2). Form an opinion on the election outcome and you have your guide on growth versus value.

Trump win? Value. Biden win? Growth.

Figure 2: U.S. Large-Cap Sector Weights

For the Biden thesis—growth stocks—two strategies are the WisdomTree Cloud Computing Fund (WCLD) and the WisdomTree Growth Leaders Fund (PLAT). The latter can be thought of as our twist on the NASDAQ.

For the Trump thesis—value stocks—the WisdomTree U.S. LargeCap Dividend Fund (DLN) comes to mind because it has about 7% in the Energy sector. Another idea may be to shade down the market-cap spectrum. You can find a 22% weight to Financials inside the WisdomTree MidCap Dividend Fund (DON).

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Funds focusing their investments on certain sectors, such as DLN and DON, increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility.

Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty; these risks may be enhanced in emerging, offshore or frontier markets. Technology platform companies have significant exposure to consumers and businesses, and a failure to attract and retain a substantial number of such users to a company’s products, services, content or technology could adversely affect operating results. Technological changes could require substantial expenditures by a technology platform company to modify or adapt its products, services, content or infrastructure. Technology platform companies typically face intense competition, and the development of new products is a complex and uncertain process. Concerns regarding a company’s products or services that may compromise the privacy of users, or other cybersecurity concerns, even if unfounded, could damage a company’s reputation and adversely affect operating results. Many technology platform companies currently operate under less regulatory scrutiny but there is significant risk that costs associated with regulatory oversight could increase in the future. PLAT invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

WCLD invests in cloud computing companies, which are heavily dependent on the Internet and utilizing a distributed network of servers over the Internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the Internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.