Summary

- Texas oil and gas producers enjoy unique advantages, including great geology, significant infrastructure, and proximity to end markets.

- Recent M&A activity in the energy sector has reinforced the quality and desirability of Texas production, particularly in the Midland basin of the Permian.

- For investors wanting to own oil and gas producers, a Texas-oriented approach can provide advantages, including purer exposure to exploration and production (E&P) companies.

Texas is known for its prolific oil and natural gas production. However, investors may not fully recognize the advantages that producers in Texas enjoy relative to other regions of the US or the world. This note discusses Texas’ unique advantages for energy producers and why a Texas-oriented investment approach can be a better way to gain exposure to oil and gas producers.

Texas Boasts Low-Cost, Short-Cycle Inventory.

If real estate is all about location, something very similar can be said for oil and gas production. For producers in Texas, this is a matter of geology, drilling inventory (i.e., locations available for drilling new wells), proximity to end markets, infrastructure, and a supportive regulatory environment.

The Permian in West Texas and New Mexico is the most prolific shale play in the US and accounts for the bulk of Texas’ production. Texas is also home to the Eagle Ford, which is the third-largest oil-producing shale play in the US after the Bakken. The Barnett, portions of the Haynesville (East Texas), and portions of the Granite Wash (Panhandle) round out the shale plays in Texas.

With multiple oil and gas formations, Texas is home to more than 40% of the proved oil reserves in the US and almost a quarter of the country’s proved dry natural gas reserves. Not only are there ample reserves, but oil and gas can be extracted at a relatively low cost in a short timeframe. Beyond the quality of the rock, energy companies have seen significant efficiency gains over the years as they deploy new technologies and drilling techniques that ultimately save time and money.

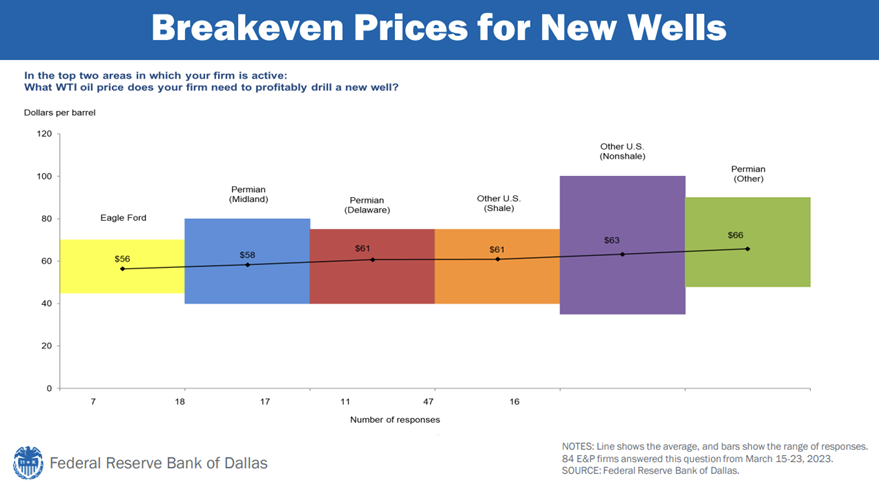

The chart below from the Federal Reserve Bank of Dallas based on March 2023 data helps illustrate the compelling economics for the Midland basin of the Permian and the Eagle Ford in particular. Note that the black line is an average of responses, and the bottom end of the range is closer to $40 per barrel (bbl). In other words, some wells in the Midland basin are profitable even with oil prices at $40/bbl.

The other advantage of producing oil and gas in Texas is proximity to end markets. For oil, that includes export terminals on the coasts and domestic refineries, with Texas boasting nearly a third of US refining capacity. For natural gas, that includes access to LNG export facilities, demand from Mexico, and other industrial demand centers along the Gulf Coast. With significant infrastructure in Texas, it is relatively easy and cost-efficient to move hydrocarbons to markets.

M&A Activity Reinforces the Appeal of Texas.

These advantages are well recognized by energy companies, with several recent acquisitions focused on expanding footprints in the Midland basin (Texas portion) of the Permian. The prime example is Exxon’s (XOM) pending acquisition of Pioneer Natural Resources (PXD) at an enterprise value of $64.5 billion. PXD has over 20 years of high-return drilling locations across 856,000 net acres in the Midland basin. Another recent example is Occidental’s (OXY) announced acquisition of private company CrownRock for $12 billion. CrownRock has 1,700 undeveloped drilling locations, including 750 locations with breakevens below a $40 crude price.

Last week, Apache (APA) announced the acquisition of Callon Petroleum (CPE) at a 14% premium in an all-stock transaction. While CPE’s acreage is mostly in the Delaware basin of the Permian with a smaller Midland footprint, its acreage is all in Texas. APA highlighted that the deal would add to its high-quality, short-cycle drilling inventory.

Broadly, consolidation has been a key theme in the energy sector (read more). Producers are particularly focused on adding low-cost, high-margin drilling inventory. Taking it one step further, M&A activity reinforces the quality and desirability of Texas acreage and production. Exxon’s $60+ billion acquisition is a strong validation for the resource base and its long-term advantages.

Looking for Exposure to Oil and Gas Producers? Look to Texas.

For investors wanting exposure to oil and gas producers (also called exploration and production companies or E&Ps) a Texas-oriented approach makes sense given the advantages discussed. The Alerian Texas Weighted Oil & Gas Index (ATXWO) is an index of energy companies that produce oil and gas in Texas and underlies the Texas Capital Texas Oil Index ETF (OILT). Companies in the index are weighted by the economic value of their oil and gas production in Texas. The maximum weight for a constituent is 10%. The index includes Texas pure plays like Diamondback Energy (FANG) and SM Energy (SM), as well as large, diversified energy companies like XOM, OXY, and Chevron (CVX).

Beyond the weighting scheme and Texas focus, this index and ETF have other important differentiators relative to other investment options. Due to the weighting scheme and 10% cap, the index is not dominated by XOM and CVX, which tends to be typical for broad energy sector products that are weighted by market cap. The index also includes smaller names that may not be eligible for broad energy sector products that use the S&P 500 as a starting universe.

Importantly, the index provides purer exposure to producers. The largest ETFs focused on oil and gas producers include refiners like Valero Energy (VLO), Phillips 66 (PSX), and Marathon Petroleum (MPC) among their top holdings. Refiners process crude into gasoline, diesel, and other products and have different performance drivers than oil and gas producers. The largest E&P ETF includes ethanol and ingredient producer Green Plains Inc. (GPRE) and renewable natural gas fuel provider Clean Energy Fuels (CLNE) – companies that are not E&Ps. ATXWO does not include any independent refiners or clean fuel companies, providing purer exposure to producers and therefore energy commodity prices.

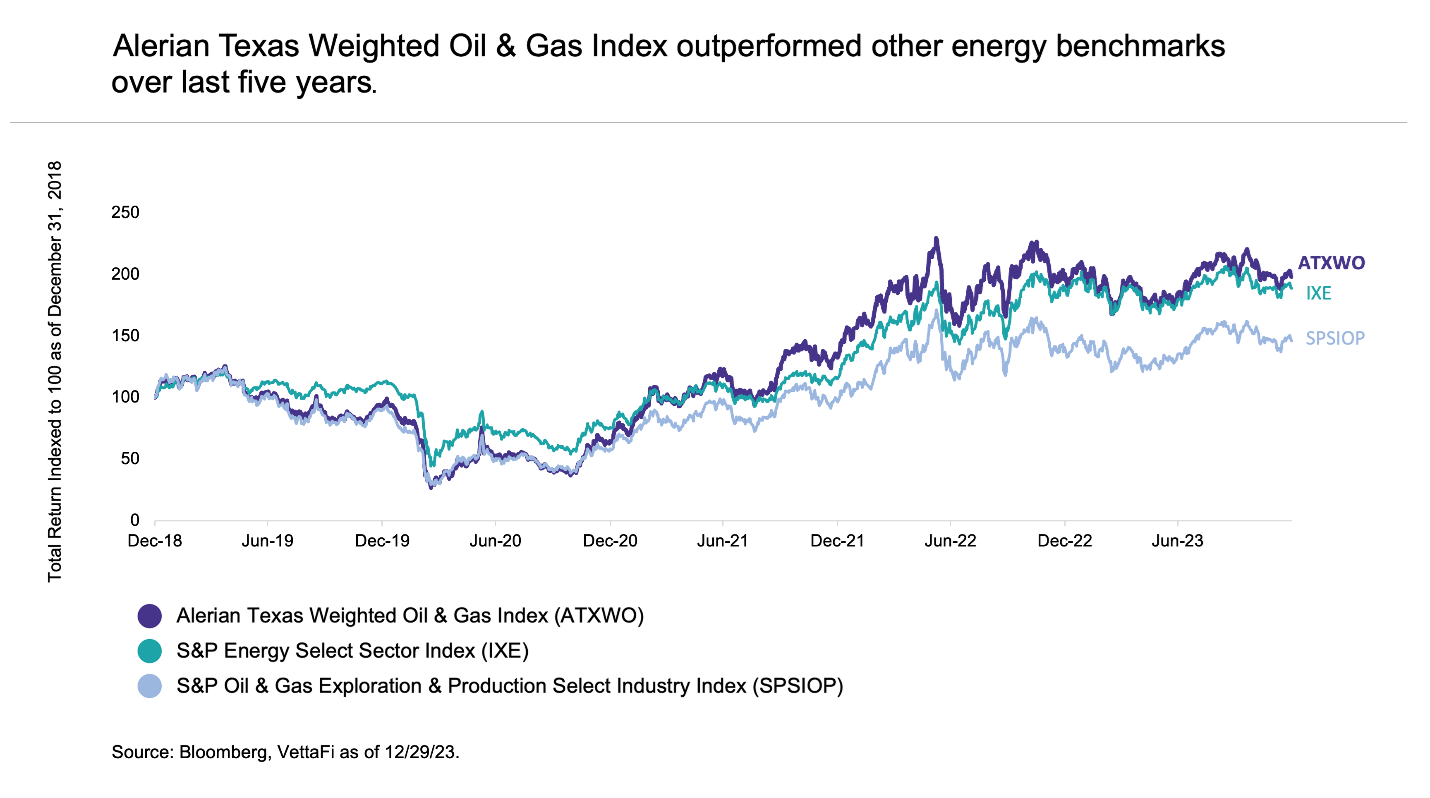

The five-year performance chart below compares the total return performance of ATXWO against the S&P Energy Select Sector Index (IXE), which underlies the Energy Select Sector SPDR Fund (XLE), and the S&P Oil & Gas Exploration & Production Select Industry Index (SPSIOP), which underlies the SPDR S&P Oil & Gas Exploration & Production ETF (XOP). ATXWO outperformed IXE and SPSIOP for the five-year period and saw particularly strong performance coming out of the pandemic as oil and natural gas prices recovered.

Bottom Line: The Case for Tailored Exposure to Texas Producers.

Energy products will generally have some exposure to Texas through the majors (XOM, CVX) or other E&Ps, but more tailored exposure to Texas is desirable given the state’s unique advantages. Importantly, ATXWO provides purer exposure to producers than other E&P-oriented indexes. Additional M&A activity could be supportive for companies in the index, as acquirers benefit from the addition of long-term drilling inventory and targets can enjoy a premium for their assets. For investors wanting exposure to oil and gas producers, a Texas-oriented approach is arguably a better mousetrap.

ATXWO is the underlying index for the Texas Capital Texas Oil Index ETF (OILT).

Related Research:

Bigger in Texas: Energy Reserves, Production & Exports

Better Together: Energy Consolidation Continues

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for OILT, for which it receives an index licensing fee. However, OILT is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of OILT.

For more news, information, and analysis, visit VettaFi | ETF Trends.