We’ve said it before and we’ll say it again: risk cannot be destroyed, only transformed.

But, these things might have their use yet…

Levered ETFs in a Portfolio

![]() Held as 100% of our wealth, a 2X daily reset equity ETF may not be too prudent. In the context of a portfolio, however, things change.

Held as 100% of our wealth, a 2X daily reset equity ETF may not be too prudent. In the context of a portfolio, however, things change.

Consider, for example, using 50% of our capital to invest in a 2x equity exposure and the remaining 50% to invest in bonds. In effect, we have created 150% exposure to a 67/33 stock/bond mixture. For example, we could hold 50% of our capital in the ProShares Ultra S&P 500 ETF (“SSO”) and 50% in the iShares Core U.S. Bond ETF (“AGG”).

To understand the portfolio exposure, we have to look under the hood. What we really have, in aggregate, is: 100% equity exposure and 50% bond exposure. To get to 150% total notional exposure, we have to borrow an amount equal to 50% of our starting capital. Indeed, at the portfolio level, we cannot differentiate whether we are using that 50% borrowing to lever up stocks, bonds, or the entire mixture!

In this context, levered ETFs become a lot more interesting.

The risk, of course, is in the resets. To really do this, we’d have to rebalance our portfolio back to a 50/50 mix of the 2x levered equity exposure and bonds on a daily basis. If we could achieve that, we’d have built a daily reset 1.5x 66/33 portfolio.

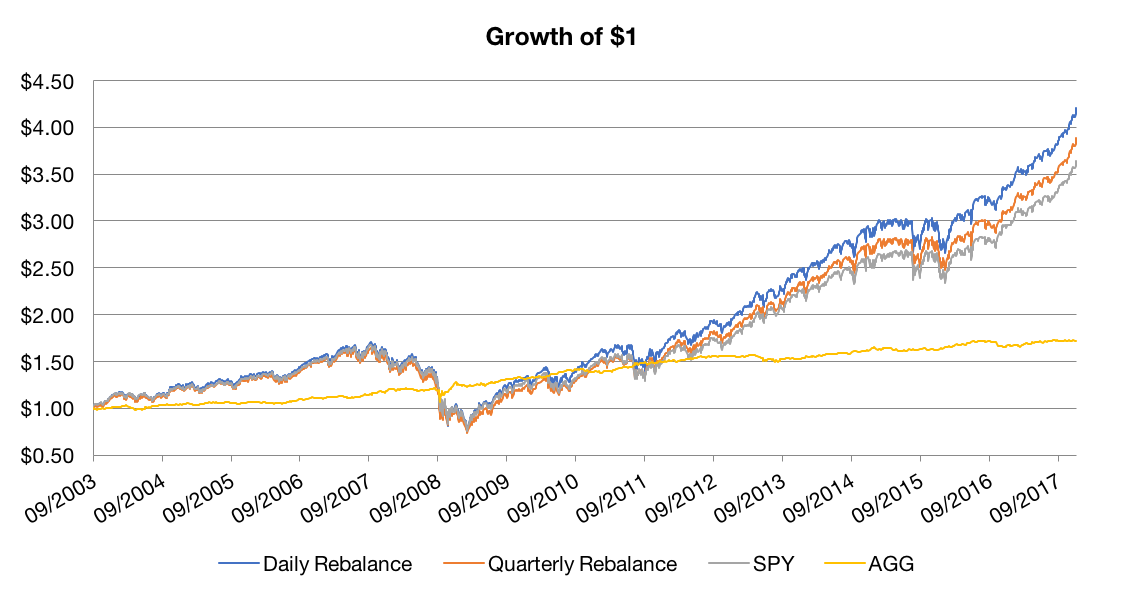

More realistically, investors may be able to rebalance their portfolio quarterly. How far does that deviate from the daily rebalance? We plot the two below.

Source: CSI. Calculations by Newfound Research. Returns for the Daily Rebalance and Quarterly Rebalance portfolios are backtested and hypothetical. Returns are gross of all fees except underlying ETF expense ratios. Returns assume the reinvestment of all distributions. Cost of leverage is assumed to be equal to the return of a 1-3 Year U.S. Treasury ETF (“SHY”). Past performance is not indicative of future results. The Daily Rebalance portfolio assumes 50% exposure to a hypothetical index providing 2x daily exposure of the SPDR S&P 500 ETF (“SPY”) and 50% exposure to the iShares US Core Bond ETF (“AGG”) and is rebalanced daily. The Quarterly Rebalance portfolio assumes the same exposure, but rebalances quarterly.

Indeed, for aggressive investors, a levered equity ETF mixed with bond exposure may not be such a bad idea after all. However – and to steal a line from our friends at Toroso Asset Management – levered ETFs are likely “buy-and-adjust” vehicles, not buy-and-hold. The frequency of adjusting, and the cost of doing so, will play an important role in results.

A Particular Application with Alternatives

Where levered ETFs may be particularly interesting is in the context of liquid alternatives.

In the past, we have said that many liquid alternatives, especially those offered as ETFs, have a volatility problem. Namely, they just don’t have enough volatility to be interesting.

Traditionally, allocating to a liquid alternative requires us removing capital from one investment to “make room” in our portfolio, which creates an implicit hurdle rate. If, for example, we sell a 5% allocation of our equity portfolio to make room for a merger arbitrage strategy, not only do we have to expect that the strategy can create alpha beyond its fees, but it also has to be able to deliver a long-term return that is at least in the same neighborhood of the equity risk premium. Otherwise, we should be prepared to sacrifice return for the benefit of diversification.

One solution to this problem with lower volatility alternatives is to fund their allocation by selling bonds instead of stocks. Bonds, however, are often our stable ballast in the portfolio. Regardless of how poorly we expect core fixed income to perform over the next decade, we have a high degree of certainty in their return. Asking us to sell bonds to buy alternatives is often asking us to throw certainty out the window.

By way of example, consider the Reality Shares DIVS ETF (“DIVY”). We wrote about this ETF back in August 2016 and think it is a particularly compelling story. The ETF buys the floating leg of dividend swaps, which in theory captures a premium from investors who want to insure their dividend growth exposure in the S&P 500.

For example, if the swap is priced such that the expected growth rate of S&P 500 dividends is 5% over the next year, but the realized growth is 6%, then the floating leg keeps the extra 1%. The “insurance” aspect comes in during years where realized growth is below the expected rate, and the floating leg has to cover the difference. To provide this insurance, the floating leg demands a premium.

A dividend swap of infinite length should, in theory, converge to the equity risk premium. Short-term dividend swaps (e.g. 1-year), however, seem to exhibit a potentially unique risk premium, making them an interesting diversifier within a portfolio.

While DIVY has performed well since inception, finding a place for it in a portfolio can be difficult. With low volatility, we have two problems. First, for the fund to make a meaningful difference, we need to make sure that our allocation is large enough. Second, we likely have to slot DIVY in for a low volatility asset – like core fixed income – so that we make sure that we are not creating an unreasonable hurdle rate for the fund.

Levered ETFs may allow us to have our cake and eat it too.

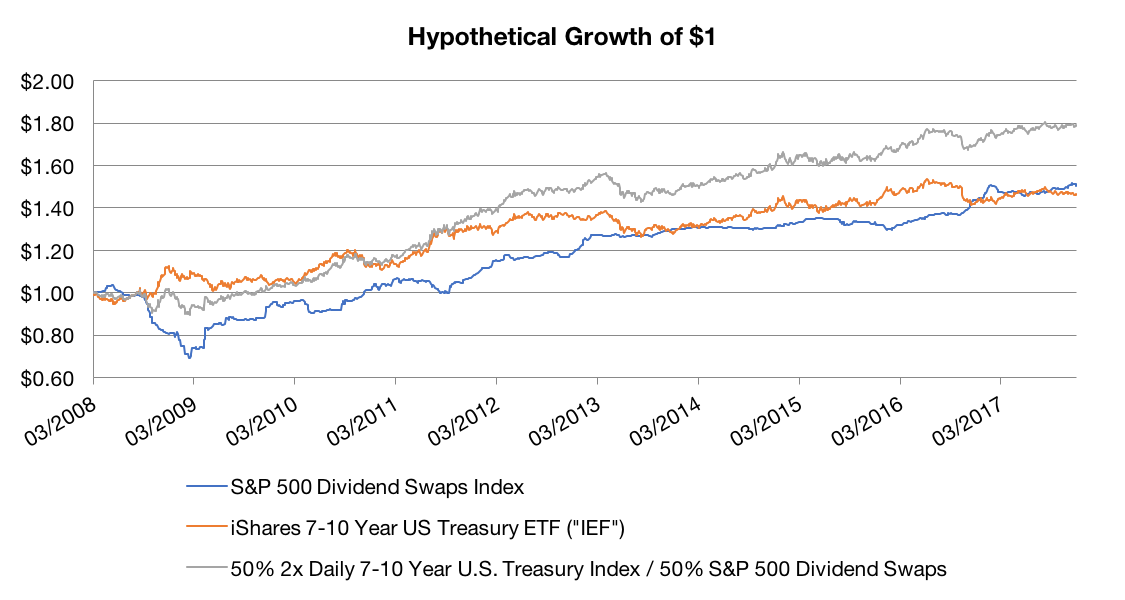

For example, ProShares offers an Ultra 7-10 Year Treasury ETF (“UST”), which provides investors with 2x daily return exposure to a 7-10 year U.S. Treasury portfolio. For investors who hold a large portfolio of intermediate-term U.S. Treasuries, they could potentially sell some exposure and replace it with 50% UST and 50% DIVY.

As before, the question of “when to reset” arises: but even with a quarterly [rebalance, we think it is a compelling concept.

Source: CSI. Calculations by Newfound Research. Returns for the S&P 500 Dividend Swaps Index and 50% 2x Daily 7-10 Year US Treasuries / 50% Dividend Swap Index portfolios are hypothetical and backtested. Returns are gross of all fees except underlying ETF expense ratios. Returns assume the reinvestment of all distributions. Cost of leverage is assumed to be equal to the return of a 1-3 Year U.S. Treasury ETF (“SHY”). Past performance is not indicative of future results. The 50% 2x Daily 7-10 Year US Treasuries / 50% Dividend Swap Index assumes a quarterly rebalance.

Conclusion

Leverage is a tool. When used prudently, it can help investors potentially achieve much more risk-efficient returns. When used without care, it can lead to complete ruin.

For many investors who do not have access to traditional means of leverage, levered ETFs represent one potential opportunity. While branded as a “trading vehicle” instead of a buy-and-hold exposure, we believe that if prudently monitored, levered ETFs can be used to help free up capital within a portfolio to introduce diversifying exposures.

Beyond the leverage itself, the daily reset process can introduce risk. While it helps maintain the leverage ratio – reducing risk after losses – it also re-ups our risk after gains and generally will increase long-term volatility drag from mean reversion.

This daily reset means that when used in a portfolio context, we should, ideally, be resetting our entire portfolio daily. In practice, this is impossible (and likely imprudent, once costs are introduced) for many investors. Thus, we introduce some tracking error within the portfolio.

We should note that there are monthly-reset leverage products that may partially alleviate this problem. For example, PowerShares and ETRACS offer monthly reset products and iPath offers “no reset” leverage ETNs that simply apply a leverage level at inception and never reset until the ETN matures.

Perhaps the most glaring absence in this commentary has been a discussion of fees. Levered ETP fees vary wildly, ranging from as low as 0.35% to as high as 0.95%. When considering using a levered ETP in a portfolio context, this fee must be added to our hurdle rate. For example, if our choice is between just holding the iShares 7-10 Year U.S. Treasury ETF (“IEF”) at 0.15%, or 50% in the ProShares Ultra 7-10 Year Treasury ETF (“UST”) and 50% in the Reality Shares DIVS ETF (“DIVY”) for a combined cost of 0.93%, the extra 0.78% fee needs to be added to our hurdle rate calculation.

Nevertheless, as fee compression marches on, we would expect fees in levered ETFs to come down over time as well, potentially making these products interesting for more than just expressing short-term trading views.

Corey Hoffstein is the Co-founder & CIO at Newfound Research, a participant in the ETF Strategist Channel.