By Jeff Weniger, CFA, Head of Equity Strategy

Key Takeaways

- South Korea’s classification as an “emerging” or “developed” market affects funds’ allocations, with some emerging markets funds having no exposure to the country.

- The “Korea Discount” refers to the low valuations placed on South Korea’s stocks relative to stocks in other countries. Korea’s officials aim to narrow this discount through corporate governance reform.

- The “Name and Shame” initiative in Japan, which increased the price-to-book ratio of Japanese companies, is being watched by Korea’s Financial Services Commission as a potential model for reform.

- The Chaebol system in Korea, which consists of family-run companies with controlling stakes in conglomerates, may be reformed through the “Corporate Value-Up Program,” potentially leading to higher stock prices.

South Korea is a peculiar country for asset allocators because our industry is torn over the question of whether the world’s 13th-largest economy is an “emerging” or “developed” market. It can be a difference-maker because some emerging markets funds may have a double-digit weight in the country while others have no allocation at all (figure 1). For example, the Vanguard Emerging Markets Stock Index Fund (VWO) has no exposure to Korea because its index provider, FTSE, puts the country in the developed category. The five non-WisdomTree Funds listed in figure 1 are all major ones with large asset bases.

Figure 1: South Korea Weight, Emerging Markets

WisdomTree’s emerging markets investors could find themselves in an alpha generation situation if Korea’s leadership pulls off a key goal this year: narrowing its stock market’s so-called “Korea Discount” by following Japan’s lead on corporate governance reform.

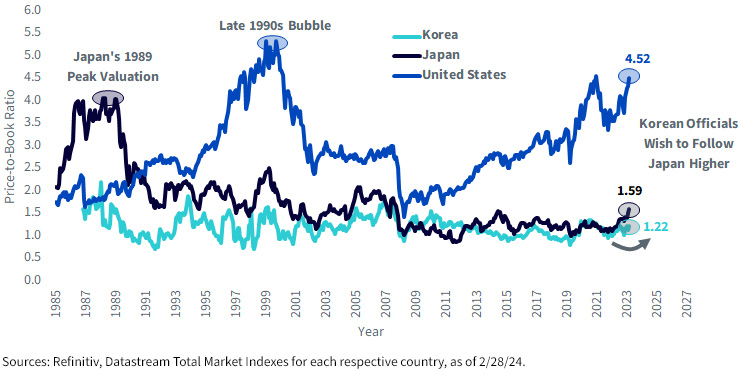

The Korea Discount refers to the low valuations placed on South Korea’s stocks relative to those in other countries. Observers may logically point the finger at the nuclear threat posed by the North Korean regime as a key driver of this discount, but we believe there is more to it than just that.

In figure 2, I put South Korea’s valuations in the context of valuations in the United States and Japan. Price-to-book is a ratio we do not cite too often at WisdomTree, but I’ll do so here because it is the primary metric being cited by Japan’s reform-minded leadership at the Tokyo Stock Exchange (TSE). We think the Korea Exchange will follow Japan’s lead, spending 2024 willing its member firms’ price-to-book ratios higher.

Figure 2: Price-to-Book Ratio: “The Korea Discount”

With Japan, the major driver of bullishness on the country has been its “Name and Shame” initiative. The Tokyo Stock Exchange basically said to Corporate Japan: “Get your price-to-book ratio up or we are going to put your company on a list of firms that aren’t serious about reforming their corporate governance. We will shame you.”

Many Japanese corporations called the TSE’s bluff, so the exchange went ahead and published the list in January. Others took the warning to heart, outlining plans to boost profitability. The result: the price-weighted Nikkei 225 Index has melted up from 26,094 at the end of 2022 to 33,464 at last year’s close. It recently broke through 40,000.

Korea’s Financial Services Commission (FSC) is watching Japan’s rally and asking itself how it can get in on the game. The solution: bring “Name and Shame” to Seoul.

This initiative has a specific title that I think will be splashing headlines all year: the “Corporate Value-Up Program.” Whenever you want to Google Korea’s reforms, type that into the search bar.

Figure 3: South Korea Is Playing Japan’s Governance Card

Shareholder activists have their targets set on Asia too. Hedge funds are prowling in both Japan and Korea because about half of each country’s stocks trade below book value. Before the COVID-19 years, activists’ sights were on Europe. Not anymore.

Figure 4: Investor Activist Activity, Europe vs. Asia

Perhaps most important for the stock market is whether the Corporate Value-Up Program can reform the lumbering chaebol system. The chaebol are family-run companies that own controlling stakes in Korea’s conglomerates. Because of their sheer power, the result is very little voice for everyday stockholders or even for some large institutions.

While it is a slam dunk that small shareholders wish for stock prices to rise, the investor in Korean stocks needs to get their mind around the concept of controlling families wishing to keep valuations low. Who wouldn’t want the price of their largest asset to rise?

Chaebol scions who are subject to a 60% inheritance tax.

South Korea is a geriatric society; chaebol families are incentivized by the confiscatory inheritance tax to do everything in their power to keep valuations in the basement so that heirs do not get stuck with a large tax bill. President Yoon Suk Yeol floated the idea of an inheritance tax cut in January. But keep in mind that his popularity is nothing like FDR or Reagan. His approval rating is very low, so this could very well be a lame-duck situation, especially with the country engaged in parliamentary elections coming in a few weeks.

Meantime, there is another reform in store.

South Korea has a shot at following Japan’s lead on retirement contribution limit increases. On January 1, Japan tripled the annual maximum that an individual could put into a Nippon Individual Savings Account (NISA), which you can think of as Japan’s equivalent of a traditional IRA.

President Yoon seems to be taking a page from his neighbor’s playbook:

We will sharply expand eligibility for Individual Savings Accounts (ISAs) and increase the limit on the non-taxable amount. In order for the state and society to prevent the solidification of classes and increase society’s dynamism, the financial investment sector must be vitalized.

— Yoon Suk Yeol, President of South Korea, January 17, 2024

Another related matter: Korea is supposed to go forward with a capital gains tax hike this year, but Yoon has promised to eliminate it. The jury is still out on this, so keep an eye on this matter to see if he can pull it off.

In summary, the bullish catalysts for Korean stocks are:

- The Korea Discount becoming more overtly political.

- Japan’s “Name and Shame” arriving in Korea via the “Corporate Value-Up Program.”

- Hedge funds swirling.

- Possible inheritance tax cuts influencing chaebol families to be open to a bull market.

- Expanding retirement contributions and capital gains friendliness.

Some emerging markets funds own South Korea because they classify it as an emerging market, while others who view it as a developed economy may have as little as zero percent in the country. The WisdomTree strategies that hold big chunks in the country are XC, EMMF, XSOE, DGRE and DGS.

Further Information Supporting the Comparison of Funds

WisdomTree Emerging Markets ex-China Fund (XC): The WisdomTree Emerging Markets ex-China Fund seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Emerging Markets ex-China Index. It potentially avoids the challenges of investing in companies with significant government ownership. The objective is to gain targeted exposure to emerging market equities ex-China. It has a gross expense ratio of 0.32%.

WisdomTree Emerging Markets Multifactor Fund (EMMF): The WisdomTree Emerging Markets Multifactor Fund seeks capital appreciation by gaining targeted multifactor exposure to Emerging Market stocks. It can be used to strategically seek alpha and help reduce risk as a core holding over longer time horizons. The Fund may help lower the cost of active managers through systematic factor exposures. It has a gross expense ratio of 0.48%.

WisdomTree Emerging Markets ex-State-Owned Enterprises Fund (XSOE): The WisdomTree Emerging Markets ex-State-Owned Enterprises Fund seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Emerging Markets ex-State-Owned Enterprises Index. The Fund gains exposure to targeted emerging market equity from companies excluding state-owned enterprises, defined as having government ownership of more than 20%. The strategy can be used to complement emerging market exposure while neutralizing companies potentially influenced by government decisions. It has a gross expense ratio of 0.32%

WisdomTree Emerging Markets Quality Dividend Growth Fund (DGRE): The WisdomTree Emerging Markets Quality Dividend Growth Fund seeks income and capital appreciation. It is used to gain access to the current investment landscape of emerging market dividend growing companies by applying quality and growth screens. It has a gross expense ratio of 0.32%.

WisdomTree Emerging Markets Small Cap Dividend Fund (DGS): The WisdomTree Emerging Markets SmallCap Dividend Fund seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Emerging Markets SmallCap Dividend Index. It can be used to gain exposure to small cap equity of emerging market dividend paying companies. It has a gross expense ratio of 0.58%.

WisdomTree Emerging Markets High Dividend Fund (DEM): The WisdomTree Emerging Markets High Dividend Fund seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Emerging Markets High Dividend Index. The Fund is used to gain exposure to targeted emerging market all cap equity of high dividend yielding companies. It can diversify income strategies or substitute for emerging market active and passive strategies. It has a gross expense ratio of 0.63%.

Vanguard Emerging Markets Stock Index Fund (VWO): The Fund invests in stocks of companies located in emerging markets, such as China, Brazil, Taiwan, and South Africa. The goal is to closely track the return of the FTSE Emerging Markets All Cap China A Inclusion Index. It has high potential for growth, but also high risk; share value may swing up and down more than that of stock funds that invest in developed countries, including the United States. It has a gross expense ratio of 0.08%.

SPDR Portfolio Emerging Markets ETF (SPEM): The SPDR® Portfolio Emerging Markets ETF seeks to provide investment results that, before fees and expenses, correspond generally to the total return performance of the S&P® Emerging BMI Index. It is one of the low cost core SPDR Portfolio ETFs, a suite of portfolio building blocks designed to provide broad, diversified exposure to core asset classes. It has a gross expense ratio of 0.07%.

Schwab Emerging Markets Equity ETF (SCHE): The fund’s goal is to track as closely as possible, before fees and expenses, the total return of the FTSE Emerging Index. It invests in over 20 emerging market countries. It has a gross expense ratio of 0.110%.

DFA Dimensional Emerging Markets Core Equity 2 ETF (FNDE): The fund’s goal is to track as closely as possible, before fees and expenses, the total return of the Russell RAFI™ Emerging Markets Large Company Index. The strategy offers contrarian investing and disciplined rebalancing through a systematic process. It has a gross expense ratio of 0.390%.

iShares ESG Aware MSCI Emerging Markets ETF (ESGE): The iShares ESG Aware MSCI EM ETF seeks to track the investment results of an index composed of large- and mid-capitalization emerging market equities that have positive environmental, social and governance characteristics as identified by the index provider while exhibiting risk and return characteristics similar to those of the parent index. It has a gross expense ratio of 0.25%.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

Expense ratios as of 4/3/24.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty.

XC/XSOE: Investments in emerging markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks. The Fund’s investment strategy limits the types and number of investment opportunities available, and as a result, the Fund may underperform other funds. The Fund’s exposure to certain sectors, countries or regions may increase its vulnerability to any single economic or regulatory development related to such sector, country or region. The Fund is non-diversified; as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DGRE/DGS/DEM: Funds focusing on a single sector generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

EMMF: Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability or geographic events that adversely impact issuers of foreign securities. Derivatives used by the Fund to offset exposure to foreign currencies may not perform as intended. There can be no assurance that the Fund’s hedging transactions will be effective. The value of an investment in the Fund could be significantly and negatively impacted if foreign currencies appreciate at the same time that the value of the Fund’s equity holdings falls. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models, and the models may not perform as intended.

Additional risks specific to EMMF include but are not limited to emerging markets risk. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

Originally published 5 April 2024.

For more news, information, and analysis, visit the Beyond Basic Beta Channel.