By Behnood Noei, CFA

Director, Fixed Income

In 2023, a dominant theme for markets was the return of income in fixed income. Fast-forward to 2024, and despite a significant rally in spreads and a fall in yields during the fourth quarter, we believe this theme is still alive and well. As a matter of fact, yields of U.S. high-yield and investment-grade corporates still rest in the top quintile and decile of levels experienced over the last 10 years.

However, one segment of the market that has gone under the radar has been emerging markets debt, specifically emerging market corporates. In this piece, we will look at this sector and examine the case for including emerging market corporates’ debt in investors’ portfolios relative to U.S. corporate bonds and the dollar-denominated debt of emerging market sovereigns.

Attractive Yield Potential

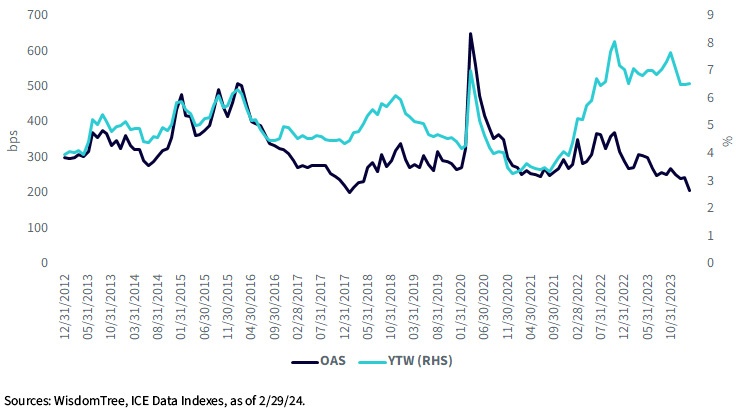

Even after a significant rally of 444 basis points (bps) in spreads from the highs during COVID-19 (653 bps in March 2020), emerging market corporates continue to offer an attractive all-in yield. In fact, the all-in yield of 6.58% at the end of February stands in the top 10th percentile of yield offered by the sector in the past 10 years.

Emerging Market Corporates

For definitions of terms in the chart above, please visit the glossary.

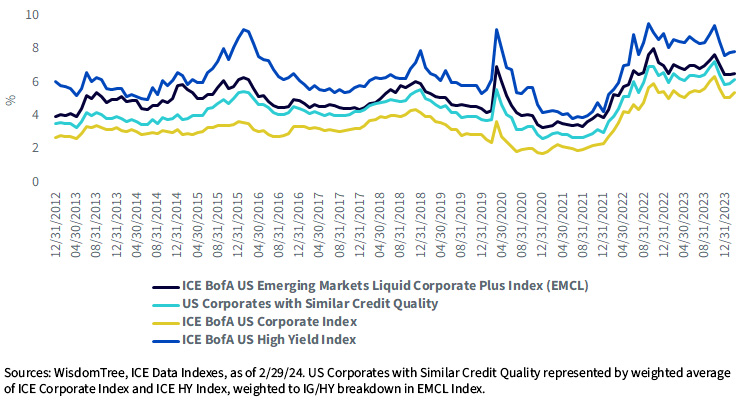

Emerging market corporates not only offer a higher yield compared to what they have offered in the past but also compared to a portfolio of their U.S. counterparts with similar credit ratings (represented by the weighted average of the ICE corporate index and ICE HY index, weighted to the investment-grade/high-yield breakdown in the EMCL Index) (69% investment-grade and 31% high-yield as of February 29, 2024), they have consistently provided investors with higher income.

YTW

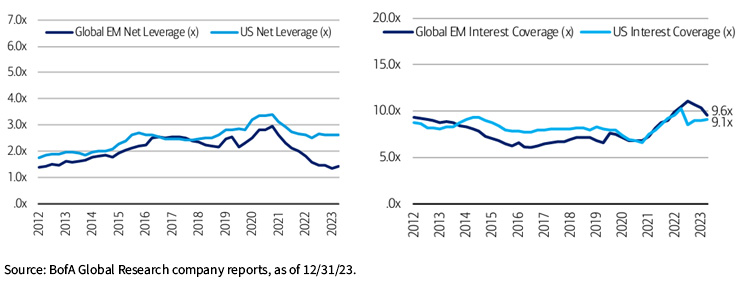

Strong Fundamentals

One of the biggest concerns with emerging market securities, specifically corporates, and the main reason they have consistently offered higher income compared to a portfolio of U.S. corporates with a similar credit rating mixture, is their fundamentals. However, by looking under the hood, one can see emerging market corporates have improved their fundamentals. The gross and net leverage in EM corporates are some of the lowest in the past decade and also lower relative to U.S. corporates. The same can be said about their interest coverage ratio. Even though their IC has fallen recently, they still fare better than U.S. corporates.

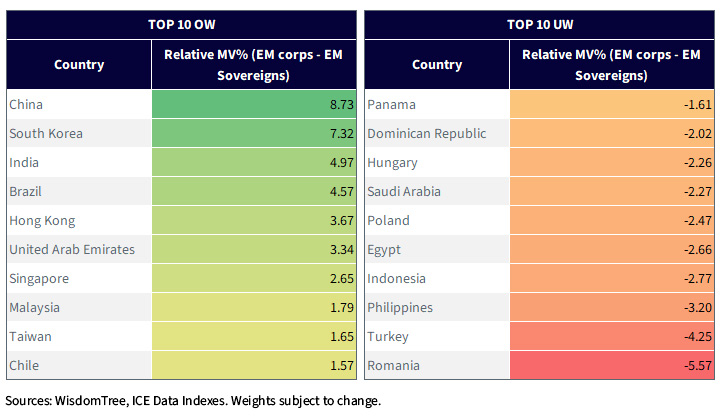

Better Credit Quality and Less Interest Rate Risk Than EM USD Sovereigns

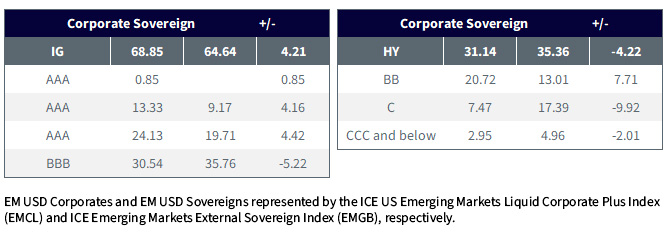

Another frequently used jibe at emerging market corporates is if an investor wants to invest in emerging markets, they can invest in “higher quality, less risky” sovereigns. However, this is another misnomer about emerging market corporates issuing in USD. The USD-Denominated Emerging Market Corporate Index has a higher allocation to investment-grade issuers than to USD-denominated EM sovereigns.

Credit Quality of ICE Emerging Market Debt Indexes – USD Corporate vs. USD Sovereign

Looking at the country of risk of the issuers in these two indexes, the EM Corporate Index has a much higher allocation to countries with better fundamentals and a lower allocation to countries with struggling economic conditions. In many cases, the governments of the more developed emerging market countries secure most of their financing through debt denominated in their own currency.

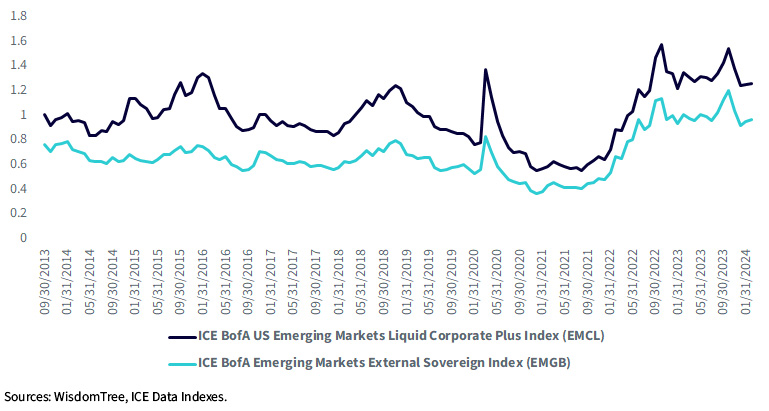

Finally, many emerging market corporations largely issue intermediate maturity debt, while EM sovereigns issue further out the curve, resulting in a consistently sharp duration difference between the two universes. (Currently, the universe for EM corporates has an average duration of 5.21 versus 6.98 for the universe of EM USD sovereigns.) Despite the duration difference, the aggregate yield sacrifice offered by EM corporates to EM is relatively modest, averaging about 27 bps over the last 10 years. Consequently, EM corporate portfolios have a significantly higher potential yield, given the amount of interest rate risk or yield per unit of duration, than EM USD sovereigns, as defined by their broad benchmarks.

Yield Per Unit of Duration

Selection Is the Key

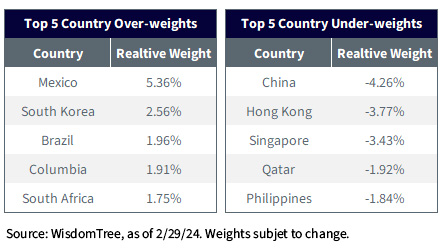

As mentioned before, EM corporate fundamentals remain resilient, and financial policy remains prudent. As such, the default rate is expected to be lower as well. However, like any other segment of the market, investors need to be selective and choose issuers/regions that have better fundamentals. And that’s the approach that the management team of the WisdomTree Emerging Market Corporate Bond Fund (EMCB) takes. EMCB is positioned with an over-weight (relative to the JPMorgan CEMBI Diversified Index) to Latin America and an under-weight to Africa and select countries in Asia, most notably China. China’s strengthened policy response appears to have stabilized activity; however, growth is likely to slow further this year as housing and private sector confidence remain negative.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Derivative investments can be volatile, and these investments may be less liquid than other securities and more sensitive to the effects of varied economic conditions.

Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. In addition, when interest rates fall, income may decline. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Unlike typical exchange-traded funds, there is no index that the Fund attempts to track or replicate. Thus, the ability of the Fund to achieve its objective will depend on the effectiveness of the portfolio manager. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.